Mobia Medical’s Post-IPO Transition: Governance Restructuring and Operational Milestones

Mobia Medical reports its first quarterly results as a public company, revealing foundational governance reforms and financial scale amid ongoing operating losses.

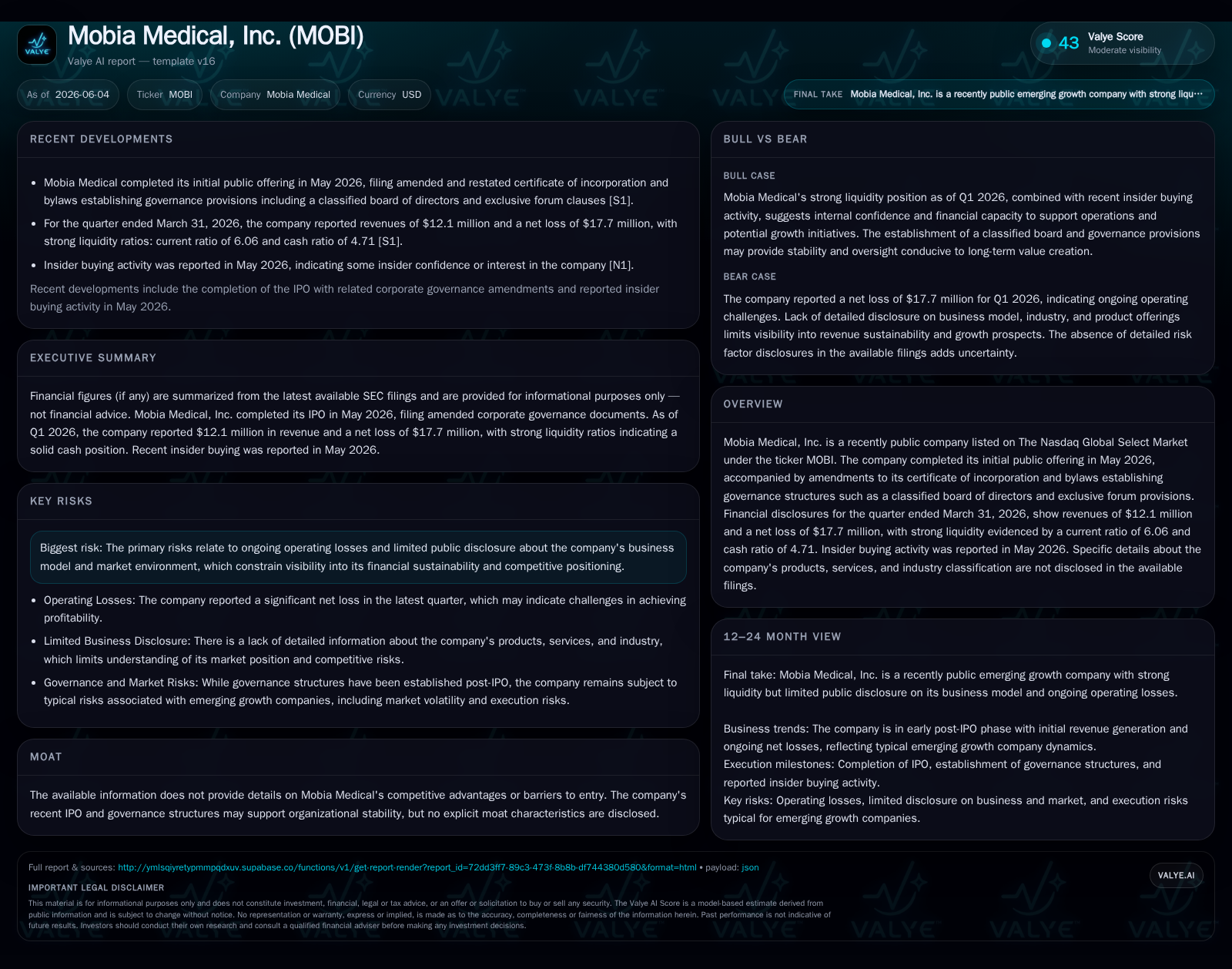

Mobia Medical, having recently completed its IPO in May 2026, filed its inaugural quarterly 10-Q indicating $12.1 million in revenue alongside a net loss of $17.7 million for the quarter ended March 31, 2026. The company’s balance sheet shows strong liquidity ratios that provide operational runway as it navigates early commercial scaling. Concurrently, Mobia formalized comprehensive governance restructuring via amended certificate of incorporation and bylaws featuring a classified board and exclusive forum provisions designed to reinforce organizational stability. Despite scarce specifics on products or market segments, these developments mark critical steps toward building the operational and structural backbone needed to translate early-stage investment into sustainable growth.

First Quarter Operating Update: Scale and Liquidity at IPO Dawn

Mobia Medical’s maiden quarterly disclosure as a Nasdaq-listed entity presents an early snapshot of its financial contours entering the public eyes. For the quarter ended March 31, 2026, revenue was reported at $12.1 million juxtaposed by a net operating loss of $17.7 million [S2]. This deficit reflects typical early commercialization challenges where foundational market development outpaces topline conversion. The balance sheet communicates significant liquidity strength — a current ratio surpassing 6.0 signals ample short-term assets to cover liabilities comfortably, while a cash ratio near 4.7 underscores cash dominance within those assets [S2]. Such liquidity ratios, particularly notable for an emerging healthcare business post-IPO, provide critical runway to pursue expansion without immediate capital pressure.

Notably, insider buying surfaced shortly after the IPO closed in May 2026 [N1], which can be interpreted as senior management's signaling of confidence in operational prospects amidst the nascent public phase.

Governance Reinvention Post-IPO: Classified Board and Exclusive Forum Provisions

Concurrent with its IPO completion on May 11, 2026, Mobia Medical undertook sweeping amendments to corporate governance outlined in an amended and restated certificate of incorporation alongside restated bylaws [S3],[S6],[S7]. Key among these reforms is the establishment of a classified board structure divided into three classes serving staggered three-year terms. This configuration limits immediate board turnover risk and establishes continuity in strategic oversight — a common feature among newly public biopharma firms aiming to insulate against activist pressures or destabilizing shareholder campaigns early on.

Additional provisions restrict director removals exclusively "for cause" requiring supermajority vote thresholds (two-thirds affirmative) from voting stockholders for such actions [S3]. This enhances managerial entrenchment possibilities but may stabilize long-term strategic initiatives during critical growth phases.

The bylaws also introduce exclusive forum clauses mandating Delaware courts as sole venues for derivative suits or fiduciary breach claims except for certain federal securities claims under SEC jurisdiction [S3]. In practice, this limits exposure to costly multi-jurisdiction litigation typical in high-profile healthcare IPOs and aligns with best practices observed in peer groups seeking reduced legal friction.

Overall, these governance enhancements signal proactive risk mitigation befitting companies positioned at sensitive inflection points between private development phases and public scrutiny.

Decoding Mobia’s Business Model Amid Limited Disclosures

While explicit details about Mobia Medical's product lines or target markets remain undisclosed in available filings, grounding analysis within healthcare sector norms helps approximate their operational model’s building blocks. Typically, companies in this sector generate revenue primarily from sales of medical devices or diagnostic tools to hospitals, clinics, or healthcare systems who ultimately pay either through direct purchases or via third-party payers including insurance providers.

Given reported revenues juxtaposed with operating losses indicative of ongoing market development rather than mature sales profitability, it is reasonable to infer Mobia operates on a commercial-stage yet nascent scale with likely concentration in select innovative medical technologies requiring clinical validation and payer acceptance.

Pricing power at this stage is generally fragile due to competitive pressures and reimbursement uncertainty; volume growth hinges heavily on successful regulatory clearances plus proven clinical utility enabling adoption by provider networks. Switching costs are moderate depending on product complexity but often accentuated through integrated hospital workflows or proprietary technology platforms once installed.

Without concrete product-level disclosures, these sector-native factors frame an ecosystem where success hinges on achieving sustainable utilization rates while managing cash burn before margin improvement — a scenario consistent with Mobia’s significant net losses amid positive revenue generation.

Industry Context: Typical Challenges for Newly Public Healthcare Firms

Companies transitioning from private to public ownership in biotech or medical device arenas frequently confront rigorous demands balancing innovation scaling with financial discipline. Pressure to validate scientific hypotheses morphs into requirements for commercial execution — building sales channels, obtaining regulatory approvals (e.g., FDA clearances), and securing reimbursement contracts all consume capital intensely.

Liquidity preservation becomes paramount alongside investor expectations gradually shifting from growth-at-all-costs narratives toward tangible profitability paths. Governance structures like those adopted by Mobia emerge as standardized defenses providing continuity amidst typical post-IPO volatility including activist investor interest or board composition debates.

These firms often face volatile headline risks stemming from trial outcomes or regulatory delays combined with elongated sales cycles common in hospital procurement settings when deploying disruptive technologies. Without entrenched moats documented here, competitive positioning might be fluid until products achieve differentiation confirmed through clinical outcomes and payer endorsements.

Growth Drivers: What Can Expand Demand and Improve Margins?

Despite limited explicit disclosures on pipeline status or market penetration metrics, plausible vectors exist for Mobia’s progression beyond current scale. Expanding commercial footprint remains fundamental — gaining wider provider acceptance accompanied by scaling recurring usage drives volume improvements that could dilute fixed costs.

Successful navigation of regulatory processes unlocks broader addressable markets especially if devices or diagnostics demonstrate compelling value propositions relative to standard care options. Coupled with favorable reimbursement environments motivated by cost-effectiveness or improved patient outcomes, pricing power may strengthen enhancing gross margins over time.

Additionally, insider purchasing activity may mirror internal assessments anticipating achievement of specific milestones such as clinical study readouts or contract wins pivotal to top-line expansions [N1]. Operational leverage through optimizing manufacturing or distribution capabilities represents another margin improvement lever common among peers progressing past initial commercialization dips.

Risks and Watchpoints: Operating Losses and Visibility Constraints

Operating losses totaling $17.7 million underscore ongoing investment intensity required at this stage though represent anticipated growing pains rather than aberrations peculiar to Mobia alone [S2],[S5]. The absence of detailed product/service disclosure curtails transparency into competitive dynamics or innovation differentiation creating heightened uncertainty around sustainable market positioning.

Risk factors emphasize potential challenges including failure to advance regulatory approvals timely or inability to secure reimbursers’ coverage which would inhibit sales ramp-up materially [S5]. Litigation risks are somewhat mitigated through governance proscriptions but remain endemic given sector complexity.

Investor caution remains warranted due to visible cash consumption combined with need for execution excellence amidst competitive healthcare technology markets where advantage rests on multiple fronts including intellectual property protection, clinical validation depth, channel access breadth, and pricing frameworks.

Upcoming Catalysts: Key Milestones to Monitor Next

In subsequent quarters, key indicators will include incremental revenue scaling aligned with operational cost controls potentially shrinking net losses as commercial activities mature [S2]. Regulatory newsflow—such as clearances for new indications or expanded use cases—will serve as tangible confirmation points boosting confidence in growth trajectories.

Financial disclosures regarding capital resources sufficiency amid burn rate evolution will further clarify liquidity runway duration supporting strategic initiatives without dilution pressures [N1]. Insider transactions following initial purchases could reveal evolving managerial sentiment regarding upcoming catalysts or challenges

Market reactions to any announced partnerships or contractual engagements would additionally signal validation within increasingly competitive environments where third-party endorsements matter critically.

Monitoring forthcoming SEC filings will be essential to map progression against established early-phase execution benchmarks typical within newly public healthcare enterprises transitioning toward scalable commercial operations.

This analysis synthesizes available disclosures from Mobia Medical’s initial quarterly filing post-IPO along with contemporaneous governance amendments contextualized within general healthcare industry knowledge. Due to limited explicit product details provided publicly at this time, interpretations remain cautious emphasizing structural developments and financial footing while identifying plausible strategic themes reflective of sector norms without speculative assertions. Readers should regard presented insights as informational framework absent any investment guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments