Motorcar Parts of America Advances Aftermarket Leadership with Scale and Innovation

Recent operational investments and exclusive customer agreements underpin Motorcar Parts’ sustained market leadership in the automotive aftermarket.

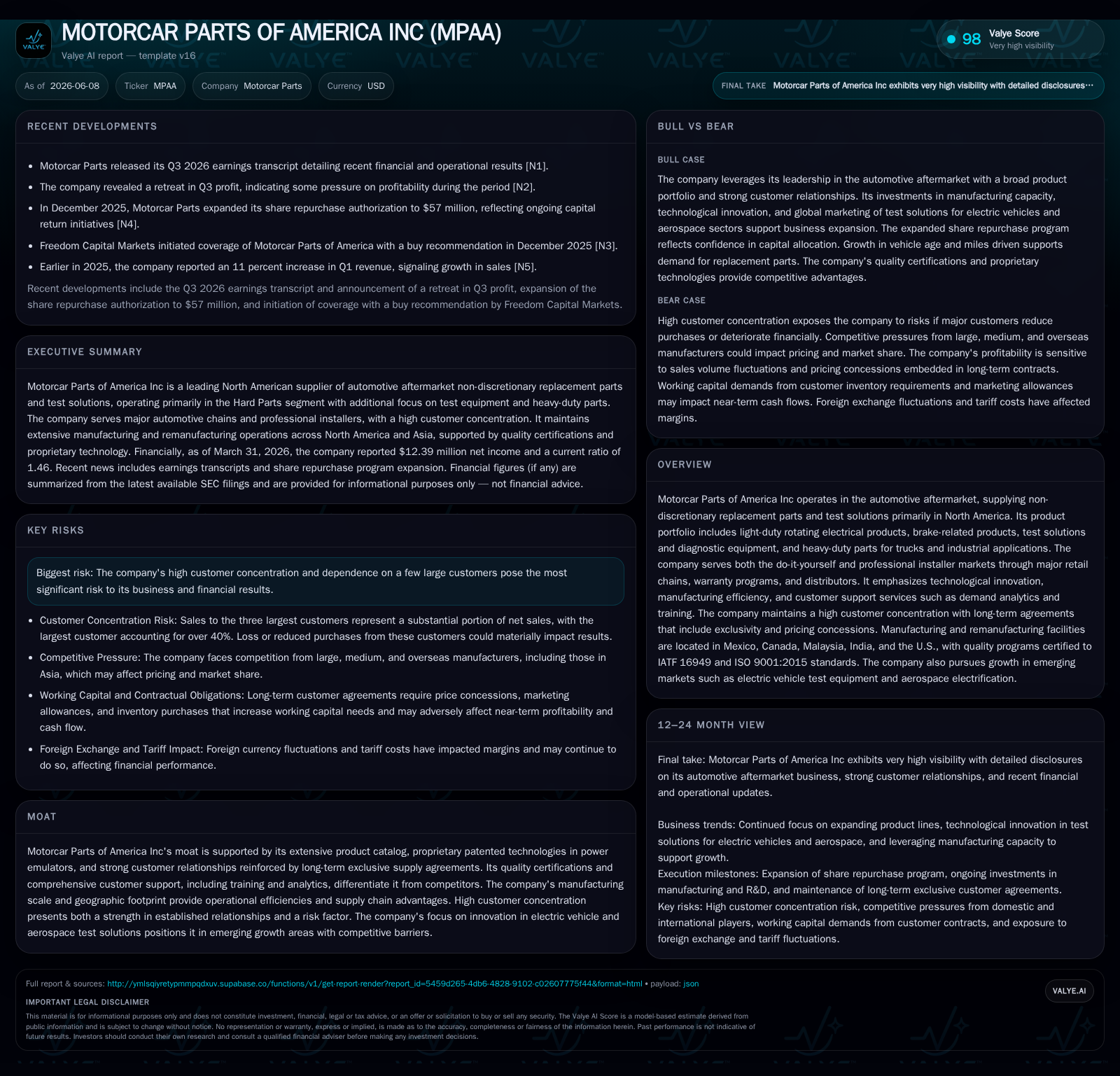

Motorcar Parts of America’s latest quarterly report highlights strategic expansions in manufacturing capacity and enhancements in inventory management, supporting its dominant position in the North American aftermarket. The company’s business model centers on sales of non-discretionary replacement hard parts and emerging test solutions for electrification, serving a highly concentrated customer base under long-term exclusive agreements. Operational efficiencies arising from a diversified manufacturing footprint and continued product innovation, particularly in diagnostic equipment, bolster growth prospects despite risks tied to customer concentration and working capital demands. Financially, Motorcar Parts maintains positive operating income and a solid liquidity position, illustrating effective balance-sheet management alongside growth initiatives.

Latest Quarterly Operating Update Sets Tone for Growth Continuity

Motorcar Parts of America’s 10-Q filing dated February 9, 2026 reveals meaningful progress in scaling its manufacturing infrastructure to meet growing aftermarket demand. The company invested in a new 410,000 square foot distribution center alongside 372,000 square feet dedicated to remanufacturing brake calipers—critical components in their hard parts lineup [S2]. Additionally, realigning production at its established Mexican facility of 312,000 square feet underscores efforts to optimize capacity utilization while controlling costs [S2].

Finished goods turnover ratio decreased modestly to an annualized rate of 3.4x from prior periods, suggesting increased inventories driven by contractual requirements to maintain stock levels for key customers under exclusive agreements [S2]. This inventory buildup supports service-level targets critical in the automotive aftermarket, where fill rates and on-time delivery are key KPIs influencing customer retention and shelf presence.

Business Model Anchored by Non-Discretionary Hard Parts and Test Solutions Innovation

Motorcar Parts generates the bulk of its revenue from non-discretionary replacement parts within the North American automotive aftermarket—a $130 billion sector focused primarily on vehicle maintenance rather than discretionary upgrades [S1][S19]. Its customer base consists mainly of large retail chains such as Advance Auto Parts, AutoZone, Genuine Parts Company (NAPA), and O’Reilly Auto Parts, servicing both do-it-yourself (DIY) purchasers and professional installers (do-it-for-me, DIFM) [S8].

Key product categories include light-duty rotating electrical components (alternators, starters), comprehensive brake assemblies (calipers, boosters, pads), wheel hubs, turbochargers, as well as heavy-duty replacement parts for trucks and industrial applications acquired via strategic bolt-ons like Dixie Electric [S1][S8][S11].

The company’s test solutions segment is rapidly expanding with offerings tailored for electric vehicle (EV) development—including hardware-software power emulation platforms—and diagnostic equipment servicing pre- and post-production validation across automotive and aerospace applications [S1][S22]. This segment benefits from intellectual property protections such as U.S. patents on proprietary power emulators, which create a significant technological moat and support higher margin potential [S1][S8].

Motorcar Parts operates under long-term supply contracts averaging at least four years, providing exclusivity or primary supplier status. These agreements come with pricing concessions, marketing allowances, and service-level commitments [S4][S11]. A notable working capital consideration is the requirement to purchase and maintain remanufactured core inventories held on customer shelves, a capital-intensive practice integral to sustaining these partnerships and ensuring product availability [S4].

Industry Context: Competitive Positioning Amid Concentrated Customer Base

Sales concentration is pronounced; approximately 85% of net sales in fiscal year 2026 stem from the top three customers, with a single largest client accounting for over 40% of revenues [S4][S19]. While this confers deep relationship strength and negotiation leverage via exclusivity contracts, it simultaneously concentrates revenue risk should any key customer reduce volumes or shift purchasing strategies.

Competitive dynamics pit Motorcar Parts against companies such as Terrepower and DRiV in hard parts, as well as Burke Porter and Langdi Measurement Control in test equipment segments. However, Motorcar Parts differentiates itself through an extensive catalog breadth of approximately 44,000 SKUs, superior delivery logistics bolstered by large-scale distribution centers strategically located near major demand zones, and detailed technical resources including online training modules for technicians [S4][S10][S15].

Unlike broader OEM-focused peers such as Magna International or BorgWarner, Motorcar Parts specializes in aftermarket core exchange programs combined with proprietary electrification test solutions tailored specifically for aftermarket needs, reinforcing its competitive moat and customer stickiness.

Manufacturing Footprint Driving Operational Flexibility and Cost Management

Motorcar Parts maintains a globally dispersed manufacturing and remanufacturing footprint anchored principally in Mexico (its largest production base), Canada, Malaysia, and India, complemented by U.S.-based assembly lines for diagnostic equipment [S1][S26]. This geographic diversification enables the company to leverage tariff advantages and optimize supply chain costs while maintaining proximity to critical North American markets.

The company employs lean manufacturing principles, batching similarly configured product families into dedicated work cells to reduce inventory handling complexity and improve throughput. Environmentally conscious remanufacturing practices recycle metals and packaging materials, supporting sustainability initiatives increasingly valued by customers [S15][S17].

Strategic sourcing favors low-tariff countries while ensuring supplier compliance with quality standards such as ISO/TS16949 certifications, balancing cost competitiveness with stringent quality requirements—an essential factor given the critical safety nature of automotive replacement parts.

Growth Drivers: Electrification Trends and Expanding Test Solutions Portfolio

The aging vehicle fleet in North America, with an average age around 13 years, drives structurally recurring demand for replacement parts as wear-and-tear necessitates maintenance and repair, providing a stable revenue base [S1][S22]. Additionally, historically rising miles driven offset fuel price fluctuations, supporting steady aftermarket volume growth even during economic downturns.

Complementing legacy product lines, Motorcar Parts is expanding its footprint in the $11 billion-plus global market for automotive test solutions focused on electrification technologies. This includes electric motors for vehicles and aerospace sectors transitioning toward electric propulsion systems [S1][N1]. Its diagnostic offerings cover combustion engines and inverter systems critical for EV charging infrastructure validation, enhancing future growth optionality beyond traditional hard parts [S22].

Risks Highlight: Customer Concentration and Working Capital Demands

Exclusive customer relationships secure shelf space but enforce pricing concessions that compress margin headroom while mandating significant upfront investment in remanufactured cores stocked at Motorcar’s facilities, imposing working capital strain [S4][S18]. Should large customers scale back orders or experience financial distress, revenue stability could be materially affected.

Cybersecurity risks also warrant careful oversight given increased hacking threats across supply chains. The company’s defenses include a multifaceted cybersecurity program with employee training, external audits, data protection frameworks aligned with NIST standards, and Audit Committee supervision [S18][S20].

What to Watch: Upcoming Milestones in Product Expansion and Customer Renewals

Key forthcoming catalysts include renewal negotiations with top-tier customers who account for the majority of sales; the terms agreed will strongly influence near- to medium-term revenue trajectories and associated marketing support commitments [N1][S3]

Monitoring advancements within the test solutions division offers insight into the company’s pace of winning new contracts, particularly within electric vehicle OEM ecosystems and adjacent aerospace segments.

Operational metrics such as finished goods turnover improvements or capacity utilization optimizations at Mexican manufacturing sites will also serve as leading indicators of margin expansion potential.

Financial Snapshot: Profitability, Liquidity, and Capital Structure Review

For the fiscal year ending March 31, 2026, Motorcar Parts reported operating income of $65.8 million backed by net income of $12.4 million, demonstrating continued profitability amid competitive pressures [F1]. Cash and equivalents stood at $14.7 million, supported by a strong current ratio of approximately 1.46, reflecting solid short-term liquidity management despite sizeable working capital needs [F1][S2].

Total debt approximated $28.8 million (best-effort figure) yielding net debt near $14.1 million after cash offsets [F1][S23]. No material changes in leverage were noted compared to previous disclosures, preserving financial flexibility under existing credit facility arrangements maturing in late 2028

The company remains focused on balancing incremental capital investments aimed at manufacturing expansion while maintaining discipline over operating cash flows necessary for sustainable growth execution.

This analysis synthesizes disclosures from Motorcar Parts’ latest SEC filings alongside recent earnings commentary without expressing any investment research view or forecast. It contextualizes operational developments within industry fundamentals relevant to stakeholders monitoring aftermarket substitution dynamics amid accelerating electrification trends.

Financial position in context

As of 2026-03-31, companyfacts shows $14.65 million in cash and equivalents [F1]. Current assets of $583.98 million and current liabilities of $399.60 million imply a current ratio near 1.46x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments