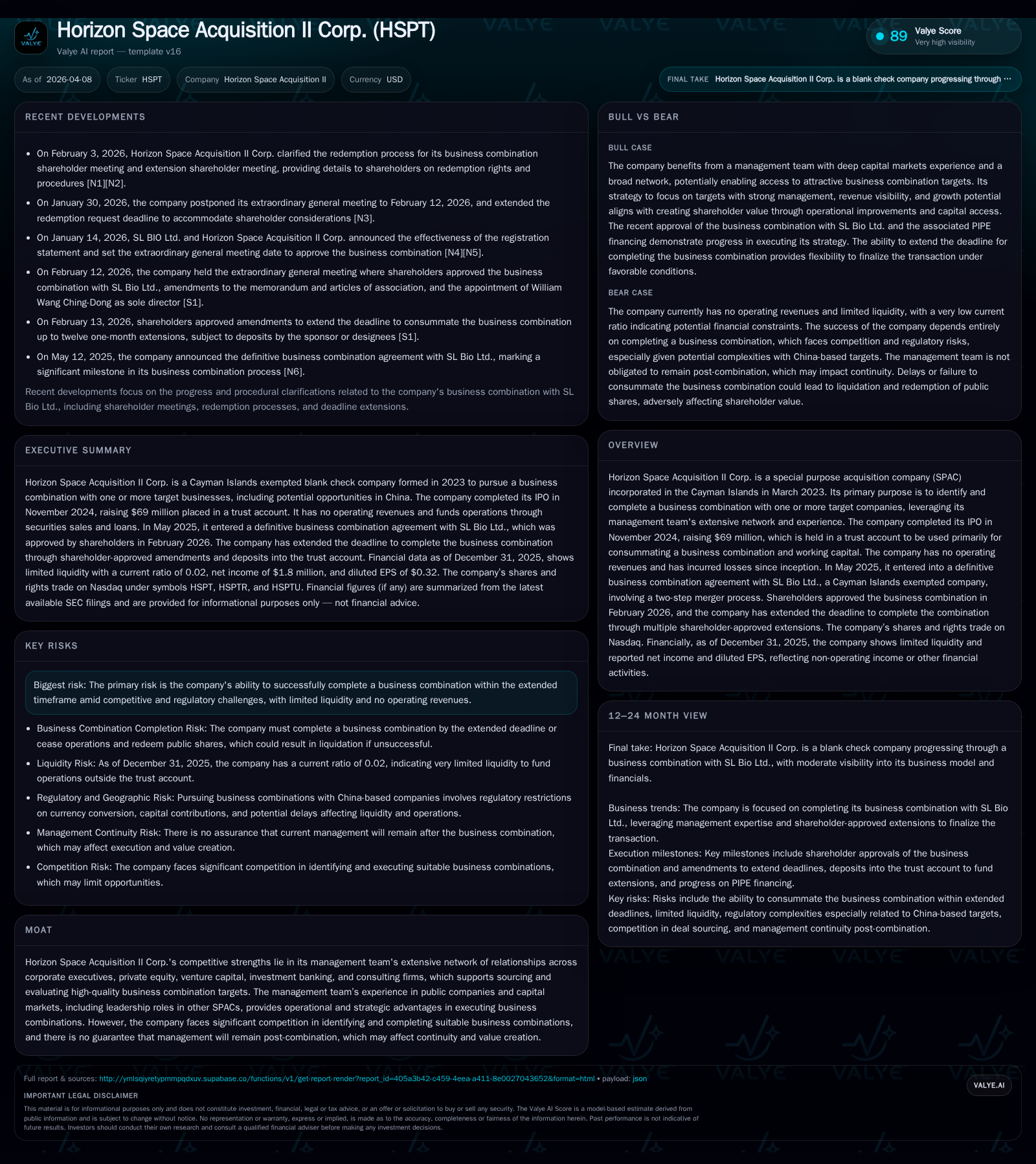

Horizon Space Acquisition II Corp.'s Transition From SPAC to Public Entity: Financial and Strategic Outlook

An examination of Horizon Space Acquisition II Corp.'s financial history as a SPAC, its strategic merger with SL Bio Ltd., and evolving capital priorities amid regulatory and competitive challenges.

Horizon Space Acquisition II Corp., incorporated as a Cayman Islands-based SPAC in March 2023, raised $69 million in its November 2024 IPO, placing proceeds in a trust account for a business combination. The company's historic financials show net income growth driven by one-time items but deteriorating operating cash flows and increasing negative equity. Its strategic focus centers on a two-step merger with SL Bio Ltd., approved by shareholders in February 2026, marking a critical inflection point. Multiple deadline extensions backed by sponsor and CEO deposits highlight liquidity management complexities amid shareholder redemptions. Post-combination governance uncertainty and stiff competition to secure quality targets remain material risks to value creation.

SPAC Origins and Capital Formation: November 2024 IPO Overview

Horizon Space Acquisition II Corp. was established as an exempted Cayman Islands blank check company on March 21, 2023 [S1]. Its initial public offering took place on November 18, 2024, issuing 6 million units at $10 per unit for gross proceeds of $60 million. Each unit included one ordinary share and one right to acquire one-tenth of an ordinary share upon completion of a business combination. Concurrent private placements to the Sponsor added $2 million via an additional 200,000 units priced identically. Subsequently, the underwriters exercised their overallotment option fully by acquiring 900,000 units for $9 million in late November alongside a small additional private placement [S1][S4][S14].

In total, the gross proceeds reached approximately $69 million that have been placed into a segregated trust account managed by Wilmington Trust to be preserved primarily for consummating a business combination and related working capital needs [S1][S4]. This trust structure is consistent with standard SPAC mechanics designed to protect public shareholders' funds until deployment towards transactions.

Historic Financial Snapshot: Losses, Net Income Surge, and Operating Cash Flows (2024-2025)

The company has no operating revenues since formation nor does it intend to generate standalone revenues prior to completing a merger [S1][S4]. Its financial profile is typical for a SPAC at this development stage—incurring formation costs and administrative expenses resulting in operational losses.

Notably, net income jumped markedly year-over-year from $142,877 in FY2024 to $1.81 million in FY2025 (+1166%) [F1]. This spike largely reflects one-time financial events rather than core profit generation. Conversely, operating cash flow deteriorated sharply from -$110K to -$1.04 million (-840%) year-over-year [F1], signaling increasing cash burn related to ongoing activities.

Equity transitioned from positive $451K at end-2024 to negative $1.32 million by end-2025 [F1], producing an effective return on equity near -137%, underscoring deepening net liabilities possibly tied to accumulated losses or debt issued for operational funding [F1].

Historical performance (annual)

| FY | Net ($) | CFO ($) | Net YoY |

|---|---|---|---|

| 2025 | 1809006 | -1038803 | +1166.1% |

| 2024 | 142877 | -110465 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -137.1 |

| 2024 | 31.7 |

Source: SEC companyfacts cache [F1].

Strategic Path to Growth: Business Combination with SL Bio Ltd.

On May 9, 2025, Horizon entered into a definitive business combination agreement with SL Science Holding Limited (PubCo), involving SL Bio Ltd., structured as a two-step merger whereby Merger Sub I merges into Horizon followed by Merger Sub II merging into SL Bio as the surviving entity [S22][S19]. Upon closing—expected soon after shareholder approval granted February 12, 2026—both Horizon and SL Bio would become subsidiaries of PubCo whose shares will be listed on Nasdaq [S22][S19]. This transaction represents Horizon’s first significant step transitioning away from SPAC status toward becoming an operating public company.

Navigating Capital Structure and Liquidity Amid Deadline Extensions

Originally set to complete the business combination by February 18, 2026 [S20], Horizon faced delays necessitating several deadline extensions approved by shareholders at extraordinary general meetings. These were financed via unsecured promissory notes backed by deposits totaling $790K made by Hsiao-Lan Wu (Sponsor designee) and William Wang (SL Bio CEO) between late 2025 and March 2026 [S7][S20]. Despite these injections easing imminent liquidity strains somewhat, balance sheet data highlights starkly tight liquidity: current assets at just under $30K versus current liabilities exceeding $1.3M at FY-end December 31, 2025 yield an alarming current ratio around 0.02 [F1][S7].

Shareholder redemptions further reduced capital; notably more than three million shares redeemed during extension votes dilute available financial resources for closing and integration costs [S7][S20]. These moves reflect delicate cash management imperative as Horizon races against contractual liquidation triggers.

Capital Allocation Focus: Trust Account Management, Sponsor Loans, and Shareholder Redemptions

Consistent with SPAC norms observed here ([S4],[S8],[S11],[F1]), Horizon’s capital allocation prioritizes preservation of trust account funds almost exclusively for consummation of the business combination and minimal working capital needs before closing. No dividends or share repurchase programs have been initiated pending completion.

Supplemental funding beyond trust proceeds has come through issuance of private units sold to the Sponsor alongside working capital loans convertible into units post-merger if exercised [S8][S18]. The restricted use of trust assets combined with loan-financed extensions underscore management's cautious deployment strategy given uncertain timing.

Governance and Management Continuity Concerns Post-Combination

Horizon touts competitive strengths rooted in its management team's broad industry networks across private equity and investment banking realms aiding target sourcing and evaluation [S10][S1]. Management also brings past SPAC leadership experience coupled with ties that may facilitate capital market operations following business combination.

Nonetheless competition amongst numerous SPAC vehicles vying for similar high-quality targets remains intense — threatening premium valuations or prolonged search periods [S10]. More structurally challenging is the lack of assurance that existing management will continue post-merger; lower continuity may impair integration momentum or strategic execution within PubCo’s new operational framework [S1][S10].

Key Risks: Completion Uncertainty, Competitive Pressures, and Regulatory Environment

A principal risk remains whether Horizon can consummate its initial business combination before exhausting permissive extensions — failure would trigger liquidation returning invested capital pro-rata to shareholders but extinguishing sponsor equity stakes as worthless [S16][S20][S27]. Such deadline pressure invites considerable execution risk.

Additional regulatory complexities stem from potential China-linked transactions where foreign exchange limitations or government approvals could delay or constrain operations or distributions after closing (post-merger entities are expected to maintain ties with Chinese jurisdictions including Hong Kong and Macau) [S23][S24][S25]. Enforcement challenges emerge given key officers reside outside U.S., complicating legal recourse if compliance issues arise [S21].

Lastly market saturation in SPAC pipelines seeking similar opportunities exacerbates competitive tension over target valuations placing downward pressure on acquisition multiples or prolonging deal timelines [S10].

Analyst’s Watchlist: Milestones to Track Beyond the Merger Close

Absent explicit guidance on deal closing dates beyond April extensions provided by unsecured note-backed deposits ([S7],[S20]), close monitoring should focus on:

- Finalized completion date of SL Bio mergers post-April 18th deadline,

- Closing of committed PIPE financing aggregating approximately $7.8 million as part of broader transaction funding,

- Redemption activity levels that will influence net equity base outstanding,

- Confirmation of post-merger management appointments especially directorship changes,

- Evolving leverage metrics once combined entity reports publicly post-close.

These milestones will materially affect Horizon’s strategic trajectory as it transitions from special purpose acquisition vehicle into an operating public enterprise.

This analysis is based solely on information available from official SEC filings up to April 8th, 2026 ([F1], [S#]) without speculation or forward-looking statements outside documented disclosures. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments