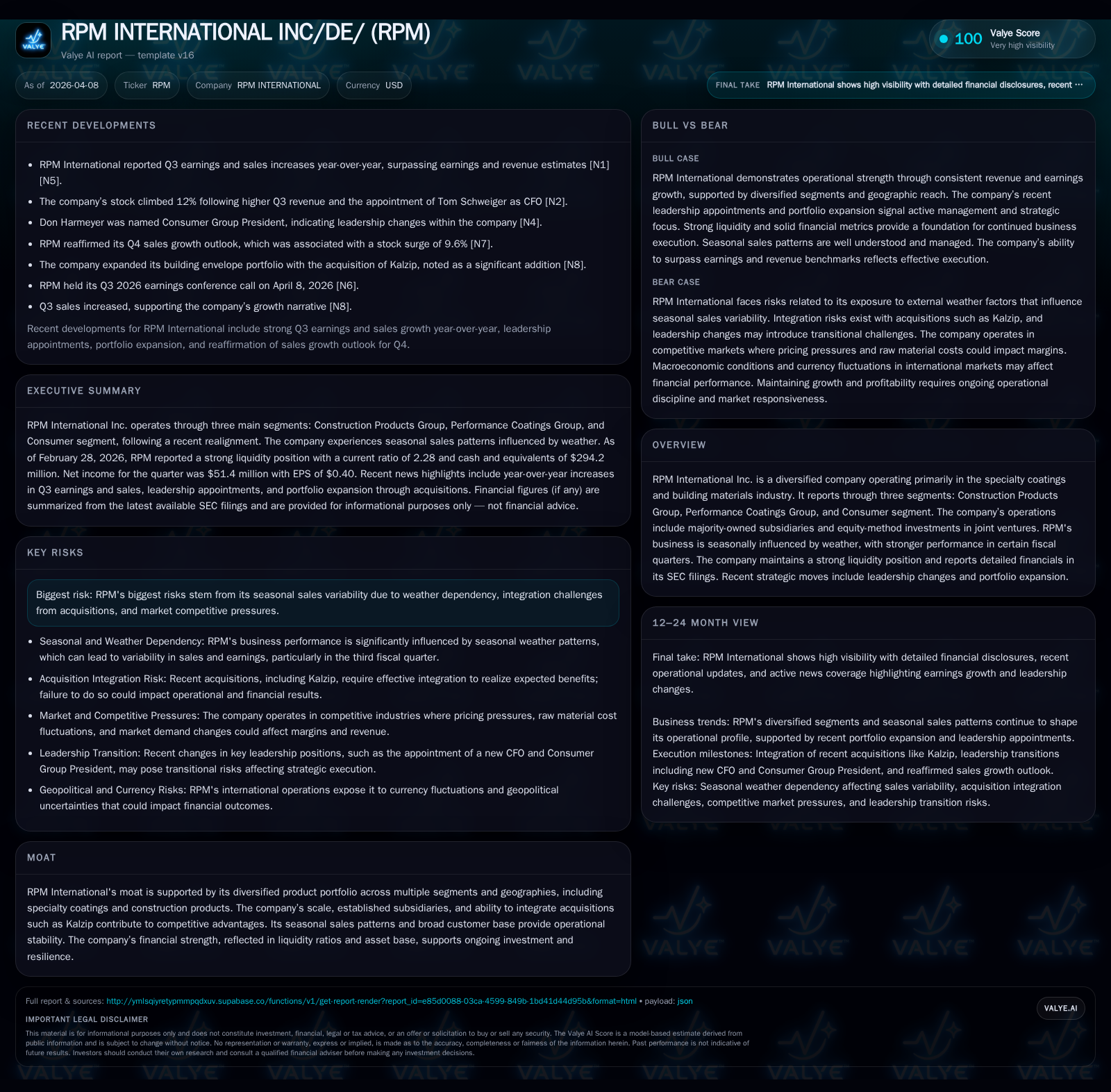

How RPM’s Diversified Segments and Capital Strategy Support Sustainable Growth

RPM International leverages its multi-segment specialty coatings portfolio and disciplined capital management to underpin robust financial performance and growth potential.

RPM International exhibited notable revenue and net income growth in its recent fiscal year, buoyed by demand across its Construction Products, Performance Coatings, and Consumer segments. The company has appointed new leadership in key financial and consumer unit roles, signaling a strategic focus on operational efficiency and market expansion. Despite seasonal sales variability tied to weather and integration of acquisitions like Kalzip, RPM maintains strong liquidity and capital allocation discipline, evidenced by consistent dividends and measured buybacks. Investors should monitor Q4 sales outlook and integration progress to gauge ongoing momentum.

Revenues Ascend: Growth Drivers Behind Recent Performance

RPM International closed FY2025 with a net income of nearly $689 million, marking an appreciable 17% increase over the prior year’s $588 million figure [F1]. This upward trajectory is attributed mainly to resilient demand across RPM’s diversified product base encompassing specialty coatings and building materials. Notably, the operating cash flow dipped by approximately 31.6% from FY2024’s $1.12 billion to $768 million in FY2025 [F1]. While this contraction warrants attention, it was offset by sustaining free cash flow above $538 million post-capital expenditures. The cash allocation balanced capex growth (up 7.5% YoY) supporting asset modernization against liquidity preservation.

The company's revenue streams are subject to seasonality driven by weather fluctuations affecting construction activities—conditions that historically amplify Q2/Q3 performance strength but increase volatility risks around other quarters [valye_report_excerpt.risks][S2]. Nonetheless, RPM managed to exceed consensus estimates for Q3 sales and earnings per share, catalyzing a more than 12% stock price lift upon announcement [N1][N2][N4].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 689 | 768 | 230 | +17.0% |

| 2024 | 588 | 1122 | 214 | +22.9% |

| 2023 | 479 | 577 | 254 | -2.6% |

| 2022 | 491 | 179 | 222 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 256 | 70 | 538 |

| 2024 | 232 | 55 | 908 |

| 2023 | 214 | 50 | 323 |

| 2022 | 204 | 53 | -44 |

Source: SEC companyfacts cache [F1].

Table: RPM's financial summary highlights fiscal years showing steady net income growth amid fluctuating cash flows.

Segment Dynamics: Construction, Performance Coatings, and Consumer Insights

RPM structures its operations into three primary segments: Construction Products Group (CPG), Performance Coatings Group (PCG), and Consumer segment [S25]. The CPG segment continues to benefit from portfolio expansions such as the latest acquisition of Kalzip—a provider of standing seam metal roofing solutions—broadening RPM's footprint in the high-growth building envelope niche [N10]. This bolsters the company’s capacity to serve architects and contractors focusing on sustainable design.

The Performance Coatings segment maintains strength through specialty chemical formulations tailored to industrial applications and protective coatings. Meanwhile, the Consumer unit is repositioning under new leadership aimed at enhancing brand reach within renovation and maintenance markets where end-user preferences are rapidly evolving [N7]. Together these segments offer resilience against demand swings typically tied to macroeconomic cycles impacting traditional construction timelines.

Geographically diverse operations spanning North America and Europe also contribute to risk mitigation by balancing regional construction market maturity differences [S25]. The integrated approach allows cross-leveraging manufacturing capabilities while adapting product offerings to local standards—a key competitive moat element noted in RPM's latest disclosures [valye_report_excerpt.moat].

Leadership Transitions: New CFO and Consumer Group President Implications

April 2026 saw RPM announce strategic leadership changes with Tom Schweiger appointed CFO alongside Don Harmeyer's elevation as President of the Consumer Group [N7]. Schweiger brings attention toward refining financial processes and capital deployment strategies which investors interpreted positively amid growing concerns about managing working capital efficiently given shifts seen in operating cash flows.

Harmeyer's experience in consumer-facing businesses signals an intensified focus on driving innovation and customer-centric initiatives within that segment—critical for capturing discretionary spending trends linked to home improvement cycles that can be less predictable than commercial contracts.

These leadership moves resonated well with market watchers triggering a stock price surge confirming investor confidence in RPM's ability to integrate operational improvements with sustainable growth ambitions [N1][S3].

Risks Amid Seasonality and Acquisition Integration Challenges

Despite diversification benefits across product lines and geographies improving overall stability at RPM International there remain inherent risks tied first to cyclical weather impacts—their sales cycles closely track construction activity peaks influenced by climate variations causing quarter-to-quarter volatility.

Secondly integration challenges following acquisitions like Kalzip demand meticulous management attention to harmonize supply chain logistics along with cultural assimilation within RPM’s decentralized operating structure. Failure here could erode margins or distract management focus away from organic growth drivers [valye_report_excerpt.risks][valye_report_excerpt.moat].

Understanding that this weather-driven seasonality introduces an earnings cadence distinct from more linear industrial suppliers is crucial when evaluating quarterly results.

Capital Allocation Discipline: Dividends, Buybacks, and Cash Flow Trends

RPM maintains a conservative capital allocation framework emphasizing shareholder returns balanced against reinvestment needs. Dividends paid totaled roughly $256 million for FY25 reflecting a per-share payout increase consistent with long-term policy aimed at stable income delivery [F1][S4][S13]. Concurrently share repurchases amounted to approximately $70 million over the same period.

The company’s operating cash flow contraction during FY25 contrasts with rising capex demands; yet free cash flow remains healthy at over half a billion dollars—affirming sufficient liquidity coverage for ongoing dividend commitments plus incremental debt service requirements given total liabilities nearly matching assets but backed by strong equity base [$2.89 billion] resulting in an ROE near 24% when measured against net income for FY25 [F1].

Moreover liquidity measures such as a current ratio north of 2.2x highlight ample short-term solvency providing discretionary maneuverability absent excessive leverage pressures common in cyclically sensitive industrials [F1][S8][S15]. The balance sheet fortitude enables selective bolt-on acquisitions or R&D funding supporting product innovation central to sustaining market position.

What to Watch: Upcoming Milestones and Market Expectations

Looking ahead into calendar Q4 2026 time frame management has reaffirmed positive sales growth outlook reflecting confidence in pipeline robustness alongside seasonally supportive factors continuing into spring construction ramp-ups [+9.6% stock move on guidance confirmation] [N8][N11]. If realized this would extend the recently gained momentum derived from Q3 beats driving improved full-year earnings expectations.

Observers should track how effectively integration synergies materialize post-Kalzip acquisition along with monitoring any emerging headwinds tied to raw material inflation or geopolitical trade disruptions impacting supply chain resilience typical for chemicals-dependent producers.

Additionally evolving consumer preferences shaping renovations versus new builds offer fertile ground for innovation-led wins within the Consumer segment administration under new leadership.

Finally currency translation effects remain relevant given RPM’s multinational exposure potentially impacting reported results versus operational realities.[S25]

In summary RPM International’s demonstrated ability to harness its diversified product portfolio balanced with prudent capital deployment under refreshed leadership bodes well for sustaining long-term growth amidst industry cyclicality. However mitigating weather-driven seasonality impacts combined with successful acquisition integrations remain critical watchpoints as the company navigates its next phases.

This analysis is based solely on reported data sources cited herein without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments