Franklin Covey's Revenue Decline and Profit Squeeze Amid Strategic Transformation

The company faces a challenging recovery path with shifting revenue dynamics and squeezed profitability despite ongoing investment in sales and content.

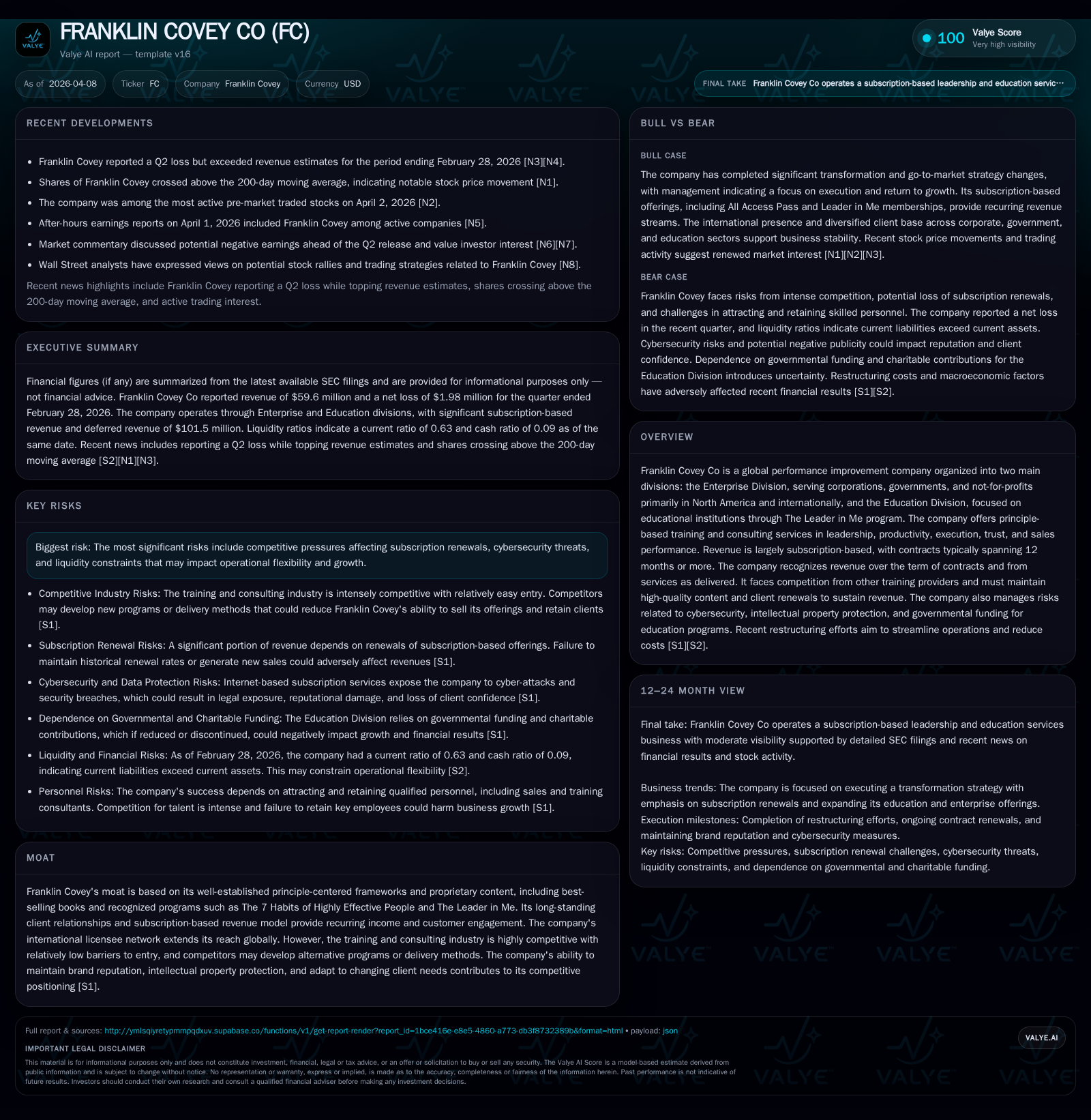

Franklin Covey Co experienced a top-line contraction and a steep decline in operating income in fiscal 2025, impacted by macroeconomic headwinds and strategic restructuring. Revenue fell 7% year-over-year to $267 million, while operating income plunged over 80%, reflecting margin pressure from investments and competitive challenges. The business model centers on subscription-based leadership and education training delivered globally through its Enterprise and Education divisions, with recurring revenue representing a majority of sales. Looking ahead, successful execution of new go-to-market strategies and client retention will be critical growth drivers, although risks around renewals, competition, and cybersecurity loom large. The company maintains healthy free cash flow but carries liquidity constraints that require careful capital allocation alongside cautious optimism for accelerating growth in fiscal 2026–27.

Company Overview

Franklin Covey Co is a global performance improvement firm specializing in principle-centered training and consulting services aiming to elevate leadership, productivity, execution, trust, and sales effectiveness across organizations. Its business is split into two main divisions: the Enterprise Division serving corporations, governments, and nonprofits primarily in North America and internationally; and the Education Division which uses its proprietary 'Leader in Me' program focused on educational institutions [S1][S26]. Many of Franklin Covey’s revenues derive from subscription-based offerings with contracts typically spanning one year or more, emphasizing the importance of customer renewals for sustained income streams.

Historical Financial Performance

The company faced notable top-line contraction in fiscal year 2025 compared to prior years. Total revenue declined by approximately 7% to $267 million from $287 million in FY2024 [F1]. This drop reflected broader macroeconomic headwinds including subdued U.S. federal government spending impacting contract volumes [S13]. Concurrently, operating income deteriorated sharply by nearly 83%, slumping from $33 million in FY2024 down to just $5.7 million in FY2025 [F1], signaling margin compression tied partly to investments made in transformational sales strategies.

Net income followed a similar trend with an 87% decrease year-over-year to around $3 million [F1]. Operating cash flows also showed volatility falling almost 52% YoY but remained positive at nearly $29 million [F1]. Capital expenditures ramped up significantly by over 120% consistent with the company’s commitment to enhanced content development and delivery infrastructure [F1]. Despite these pressures, free cash flow stayed healthy at approximately $20.7 million given controlled capex levels.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 267 | 3 | 29 | 6 | -7.0% | -86.9% |

| 2024 | 287 | 23 | 60 | 33 | +2.4% | +31.6% |

| 2023 | 281 | 18 | 36 | 26 | +6.7% | -3.5% |

| 2022 | 263 | 18 | 52 | 24 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 26 | 21 | 4.6 |

| 2024 | 31 | 57 | 28.1 |

| 2023 | 36 | 31 | 22.6 |

| 2022 | 24 | 49 | 22.3 |

Source: SEC companyfacts cache [F1]. *Prior year growth figures estimated where available from data series [F1]

Business Segments and Revenue Drivers

The Enterprise Division remains Franklin Covey’s primary revenue driver by serving business organizations with leadership training subscriptions often renewed annually or multi-year [S17][S26]. These principle-based programs lean heavily on well-known proprietary content such as "The 7 Habits of Highly Effective People." Internationally, this division utilizes direct offices alongside licensees extending reach across Europe, Asia-Pacific, and other key markets.

The Education Practice leverages the Leader in Me framework targeted at schools worldwide aiming to foster better student outcomes through leadership culture changes [S17]. This segment represents a smaller but strategically important growth pillar given rising adoption particularly outside North America.

Subscription-based contracts dominate the revenue mix providing predictable recurring income streams subject to renewal risk which management highlights as critical for financial stability [S1][N1]. Company pricing strategies have been adjusted amid transformations which may affect client renewals both positively (via improved offerings) and negatively (if customers resist pricing changes).

Growth Prospects

Looking forward into fiscal years 2026-27, Franklin Covey is positioning for a return to growth centered on scaling benefits from its recent go-to-market redesigns particularly within North America’s Enterprise segment [S13][N1]. Continued investments into digital product enhancements plus expanded international licensing are expected to broaden addressable markets.

However, growth could be capped by intense competition in professional training markets where barriers to entry remain relatively low and alternative methodologies proliferate rapidly [S1]. Additionally, renewal rates for subscription contracts must remain robust; failure here would directly depress revenue visibility [S1]. Economic uncertainties such as government budget cuts remain ongoing concerns potentially limiting public sector spending.

Forecasts & Milestones

Explicit company guidance for FY2026 has not been publicly detailed beyond quarterly earnings disclosures indicating modest revenue beats but continuing net losses amid high investment phases [N1][S3]. Market watchers should observe quarterly renewal trends, international expansion progress especially licensee performance quality, alongside margin stabilization efforts as main milestones.

The upcoming implementation of recent FASB accounting standards may affect future reporting transparency regarding software development costs impacting intangible asset recognition starting post-2027 [S18].

Capital Allocation & Returns

Franklin Covey generated approximately $29 million in operating cash flow during FY2025 while investing over $8 million back into capital expenditure supporting technology infrastructure upgrades — this translates into roughly $20 million free cash flow available to support financing activities [F1][S21].

Despite compressed profitability, the company continued share repurchase programs at a noteworthy pace totaling $26 million during FY2025 aimed at returning value to shareholders while shares traded below peak levels [F1][S22]. Equity declined moderately reflecting reduced retained earnings resulting from narrower earnings and repurchases.

ROE approximated near five percent in FY25 — sharply down but likely temporary given strategic transitions underway [F1]. Liquidity remains constrained with a current ratio under one (0.63), suggesting tight working capital possibly attributable to timing effects between contract billing cycles versus revenue recognition schedules typical within subscription service businesses [F1][S24]. Management has flagged covenant compliance as an ongoing monitoring area relative to its credit facilities emphasizing careful balancing between debt service obligations and operational funding needs [S4][S24].

Risks & Competitive Landscape

Franklin Covey operates within a fragmented training industry where competitors can quickly innovate new content or delivery models potentially diluting market share [S1][S14]. The company’s moat rests on intellectual property embedded uniquely within signature programs — preservation of these intangible assets through vigilant protection efforts remains vital.

Other prominent risks include cybersecurity threats given dependence on digital course delivery platforms; fluctuations or cuts in governmental educational funding; cross-border regulatory complexities affecting international licensing operations particularly tension-prone markets like China; and potential litigation or contract dispute impacts as disclosed previously [S6][S11][S19][N1].

Industrial practices point out that maintaining high client engagement through tailored coaching services often distinguishes sustainable providers — thus Franklin Covey’s ability to adapt offering mix dynamically is equally crucial alongside classic IP defenses.

Recent Developments

The second quarter of fiscal year 2026 results released April 1 showed losses persisting despite topping revenues estimates—reflecting ongoing expenses related to sales transformation rollouts coupled with delayed margin improvements reported across the Enterprise division segments [N1][N2][S3]. Following this release, the stock price crossed above its key technical support level at the 200-day moving average hinting at stabilization though fundamental challenges are unresolved [N6].

Investor commentary has highlighted valuation discrepancies driven by uncertainty about when operational leverage gains will materialize meaningfully enough to restore pre-transformation profit margins levels amid competitive pressures [N8][N12]. Analysts identify subscriber renewal metrics as primary near-term barometers of health.

Conclusion & Outlook Analysis

Franklin Covey Co manifests a classic mid-cycle transformation profile: facing immediate financial stress manifested by shrinking revenues and profits yet underpinned by strategic initiatives aiming at sustainable competitive repositioning through enhanced sales frameworks plus expanded international channels.

Key watch points include client retention trends on subscription products pivotal for recurring revenues; deployment success of new digital tools accompanying principle-based content updates; regulatory developments impacting global operations; alongside prudent liquidity management under debt covenant scrutiny.

While risks abound notably from industry rivalry and funding variability especially public sector spending policies—the company’s heritage brands like “The 7 Habits” retain strong cultural cachet offering durable franchise value if successfully modernized away from textbook distribution towards integrated learning ecosystems.

This report is prepared solely for informational purposes without any recommendation or investment advice implied or expressed regarding Franklin Covey Co securities or potential transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments