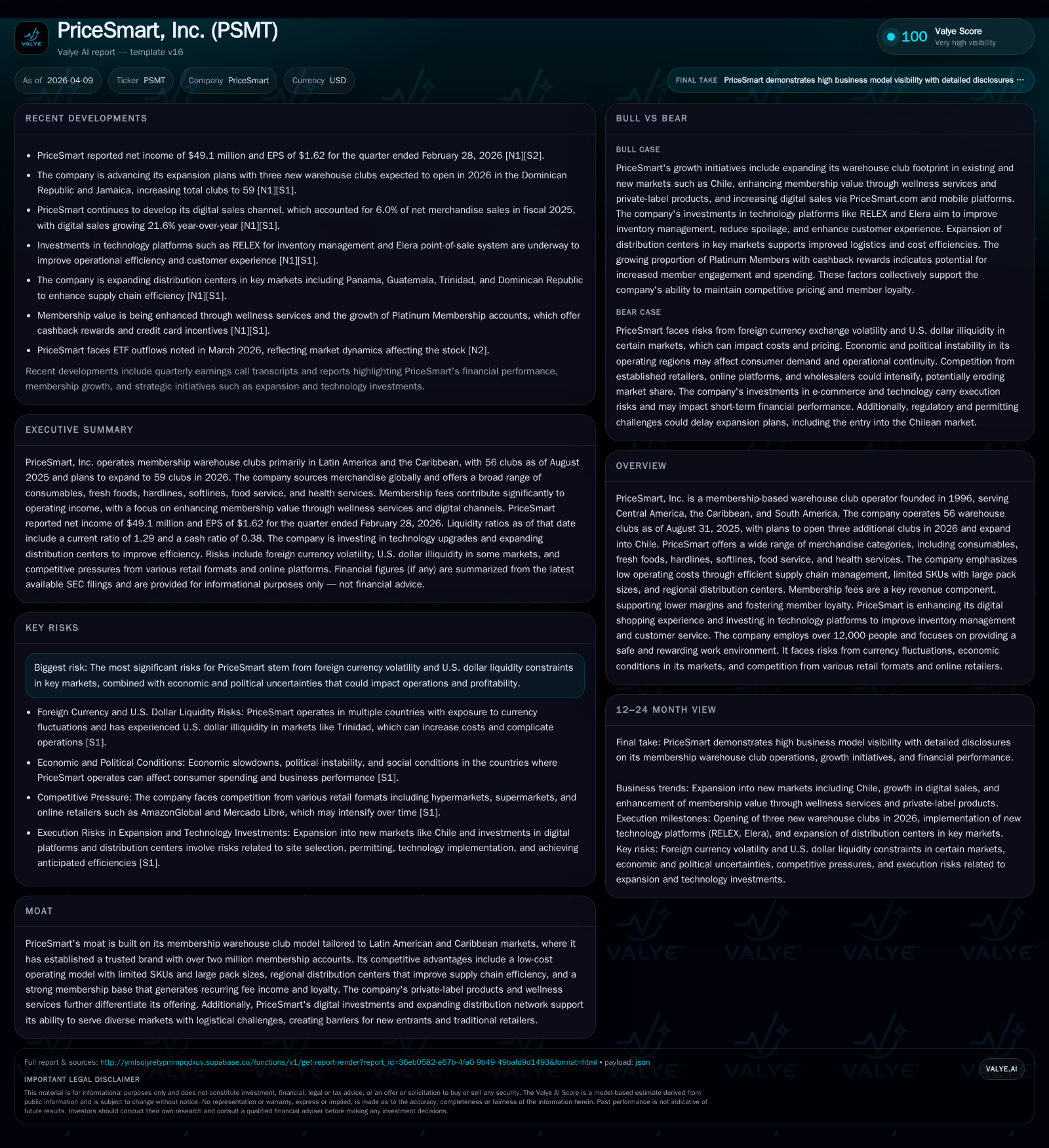

PriceSmart Inc's Growth Tracks Membership Loyalty and Regional Expansion Amid Currency Challenges

PriceSmart leverages its membership warehouse club model to drive steady growth while navigating currency volatility and market expansion hurdles.

PriceSmart, a U.S.-style warehouse club operator deeply embedded in Latin America and the Caribbean, has demonstrated consistent revenue and profit growth supported by an expanding membership base and regional expansion. Its low-cost operating model, combined with technological investments and enhanced membership services, underpins its competitive positioning. However, foreign currency fluctuations and U.S. dollar liquidity constraints in key markets pose ongoing risks. The company plans to increase warehouse club count to 59 by end-2026 and expand into Chile while focusing on elevating membership value through digital channels and wellness services. Capital allocation reflects modest dividends and limited buybacks amid targeted reinvestment.

Historical Performance

PriceSmart has enjoyed a steady trajectory of revenue growth, evidenced by a rise from approximately $3.23 billion in fiscal year (FY) 2019 to over $4.06 billion in FY2022[F1]. Operating income grew even more impressively from about $167 million in FY2022 to $232 million in FY2025, marking a compound improvement which underscores operational efficiencies and expanding scale[F1]. Net income followed suit with a solid increase reflecting improved margins despite inflationary pressures experienced in certain markets.

This growth stems principally from two pillars: expanding warehouse club footprint across twelve countries and one U.S. territory, and developing membership fee contributions that now constitute roughly 37% of operating income[S1][S12]. PriceSmart's controlled SKU count with large pack sizes reduces labor costs, while its regional distribution centers enhance supply chain stability—a critical advantage given infrastructural challenges typical of its markets[S8][S11][S16].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 148 | 261 | 233 | 158 | +6.5% |

| 2024 | 139 | 208 | 221 | 169 | +27.2% |

| 2023 | 109 | 257 | 185 | 143 | +4.5% |

| 2022 | 105 | 122 | 167 | 121 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 39 | 7 | 103 |

| 2024 | 66 | 73 | 39 |

| 2023 | 29 | 115 | |

| 2022 | 27 | 1 |

Source: SEC companyfacts cache [F1].

Figures rounded; 'OpInc' = Operating Income; 'CFO' = Operating Cash Flow; 'Capex' = Capital Expenditures

Drivers Behind Past Growth

The key driver fueling historical growth is PriceSmart’s membership business model tailored for Latin American and Caribbean consumers who seek value-oriented bulk purchasing options anchored by the U.S.-style warehouse club experience[S1][S18]. This format is relatively unique within their markets, where traditional retail formats dominate but do not offer equivalent scale or pricing leverage.

Increased memberships—over two million documented as of August 31, 2025—and specifically the expansion of premium Platinum memberships with cashback rebates have propelled comparable sales gains by enhancing customer loyalty and spend[S12][S16]. Furthermore, investments in technology platforms aimed at digitizing the shopping experience (mobile apps, online ordering via PriceSmart.com with home delivery/curbside pickup) extended reach beyond physical stores[S18][N1].

A noteworthy contributor is also geographical expansion: maintaining steady club counts domestically but enhancing presence through new clubs opened each year—increasing from 54 to 56 clubs between FY2024 and FY2025—and preannounced additions for FY2026[S1][S24]. The commencement of regional distribution centers optimized inventory flow amid persistent logistical challenges intrinsic to emerging markets.

Future Growth Prospects

The roadmap ahead features three primary engines:

Club Expansion: Plans are underway to open three new clubs during fiscal year ending August 31, 2026—one in La Romana (Dominican Republic) and two in Jamaica—bringing total locations to nearly sixty[S1][S24]. Beyond immediate openings, the firm is advancing plans into Chile—a new country marked as an attractive target where the membership warehouse club concept is nascent but potentially scalable[S1][S24].

Elevating Membership Value: PriceSmart aims to deepen engagement via increasing membership benefits including health-related services such as optical, audiology, pharmacy operations alongside private-label product expansion under the "Member’s Selection" brand that carries higher margins[S12][S16]. The Platinum membership tier penetration grew from roughly 12% to nearly 18% over one year illustrating success in upselling[S16]. Additionally, fee increases have been executed selectively since fiscal year 2024.

Digital Channel Enhancement: Accelerating investments into e-commerce infrastructure including mobile app modernization to native iOS/Android architectures fosters faster deployment of features intended to reduce friction points at checkout and enhance payment options through an upgraded point-of-sale system (Elera)[S17]. This mirrors broader omnichannel retail trends increasingly important given competitors such as AmazonGlobal and Mercado Libre encroaching logistic services within these regions[S20].

However, some factors could constrain growth:

- Currency Volatility & Dollar Liquidity Constraints: Approximately eighty percent of PriceSmart’s sales occur outside the U.S., predominantly denominated in local currencies highly susceptible to devaluation versus the dollar—a fundamental risk amplified by intermittent shortages of USD liquidity impairing payment cycles for imported goods[S1][S14]. The company has resorted to debt financing for Trinidad operations where central bank controls generate chronic illiquidity issues impacting balance sheet composition.[F1][S5]

- Political & Socioeconomic Turbulence: Recurring protests (notably Panama in late FY2025) disrupt store access; similar instability has hit Guatemala and Colombia recently.[S14]

- Competitive Environment: While no direct US-style warehouse club rivals currently exist locally, competition arises from supermarkets, hypermarkets corporate chains such as Walmart Central America or Grupo Éxito Columbia as well as emerging e-commerce platforms.[S20]

Financial Outlook & Milestones

While explicit forward guidance was not disclosed beyond operational milestones like store openings announced for fiscal years ending August '26/'27[N1][S1], investors should monitor:

- Execution progress on Chile entry plans.

- Platinum membership growth rate.

- E-commerce sales contribution relative to brick-and-mortar.

- Foreign currency exchange impacts tied to socio-political developments.

- Adoption pace of new POS systems across markets.

These will serve as significant indicators for sales momentum, cost control leverage, and overall service value enhancement that underpin profitability.

Returns & Capital Allocation

PriceSmart exhibits solid operating cash flow generation with CFO rising from $121 million (FY22) to $261 million (FY25), allowing sustained reinvestment[F1]. Capital expenditures remain elevated reflecting network expansion but declined slightly (-6%) in latest reported period indicating stabilization after prior growth sprees.

Free cash flow stayed positive ($103 million annually recently), facilitating modest dividend payouts which showed variability but latest figures illustrate ongoing returns ($39 million paid in FY25)[F1]. Buybacks are minimal relative to dividends suggesting preference toward organic investment over shareholder distributions.

Equity has grown alongside profitability gains lifting approximately from $991 million (FY22) to $1.25 billion (FY25)[F1], underpinning an approximate return on equity near ~11.9%, reflective of efficient capital deployment within a moderate-margin business model emphasizing volume-driven scale.[F1]

Sector-Native Observations

Warehouse clubs traditionally rely on tight inventory management combined with streamlined distribution logistics—which PriceSmart achieves through its multiple regional centers strategically located near clustered warehouses enabling bulk freight consolidation—a critical advantage when serving geographically fragmented Latin America-Caribbean markets where transport infrastructure frequently lags developed-country standards.

Moreover, digital payment integration along with loyalty rewards increasingly defines customer retention benchmarks globally within warehouse formats; PriceSmart's phased implementation of advanced POS systems aligns it competitively against formidable e-commerce players embedding delivery capabilities across similar territories.

Conclusion

PriceSmart represents a resilient niche player leveraging an established U.S.-style warehouse club platform tailored for emerging Latin American and Caribbean economies where it retains substantial market trust reflected in sizeable membership penetration. The company's steady clinic of new store openings and digital enhancements paired with emphasis on health-related services signify a thoughtful evolution rather than disruptive overhaul.

Its core risk vector remains systemic: currency instability paired with political unrest normalizes within its market context but mandates consistent operational agility supported by strong balance sheets bolstered via prudent liquidity management. Navigating these factors will define PriceSmart's capacity to sustain profit growth while investing strategically beyond traditional geographies such as Chile.

This analysis is based solely on information publicly available as of April 9, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments