Aspire Biopharma's Path from Early Losses to Potential Market Disruption

Aspire Biopharma leverages proprietary sublingual technology to redefine aspirin delivery amid operational and financial challenges.

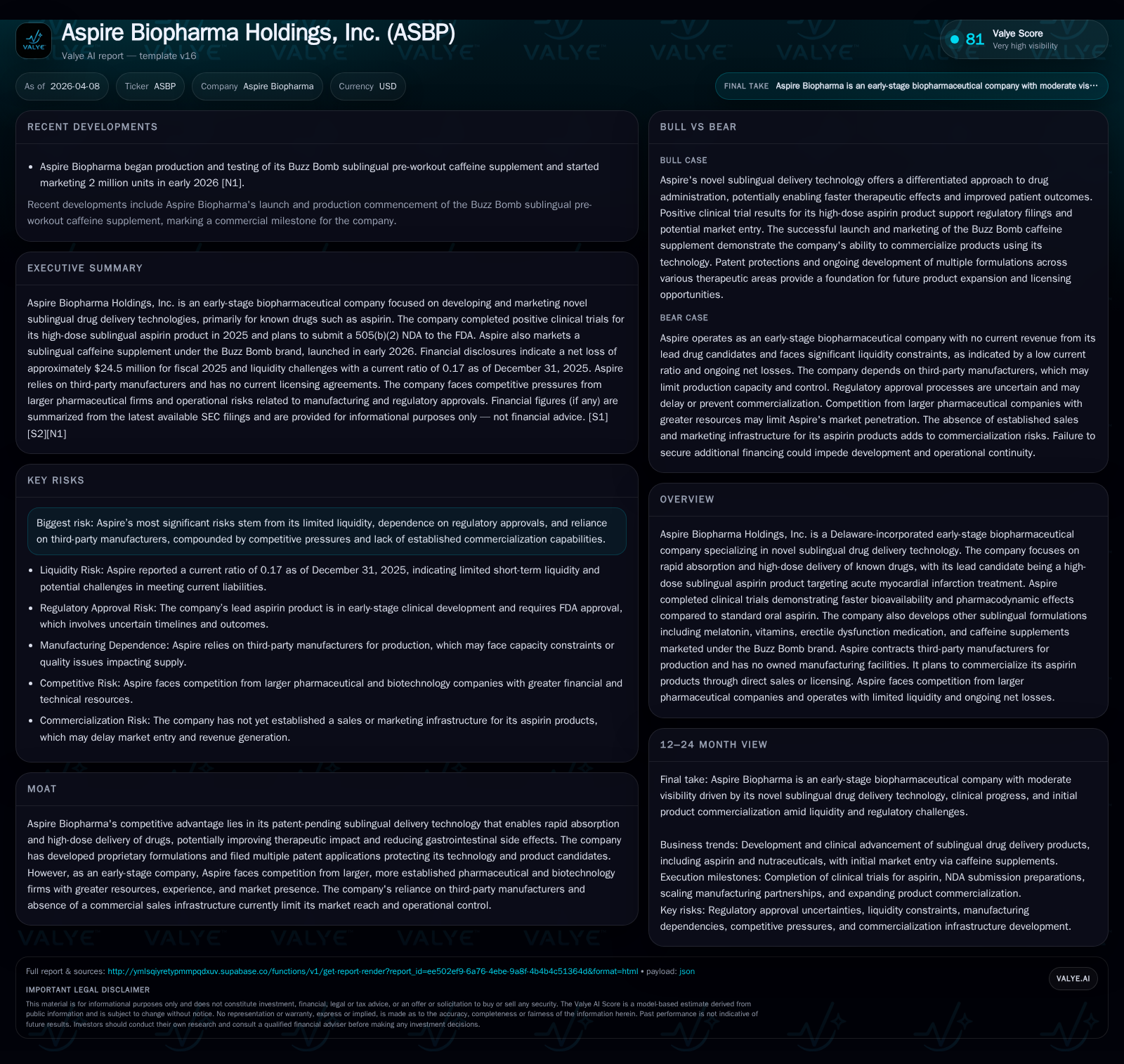

Aspire Biopharma Holdings is an early-stage biopharmaceutical company pioneering a patent-pending sublingual drug delivery platform, with a lead high-dose aspirin candidate aimed at acute myocardial infarction treatment. Despite promising clinical trials that show enhanced bioavailability over conventional oral aspirin, Aspire faces the typical hurdles of an emerging biopharma: persistent net losses, limited liquidity with a weak current ratio, absence of manufacturing ownership, and regulatory uncertainties surrounding novel drug formulations. The company’s financials reveal increasing operating cash flow deficits and negative equity, underscoring capital intensity during clinical development. Going forward, regulatory approvals, manufacturing scale-up via contract manufacturers, and successful commercialization or licensing deals are pivotal milestones to monitor.

From Concept to Clinical Validation: Historical Revenue and Loss Trends

Aspire Biopharma Holdings has charted a classic trajectory for an emergent biopharmaceutical enterprise focused on innovative drug delivery technology. Incorporated as a Delaware entity only recently in February 2025 following its prior incarnation as a Puerto Rico corporation since September 2021 [S1], Aspire is positioned at the confluence of early-stage clinical development and nascent commercial activities.

The company's revenue history is sparse, reflecting the developmental stage, with commercial sales yet to meaningfully materialize from its flagship sublingual aspirin candidate or ancillary nutraceutical offerings under the Buzz Bomb brand . Fiscal year data from 2022 through 2025 illustrate persistent operating losses driven by substantial R&D expenditures necessary to validate its pharmacokinetic innovations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -24 | -5 | -95.3% |

| 2024 | -13 | -2 | -380.9% |

| 2023 | 4 | -1 | +33.6% |

| 2022 | 3 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 383.9 | |

| 2024 | 14 | 80.5 |

| 2023 | 285 | -1385.9 |

| 2022 | -33.6 |

Source: SEC companyfacts cache [F1].

Note: Operating income data is only available for FY2025; other years omitted accordingly.

The turnaround from modest positive net income in early years (FY2022-23) to steep losses starting FY2024 (-$12.5M) marks intensified clinical trial expenditures relating to high-dose sublingual aspirin programs [F1]. The growing negative operating cash flow confirms this capital-intensive phase transition.

The Promise of Rapid-Absorption Sublingual Aspirin: Pipeline and Technology Advantages

Aspire’s core technological asset is its patent-pending sublingual drug delivery platform designed to achieve rapid systemic absorption while facilitating high-dose administration without the gastrointestinal side effects typical of oral aspirin . This platform has produced a promising candidate: a high-dose sublingual aspirin intended for acute myocardial infarction treatment.

Completed clinical trials as of July 2025 demonstrated superior pharmacokinetics compared to standard oral aspirin cohorts, evidencing quicker Tmax (time to peak concentration) and enhanced Cmax values alongside measurable improvements in pharmacodynamics—specifically serum thromboxane B2 inhibition—supporting rapid platelet inhibition [S10]. Notably, these trials were conducted under exempt IND requirements given the active ingredient's approval status but novel route of administration [S10].

While improved bioavailability theoretically could increase therapeutic impact during emergency cardiovascular episodes by circumventing first-pass metabolism delays, this untested delivery modality carries the risk of protracted regulatory scrutiny due to its novelty within FDA frameworks focused traditionally on established oral aspirin formulations [S7][S20].

Navigating Regulatory and Market Entry Barriers

Regulatory approval remains a critical gating hurdle for Aspire’s lead product. The FDA application pathway involves stringent demands for demonstrating safety, efficacy, reliability under Good Laboratory Practice (GLP), current Good Manufacturing Practice (cGMP), and compliance with the Federal Food, Drug & Cosmetic Act [S11][S20].

Aspire's interaction with regulators has included formal pre-IND consultation yielding positive feedback necessary for NDA preparation [S20]. Nevertheless, FDA approval is not assured given the unique claim around sublingual administration enhancing delivery speed for an established agent. The regulatory environment also mandates extensive labeling, marketing controls, post-marketing surveillance obligations, increasing Aspire’s compliance complexity upon market entry [S4][S6][S7][S20].

Market acceptance poses another formidable barrier: physicians habituated to oral aspirin may hesitate to adopt alternative formulations without robust outcome data beyond surrogate lab markers like thromboxane suppression [S5]. Pricing pressures from entrenched oral aspirin generics could constrain reimbursement potential and patient uptake despite any incremental clinical benefit [S5].

Finally, compliance with healthcare fraud & abuse laws remains an ongoing operational consideration that will rise in salience upon commercialization [S4], necessitating careful governance structures embedded in future sales efforts.

Manufacturing Strategy: Contract Reliance and Capacity Risks

Without owned production facilities, Aspire relies exclusively on third-party contract manufacturers specialized in cGMP-compliant processes [S1]. Glatt's New Jersey site serves as the principal manufacturer of bulk active pharmaceutical ingredient batches for both clinical trials and prospective commercial sales [S1][S12]. A separate fill-and-finish contract manufacturer converts active ingredient into packaged dosage forms fit for patient use.

More recently in January 2026, Aspire engaged Microsize CDMO in Pennsylvania to broaden its manufacturing base for upcoming clinical batches following FDA communications about scale requirements [S1][S12]. While leveraging specialist CDMOs mitigates upfront capital expenditure risks inherent in facility ownership, it introduces supply chain vulnerabilities including possible capacity constraints during ramp-up phases or demand spikes [S8][S17]. Additionally, loss of operational control inherent to outsourcing heightens coordination complexities necessitating deep pharma-experienced oversight from Aspire personnel assigned to vendor management [S1].

The fill-and-finish pathway emphasizes sector nuances; production bottlenecks here can delay final product availability despite sufficient bulk API stocks upstream — a common risk in transitional biopharma startups scaling toward commercialization.

Financial Trajectory: Operating Cash Flow Struggles and Equity Position

Aspire’s financial statements reveal intensifying capital consumption without offsetting revenue streams characteristic of early biopharmas undergoing crucial clinical validation phases [F1]. The company recorded escalating net losses culminating in $24.48 million negative net income for FY2025—an approximate decline of 95% year-over-year relative to FY2024 losses ($12.54 million) [F1].

Operating income turned more deeply negative at nearly $19.35 million for FY2025 compared to prior years where data are unavailable but implied positive margins existed earlier [F1]. Correspondingly, operating cash flow declined sharply by nearly 140% reaching negative $4.92 million last fiscal year — indicating amplified cash burn primarily directed at clinical trial activities rather than operational scalability or marketing efforts yet.

Liquidity metrics further underscore funding stresses; quarter-end current assets stood at just above $1.3 million against $7.6 million current liabilities yielding a critically low current ratio of approximately 0.17—well below healthy operational thresholds [F1]. Meanwhile equity remains deeply negative at $-6.37 million after slight improvement from the prior year's $-15.57 million deficit indicating accumulated losses eroding shareholder value [F1].

This laddering loss pattern typifies highly capital-intensive biotechs progressing from preclinical research through pivotal studies requiring substantial financing infusions absent corresponding revenues.

Capital Allocation and Shareholder Returns: Absence of Dividends, Focus on Financing

Aspire pays no dividends nor conducts share repurchases currently; available data indicate large historic buyback activity prior to going public was discontinued post-listing reflecting redirected capital priorities towards sustaining R&D investment amid heavy losses [F1][S21][S26].

Recent financings include issuance of Series A Convertible Preferred Stock coupled with convertible debt arrangements notably completed between early 2025 through Q1 2026 [S14][S21][S26][S27][F1]. These raise vital working capital although they introduce dilution potential and heightened debt service obligations compounded by original issue discounts.

Governance disclosures identify absence of key person insurance policies on critical executives—a risk factor that might exacerbate uncertainty around leadership continuity impacting execution during critical regulatory milestones [S7]. Capital allocation strategy broadly reflects pragmatic focus on bridging developmental stages toward potential licensing or direct commercialization rather than shareholder distributions.

Return on equity metrics are distorted due to negative equity bases but underline absence of profitability expected at this juncture.

What Investors Should Monitor Next

Given absence of company-published forward guidance or explicit milestone timelines beyond recently completed studies and manufacturing contracts [N/A], investors should track:

- Progression through FDA NDA submission phases including any feedback cycles following post-trial efficacy/safety data submissions.

- Completion statuses of planned future clinical enrollments if applicable or initiation of confirmatory studies triggered by FDA requests.

- Negotiations or announcements around out-licensing agreements or strategic partnerships potentially accelerating commercial scale manufacture or market access.

- Additional financing rounds evidencing ability to maintain operations without excessive dilution.

- Expansion or diversification in manufacturing partnerships addressing emerging capacity limits noted with primary CDMOs.

- Competitive landscape developments: entries by larger pharma players into rapid-delivery antiplatelet agents that may impinge on aspirational market share positions.

- Regulatory compliance updates especially related to cGMP facilities audits, marketing authorization conditions imposed post-NDA approval.

- Changes in Nasdaq listing status relevance given historical notifications concerning bid price maintenance noted in SEC filings which could impact trading liquidity conditions.

Continued scrutiny across these vectors will be essential for stakeholders seeking to contextualize Aspire Biopharma’s transition from an innovation-heavy early-stage status toward tangible commercial returns within a highly regulated pharmaceutical framework.

Disclaimer: This document synthesizes publicly available information including SEC filings (Forms 10-K/A etc.), company meta-data summaries provided by Valye News research systems, and factual analysis without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments