ProAssurance Corp. Edges Forward While Steering Major Merger Integration

ProAssurance sustains underwriting rigor and operational improvements in 2025 amid a pivotal merger process.

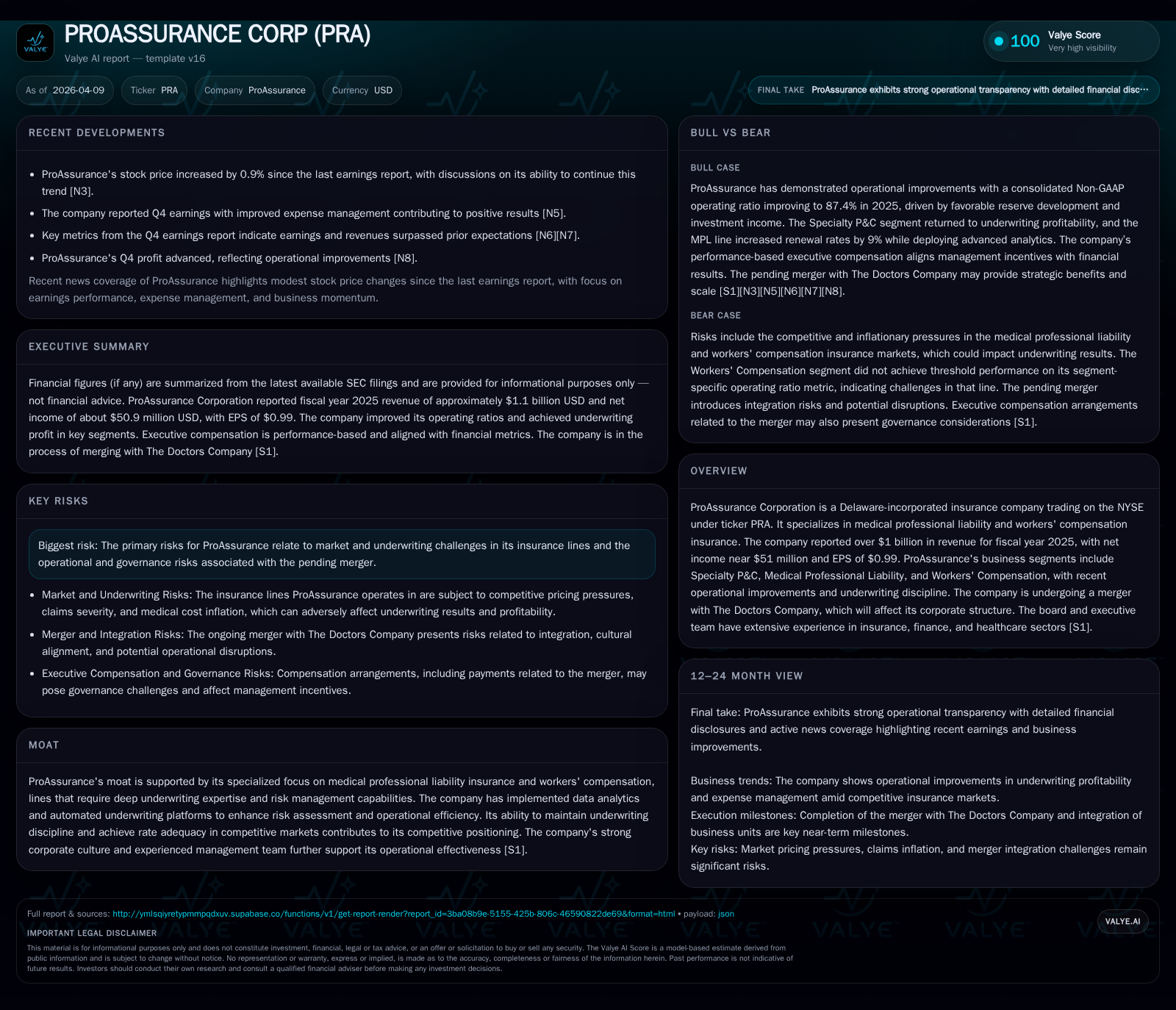

ProAssurance Corporation maintains a specialized focus on medical professional liability and workers’ compensation insurance, reporting $1.10 billion in revenue and $51 million in net income for fiscal 2025, with a slight revenue decline but improved underwriting results. Operational efficiencies have contributed to better combined and operating ratios despite ongoing challenges reflected in negative operating cash flows. The company is navigating integration risks related to its pending acquisition by The Doctors Company, with regulatory approvals progressing. Capital returns have moderated, influenced by merger-related prudence, while executive incentives remain aligned with shareholder interests through performance-based equity compensation.

Evolution of Revenue and Profitability: A Historical Perspective

ProAssurance Corporation’s recent annual financials illustrate a nuanced performance trajectory characterized by modest top-line contraction alongside stabilized profitability. According to SEC filings [F1], fiscal year 2025 revenue stood at approximately $1.10 billion USD—a decline of about 4.6% from the $1.15 billion realized in 2024. This reduction likely reflects ProAssurance’s disciplined approach to underwriting and pricing within highly competitive medical professional liability (MPL) and workers' compensation markets.

Net income for 2025 was reported near $51 million USD, down marginally by roughly 3.5% from prior year earnings of $52.7 million USD but significantly improved compared to losses recorded in preceding years (net losses in both 2022 and notably 2023). This pattern signals effective normalization of earnings under an evolved risk profile.

However, operating cash flow numbers expose a contrasting liquidity pressure: negative cash flow from operations totaled roughly -$25.6 million USD for the same period, worsening compared to -$10.7 million USD in 2024 [F1]. This divergence suggests that while accounting profits were retained on paper, underlying reserve dynamics or claim payment schedules may have impacted actual cash-generating capacity typical for long-tail specialty lines.

Capital expenditures have remained stable around prior modest levels with no significant deviation documented recently; historical capex hovered near $9–10 million annually though this is less material relative to operational outlays [F1]. The broader financial health perspective reveals a firm cautiously managing growth amid prevailing market headwinds.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1098 | 51 | -26 | -4.6% | -3.5% |

| 2024 | 1150 | 53 | -11 | +1.2% | +236.6% |

| 2023 | 1137 | -39 | -50 | +2.8% | -9503.0% |

| 2022 | 1107 | 0 | -30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 3.8 | |

| 2024 | 0 | 4.4 | |

| 2023 | 5 | 50 | -3.5 |

| 2022 | 11 | 3 | -0.0 |

Source: SEC companyfacts cache [F1].

Note: All figures rounded to nearest million USD except percentages.

Specialty Insurance Focus: Underwriting Discipline as a Competitive Edge

ProAssurance’s enduring competitive advantage remains tightly linked to its focus on specialized P&C insurance sectors—specifically medical professional liability and workers’ compensation. As outlined within the company’s latest Form 10-K/A [S1], the firm emphasizes rigorous underwriting discipline as essential to sustaining rate adequacy amidst market volatility.

Advanced deployment of data analytics and implementation of automated underwriting platforms enable granular risk assessment that reinforces loss ratio control – critical factors given the complexity of claim reserves inherent to MPL insurance where tail risk exposures can manifest years post-issue.

By maintaining tight control over policyholder selection criteria and pricing margins (rate adequacy), ProAssurance mitigates adverse loss emergence, thereby protecting underwritten portfolios from erosion due to unanticipated claims inflation or judicial shifts.

This strategic posture supports consistent policyholder retention and fortifies operational resilience even as competitors may seek growth via relaxed underwriting standards which historically result in elevated combined ratios detrimental over time.

Analysis of Recent Earnings Surprises and Operational Efficiencies

Quarterly disclosures during late 2025 underscore incremental gains through expense management initiatives. Earnings releases reported notable cost containment contributing to quarterly results surpassing analyst consensus estimates [N5][N6][N7][N10].

These margin improvements reflect ongoing efforts within ProAssurance’s core segments—Specialty P&C, Medical Professional Liability, and Workers' Compensation—to enhance operational leverage through process streamlining and technology investments fostering administrative efficiency.

However, these gains occur against a backdrop of relatively flat or declining revenues, highlighting that revenue growth does not drive performance uplift directly; rather, tighter cost structures bolster bottom-line strength during transition phases such as those associated with mergers.

The sustainability of such efficiencies merits close watch as merger-related distractions could temporarily impair execution focus or integration synergies.

Merger Developments: Risks and Strategic Opportunities Ahead

Since March 2025, ProAssurance has been engaged in a transformative transaction — merging with The Doctors Company — a reciprocal inter-insurance exchange specializing also in medical malpractice coverage [S8][S9][S11].

Regulatory scrutiny has been rigorous yet constructive; early termination of antitrust waiting periods occurred July 2025 with several state insurance departments granting final approvals by early 2026 including Alabama, Illinois, Texas among others. Nevertheless, reviews remain pending in California and Pennsylvania — jurisdictions representing material business segments introducing timing uncertainty.

The merger adds complexity through potential disruptions such as key personnel retention risks, litigation contingencies including derivative suits common in large insurer consolidations, possible temporary brand dilution effects, plus management bandwidth diversion toward integration logistics rather than organic operations.

Strategically though, the alignment expands scale within niche medical professional liability markets while leveraging complementary underwriting expertise — creating opportunities for data sharing innovations and portfolio optimization post close.

Investors benefit from awareness that closing conditions remain subject to regulatory discretion; thus timing expectations currently anticipate completion mid-2026 but remain fluid depending on outstanding jurisdictional review outcomes [S22].

Capital Deployment: Assessing Returns, Cash Flows, and Shareholder Rewards

The company’s return on equity calculates to approximately 3.8% for fiscal 2025 using net income over year-end equity figures (approximated from reported $51 million NI vs $1.35 billion equity) [F1]. This level reflects modest profitability relative to insurance sector peers often targeting double-digit ROE ranges but aligns with conservative capital management approaches under merger uncertainty.

Cash flow analysis reveals persistent negative operating cash flow (-$25.6 million) compounded by routine capex outlays (~$9 million) resulted in negative free cash flow circa -$35 million USD annually [F1]. This deficit suggests reinvestment needs or reserve strengthening limiting discretionary capacity for capital returns.

Indeed dividends were suspended since FY2024 onward—consistent with precautionary measures during strategic transitions [F1; S12-S15]. Earlier years exhibited moderate share repurchases (approximately $50 million in 2023) but no buybacks were recorded recently; reflecting a pause on capital return activities until merger consummation clarifies future structure.

Executive incentives further align management pay with shareholder value creation metrics including Relative Total Shareholder Return versus S&P Composite P&C Index alongside cumulative operating ROE benchmarks over multi-year periods .

Outlook: Measuring Growth Headwinds and Potential Catalysts

Market commentary highlights investor cautious optimism given earnings beats tempered by near-flat revenue profiles [N3]. Risk disclosure incorporated from recent filings underscores contingencies linked tightly to merger completion timelines alongside evolving regulatory landscapes impacting insurance product pricing frameworks [S1; S16].

Core catalytic factors going forward include maintaining underwriting discipline amidst competitive pressure where failure to uphold rate adequacy could materially affect loss ratios; realization of operational integration benefits post-merger; capitalizing on expanded data analytics capabilities to improve claim reserving accuracy; plus regulatory approvals enabling full transaction closure without onerous conditions.

Watch points also comprise potential latent litigation arising from transaction challenges beyond announced filings which could impose unanticipated costs or distract senior leadership during critical execution phases.

Thus operational milestones like combined ratio progression post-close, net investment returns stability amid fluctuating yields on fixed income portfolios—typical driver of insurer profitability—and scaling workforce talent retention policies represent key indicators for assessing forward momentum.

Disclaimer:

This analysis is based exclusively on public disclosures up to June 2026 and does not constitute investment advice or financial recommendation. Readers should consider the effect of emerging events subsequent to this report independently before forming any opinions regarding ProAssurance Corporation's securities or strategic direction.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments