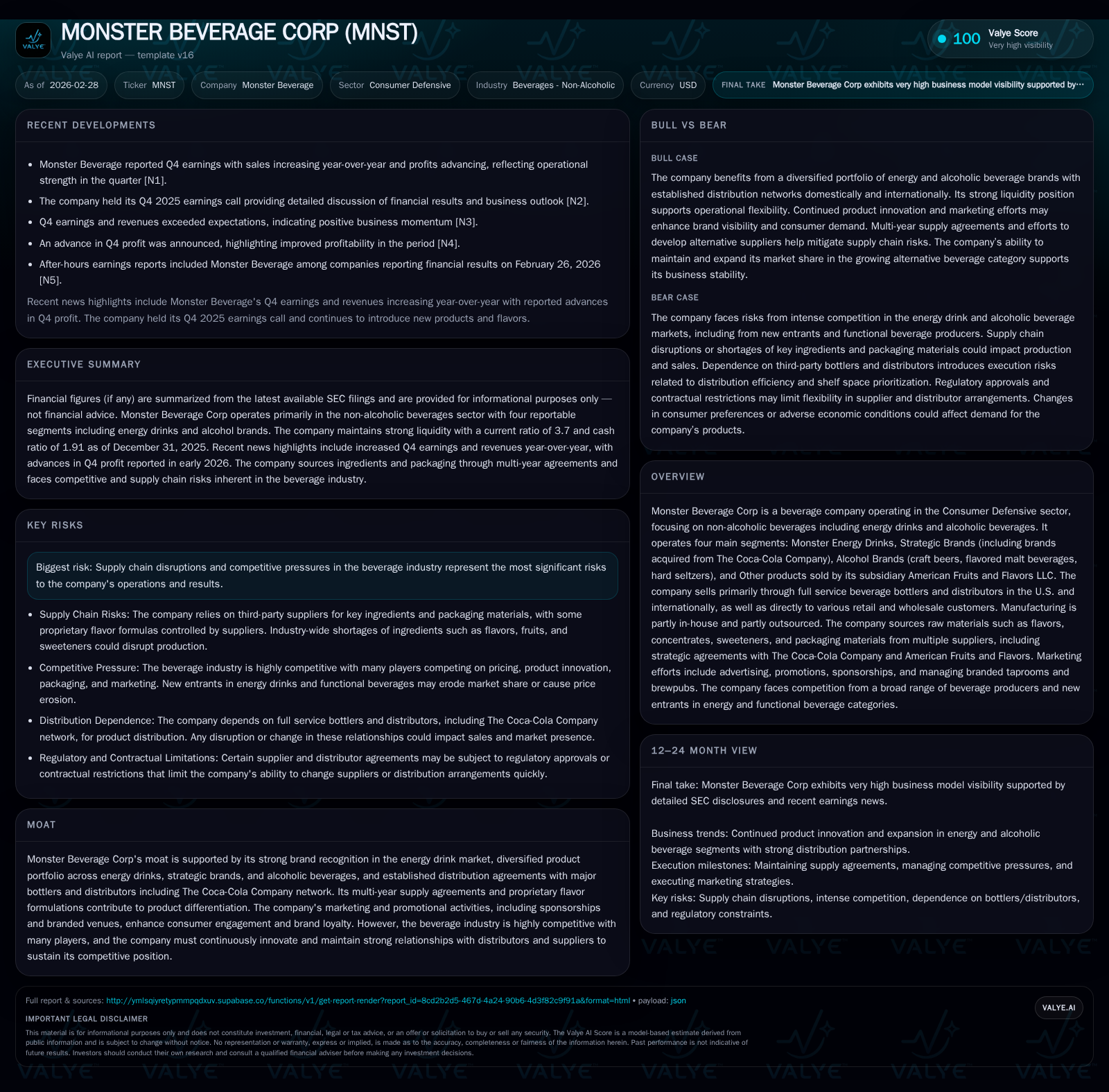

Monster Beverage’s Earnings Surge Reflects Strategic Brand Expansion and Distribution Strength

Robust operating income growth driven by diversified product lines and fortified distribution partnerships.

Monster Beverage Corp experienced a notable increase in operating income and net income in 2025, underscoring the effectiveness of its strategic brand expansions and an entrenched distribution network, particularly leveraging its relationship with The Coca-Cola Company bottlers. The company’s diversified segments—energy drinks, strategic brands, and alcoholic beverages—have collectively fueled top-line momentum while capital allocation shifted to more balanced share repurchases following heavy activity in prior years. Looking ahead, managing co-packing capacity constraints and navigating competitive pressures will be critical milestones to watch.

Financial Performance Snapshot: Operating Income and Net Income Growth Trends

Monster Beverage Corp demonstrated compelling profitability trends over recent years, culminating with its fiscal year 2025 results showing significant gains. Operating income rose sharply by 25.3% year-over-year to $2.42 billion, up from $1.93 billion in 2024 [F1]. This acceleration was accompanied by net income increasing even more robustly by 26.3%, reaching $1.91 billion [F1]. These metrics reveal effective operational leverage as the company scaled revenues without proportional expense growth.

Cash flows from operations (CFO) expanded by a healthy 8.8% to $2.10 billion [F1], highlighting strong underlying cash generation despite the step-down in capital expenditures, which nearly halved to approximately $132 million in 2025 from $264 million in the prior year [F1]. Lower capex possibly reflects a period of consolidation or efficiency optimization after prior expansion efforts.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1905 | 2.1 | 2.4 | 132 | +26.3% |

| 2024 | 1509 | 1.9 | 1.9 | 264 | -7.5% |

| 2023 | 1631 | 1.7 | 2.0 | 221 | +36.9% |

| 2022 | 1192 | 0.9 | 1.6 | 189 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0.1 | 1966 | 23.1 |

| 2024 | 3.8 | 1664 | 25.3 |

| 2023 | 0.7 | 1496 | 19.8 |

| 2022 | 0.8 | 699 | 17.0 |

Source: SEC companyfacts cache [F1].

*Figures for FY2025 reflect latest reported annual results [F1].

Historical Drivers Behind Revenue and Profit Expansion

The company’s revenue growth arc has been shaped heavily by strategic brand extensions coupled with marketing investments that boost brand equity among consumers across both domestic and international markets [S4][S5]. In particular, Monster’s intensified sales and marketing programs comprise an approximate increase of 6.3% in spending during the year ended December 31, 2025 [S5], underpinning elevated brand visibility.

Revenues draw prominently from the Monster Energy drink portfolio along with newly acquired or developed product lines under Strategic Brands—originally sourced from The Coca-Cola Company’s assets—and an expanding alcoholic beverage range comprised of craft beers, flavored malt beverages (FMBs), and hard seltzers [S4][S6]. This multi-segment approach allows for cross-category synergies while diversifying risk inherent to single-category focus.

International sales proved a notable contributor with net sales outside the U.S expanding from $2.71 billion in 2023 up to $3.44 billion by the end of fiscal year 2025 [S7]. Such geographic diversification efforts support resilience versus saturation risks within domestic channels.

Strategic Segments Reflection: Energy Drinks and Alcoholic Brands Momentum

Monster Beverage operates four main reportable segments: (i) Monster Energy Drinks; (ii) Strategic Brands; (iii) Alcohol Brands; and (iv) Others (primarily American Fruits and Flavors LLC products) [S6][S14].

The Monster Energy segment remains the flagship division with high per-case revenues though moderate gross margin percentages relative to Strategic Brands energy concentrates which carry comparatively higher margin profiles due to their concentrate sales model [S10]. Strategic Brands include affordable energy beverages like Predator® and Fury®, offering tiered pricing strategies that extend reach into value-sensitive demographics.

Alcohol Brands constitute an increasingly significant portion of the portfolio with sales comprising various ready-to-drink canned beers and FMBs distributed mainly through licensed beer distributors domestically [S10][S13]. While this segment commands lower gross profit margins than core energy drinks, it complements Monster’s market positioning by catering to evolving consumer tastes favoring craft brews and beyond-beer alternatives such as hard seltzers.

Manufacturing challenges are present regarding co-packer availability; constrained capacity among co-packers capable of handling various packaging innovations necessitates continuous scouting for additional contract manufacturing partners domestically and internationally [S7][S13].

Distribution Network Synergies and Market Penetration Insights

Distribution strategy rests heavily on entrenched relationships with full-service beverage bottlers/distributors primarily aligned through The Coca-Cola Company’s expansive bottling network encompassing North America and global markets [S4][S19][S27]. This infrastructure enables efficient market access while affording leverage over shelf space prioritization against competitors.

In the US alone, roughly forty-five percent of net sales traverse full-service bottler/distributor channels while international counterparts contribute another forty-three percent—a near balance reflecting deliberate global expansion efforts [S4]. Additional channels include club stores, e-commerce platforms accounting for about eight percent combined along with smaller portions via retail grocery chains.[S4] These partner ecosystems empower Monster to maintain distinctive brand positioning amidst variety-rich beverage shelves.

Customer concentration details highlight Coca-Cola Europacific Partners representing approximately fifteen percent of net sales in fiscal year ending December 31, 2025—up sequentially from thirteen percent two years prior—and Coca-Cola Consolidated consistently accounting for about ten percent annually [S23]. Continuity of such contracts remains paramount but comes with contractual termination rights offering negotiated exit or renewal triggers [S27].

Capital Allocation Priorities: Share Repurchases, Dividends, and Cash Flow Management

Monster exhibits disciplined capital stewardship marked by high return on equity approximating twenty-three percent based on latest figures ($1.91B net income / $8.25B equity) [F1]. Free cash flow generation is solid at roughly $1.97 billion after deducting capex from operating cash flow in FY2025 [F1], affording flexibility between reinvestment opportunities and direct shareholder returns.

Notably, share repurchase activity markedly declined—from an aggressive $3.77 billion spent in buybacks throughout FY2024 down to a more restrained $104 million in FY2025—a strategic pivot possibly aimed at preserving liquidity for organic growth or new initiatives rather than leveraging balance sheet aggressively [F1][S17]. There is no reported common dividend payout as of the latest filings; capital returns predominantly take place through buybacks.

This change signals management’s responsiveness to broader economic or competitive signals while maintaining prudent financial ratios including a conservative current ratio near three point seven times [F1].

Risks and Constraints on Growth: Supply Chain and Competition Dynamics

Supply chain complexity is a persistent risk factor influenced by dependencies on raw materials including aluminum cans (standard/slim/sealable variants), flavor concentrates sourced partially through American Fruits and Flavors LLC as well as supply agreements with The Coca-Cola Company for key ingredients among Strategic Brands drinks [S7][S21]. Global shortages or price volatility related to agricultural commodities such as hops or sweeteners add layers of uncertainty.

Co-packing facility limitations impose tactical production constraints given few high-capacity domestic/international partners equipped meeting specialized packaging needs; prolonged disruption could materially affect product availability at points-of-sale [S7]. Efforts continue to find alternative suppliers but contractual restrictions can impose hurdles especially concerning proprietary flavors owned by third-party providers [S21].

Competition intensifies across multiple vectors: from established multinational beverage corporations deepening functional beverage portfolios to nimble entrants releasing niche energy shot alternatives or 'beyond beer' style drinks like ready-to-drink cocktails [S11][N13]. Shelf space battles necessitate ongoing innovation around flavors, packaging differentiation combined with promotional heft supported by branded events.

Regulatory scrutiny also weighs on formulation marketing practices particularly surrounding health claims on energy or alcohol-based products demanding compliance monitoring across jurisdictions [S8].

Analyst Expectations and Key Milestones to Monitor

Although explicit guidance is limited in filings ([N9]), consensus anticipates sustained earnings improvements predicated on incremental volume gains both domestically via deeper penetration of existing SKUs plus alcoholic lineouts expansion internationally ([N1],[N3],[N11]). Monitoring quarterly earnings releases will be instructive given recent beats suggest ongoing upside potential ([N10],[N14]).

Milestones include:

- Increased rollout pace of alcoholic products including hard seltzers leveraging Monster Brewing Company distribution agreements.

- Extension or renewal confirmations of key Coca-Cola bottler distribution coordination agreements set for periodic review ([S19],[S27]).

- Progress on securing new co-packing arrangements lessening capacity bottlenecks especially amid new packaging innovations ([S7]).

- Marketing campaign effectiveness vis-à-vis incremental brand awareness metrics tracking against spending uptrend seen last fiscal year ([S5]).

Vigilance is warranted on how supply chain normalizes post-pandemic constraints plus regulatory developments impacting labeling or ingredient revelation will influence competitive positioning moving ahead.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data cited herein; it does not constitute investment advice nor a recommendation regarding any securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments