United Maritime Corp's Fleet Restructuring and Capital Management Define 2025 Performance

Operating losses and revenue contraction underscore United Maritime's navigation through dry bulk market pressures and strategic fleet transitions.

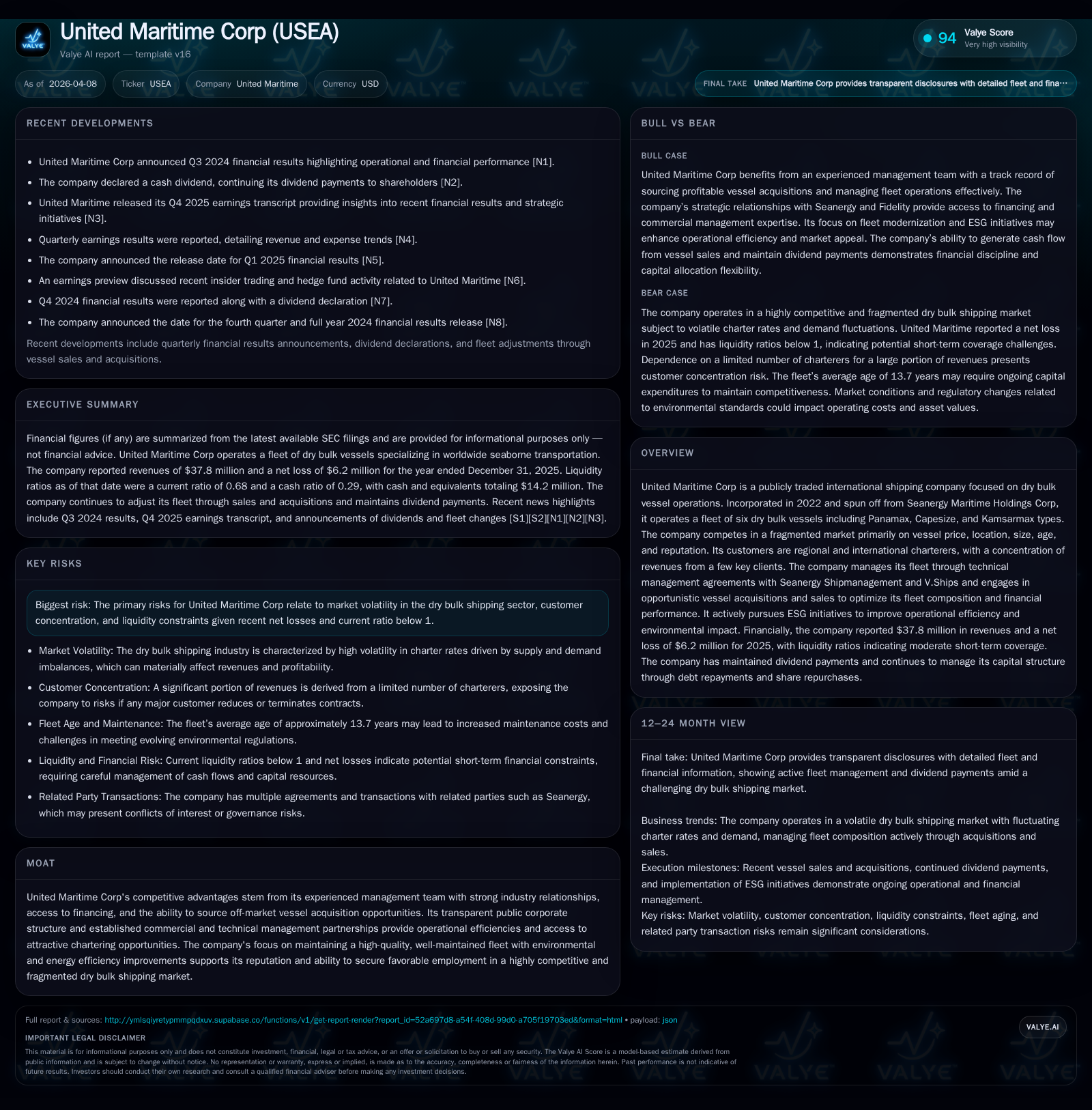

United Maritime Corp, a relatively new player in the dry bulk shipping sector spun off from Seanergy Maritime Holdings, reported a decline in revenues by about 17% in 2025 accompanied by an operating loss. The company's operational strategy focuses on managing a diverse fleet of dry bulk vessels including Panamax, Capesize, and Kamsarmax types, with active fleet optimization through acquisitions and sales during 2024-2026. Despite ongoing net losses and a current ratio below 1 suggesting liquidity constraints, the company generated positive operating cash flow and maintained discipline in capital expenditures and buybacks. Future growth hinges on successful vessel acquisitions, charter rate recovery, and navigating risks from market volatility and customer concentration.

Company Overview

United Maritime Corp (ticker: USEA) is an international dry bulk shipping operator established through a spin-off from Seanergy Maritime Holdings Corp in early 2022. Operating primarily in the dry bulk sector with products such as coal, iron ore, and grains, the company manages a fleet including Panamax, Capesize, and Kamsarmax vessels totaling a carrying capacity nearing 578,000 deadweight tons as of end-2025 [S20]. The ship age profile averages around 13.7 years though strategic acquisitions aim to modernize the fleet.

Historical Financial Performance

United Maritime’s top-line revenue reached $37.8 million in FY2025, down from $45.4 million in FY2024 representing nearly a 17% contraction [F1]. Operating income swung negative to -$455,000 after generating positive operating results of roughly $4.8 million the prior year. This reversal reflects challenging market freight rates during the year compounded by expenses associated with fleet restructuring.

Net losses widened to $6.2 million from $3.4 million in FY2024 after recording modest net profits in earlier years since spin-off initiation [F1]. The company’s ROE for FY2025 approximated -11.7%, indicating negative returns relative to equity base.

Despite losses at the bottom line level, operational cash flows remained positive at over $2.2 million, demonstrating cash generation capability amid transitional conditions [F1]. Capital expenditures more than doubled to about $668,000 as investments focused on vessel upgrades, regulatory compliance enhancements, and operational efficiency initiatives.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 38 | -6 | 2 | 0 | -16.8% | -82.9% |

| 2024 | 45 | -3 | 3 | 5 | +26.0% | -1630.8% |

| 2023 | 36 | 0 | -6 | 7 | +58.3% | -99.4% |

| 2022 | 23 | 37 | 8 | 41 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 2 | -11.7 |

| 2024 | 0 | 3 | -5.6 |

| 2023 | 1 | -88 | 0.3 |

| 2022 | 3 | -73 | 58.1 |

Source: SEC companyfacts cache [F1].

Table: Summary financial performance highlights adjusted for vessel sales impact and capital activities.

Fleet Development and Operational Strategy

Since inception post-spin-off from Seanergy Maritime Holdings Corp,[S20] United Maritime has actively managed its fleet composition through sales and acquisitions aimed at optimizing its presence in key size segments.

Key activities during late-2024 into early-2026 include:

- Acquisition via bareboat charter agreements of modern Capesize vessels such as M/V Dukeship (February 2026) with option purchase plans involving downpayments and pre-negotiated buyout prices [S1][S13].

- Agreement reached for acquiring M/V Squireship expected mid-2026 delivery further bolsters Capesize segment exposure with significant cargo capacity increases.

- Sale contracts executed for older or less economic vessels including planned disposal of M/V Cretansea slated for May 2026 delivery to new owners [S20].

- The company operates all vessels under technical management agreements primarily with Seanergy Shipmanagement and V.Ships enabling operational efficiencies [S1][S9].

This dynamic restructuring aligns with enhancing environmental standards compliance—a growing regulatory focus driving capital deployment for vessel improvements—as well as positioning for favorable charter rates leveraging vessel quality.[S21]

Industry Context

The global dry bulk shipping market remains highly fragmented with competition based on multiple factors including age and size of vessels along with availability and price per charter contract.[S9] Seasonal trade patterns linked to coal demand spikes during summer heat waves or grain harvest seasons create cyclical demand fluctuations that operators must manage carefully.[S9]

United Maritime’s sizeable revenues concentrated among a few large charter customers (~84% from top five charterers in FY25) expose it to client-specific risks amid broader freight rate volatility where forward freight agreement hedges are not systematically disclosed.[S9]

Capital Structure and Liquidity Overview

As of December end-2025:

- Cash and equivalents were reported at roughly $14.2 million providing near-term liquidity buffer.[F1]

- Current assets totaled about $33.1 million against current liabilities of approximately $48.6 million yielding a current ratio near 0.68 pointing toward tighter short-term liquidity coverage.[F1]

- The company employs various loan facilities secured against vessel collateral including sale-and-leaseback financing structures which have been used extensively for recent vessel acquisition funding.[S12][S15]

- Debt repayments were significant in 2025 totaling about $31.7 million reducing outstanding debt burdens but also contributing to cash outflows from financing activities of nearly $34.8 million.[F1][S11]

The company’s approach mixes traditional bank loans at fixed or SOFR-linked rates with alternative finance arrangements common within maritime asset financing such as leasing structures offering some flexibility but obligating future purchase commitments.[S10][S15]

Returns and Capital Allocation Policies

Despite experiencing net losses over the last two fiscal years,[F1] United Maritime has maintained a dividend policy evidenced by consistent quarterly payouts including a recent declaration of $0.10 per share for Q4-2025 paid April 2026 representing a signal on shareholder value focus amid operational challenges.[N2][S13]

Share repurchase programs remain active albeit modestly scaled relative to total equity with approximately $1.6 million available for additional repurchases as of early April 2026 after incremental buybacks totaling around $220k in shares during FY25.[S6] These capital returns occur alongside equity incentive plans authorizing issuance of shares to directors and service providers supporting corporate governance alignment.[S4][S17]

Operating free cash flow remains positive at about $1.54 million (operating cash flow minus capex) reflecting prudent cash management despite margin compression.[F1]

Growth Prospects and Challenges Ahead

Growth potential is closely tied to several levers:

- Increasing exposure to larger Capesize vessels via recent acquisitions may improve earnings leverage given higher capacity utilization prospects under favorable spot/time charter rates.[N3][S20]

- Opportunistic vessel sales help recycle capital from older tonnage towards modernized fleet assets complying with emerging environmental regulations enhancing marketability.[S21]

- Close collaboration with Seanergy facilitates access to off-market vessel deals through rights of first refusal tailored toward Capesize vessels plus favorable commercial management synergies.[S16]

- Investment into technological platforms aiming at AI-driven ship management software suggests efforts toward operational efficiency gains supporting margin improvement over time.[S11]

Conversely:

- Market volatility remains high due to global economic uncertainties impacting commodity trade volumes affecting dry bulk shipping demand cycles.

- Customer concentration risk persists; dependence on few large charterers heightens vulnerability if demand shifts or contracts are not renewed favorably.[S9]

- Liquidity pressures persist reflected by sub-one current ratios combined with loan maturity profiles require effective capital management strategies going forward.

- Compliance costs from tightening environmental regulations could elevate operating expenses unpredictably impacting margins if not offset by rate improvements or efficiencies.[S21]

What To Watch: Key Milestones & Indicators (Analysis)

In the absence of explicit company multi-year guidance,[N3] stakeholders should monitor:

- Progression of vessel acquisitions/deliveries particularly the M/V Squireship expected mid-2026 which will materially alter capacity.

- Recovery or stabilization trends in dry bulk charter rates impacting revenue trajectory.

- Ongoing effectiveness of fleet renewal measured through operating days available vs downtime related to surveys or drydocking.

- Quarterly dividend declarations signaling confidence versus potential cuts reflective of financial stress.

- Changes in debt levels or refinancing terms which may affect liquidity risk profile.

Conclusion

United Maritime Corp remains focused on leveraging its experienced management team and strategic partnerships to manage its mid-sized dry bulk shipping operations amid challenging market conditions throughout recent years since its spin-off origin in early 2022.[S16] While financial results reflect pressures manifesting as contracted revenue streams and operational losses during FY25,[F1] active fleet optimization combined with stable operating cash flows underpin viability.

The company’s pursuit of larger-capacity Capesize vessels alongside divesting legacy tonnage points toward repositioning for improved scale benefits while simultaneously maintaining shareholder distributions through dividends amidst net losses demonstrates balancing act between growth ambitions and capital stewardship.

Risks mainly stem from macroeconomic uncertainty affecting freight rates compounded by high client concentration requiring careful liquidity management given current liabilities exceeding readily available assets.[F1][S9] Nonetheless United Maritime’s transparent corporate structure coupled with integrated commercial/technical management arrangements provides access points for opportunistic growth beyond cyclical troughs common within the fragmented dry bulk marketplace.

This analysis is based solely on publicly filed information including SEC filings [F1], official company press releases [N#], regulatory disclosures [S#], and industry-standard shipping sector context without any speculative assumptions or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments