Micron Technology’s Surge: Capitalizing on AI-Driven Memory Demand and Manufacturing Expansion

Micron’s Q3 fiscal 2026 results reveal a sharp rebound fueled by robust AI-related memory demand and strategic capacity investments.

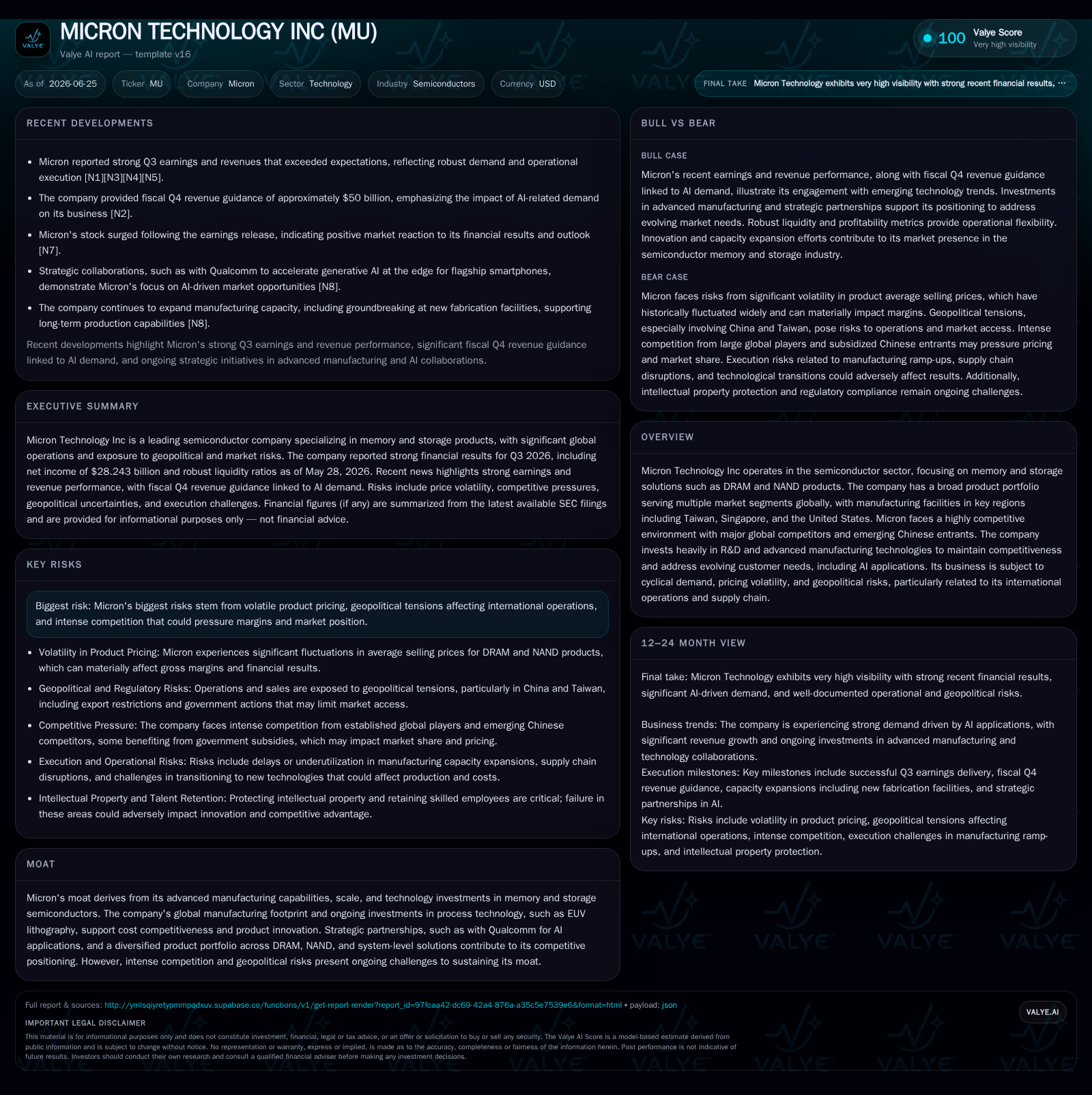

Micron Technology reported a strong Q3 fiscal 2026, with significant increases in bit shipments and fab utilization driven by surging AI and data center memory demand. The company’s guidance for a record-breaking $50 billion in Q4 revenue underscores accelerating momentum. Micron continues to leverage advanced manufacturing technologies like EUV lithography and capital expenditure expansion to maintain competitiveness amid industry cyclicality and geopolitical risks. Key challenges remain in pricing volatility and competition from emerging Chinese manufacturers, but Micron’s operational focus and R&D investments position it well for growth in the evolving semiconductor memory market.

Recent Quarterly Operating Update: Highlights from Q3 Fiscal 2026

Micron’s latest 10-Q filing for the quarter ended May 28, 2026, provides clear evidence of a strong operational rebound [S2]. Central to this uplift is accelerating demand for memory chips driven by the AI wave in data centers. The company reported meaningful increases in bit shipments across both DRAM and NAND product lines. Fab utilization rates improved significantly as manufacturing facilities operated closer to peak capacity levels to meet surging customer orders. This operational leverage contributed to an improved gross margin profile despite ongoing price pressure environment typical in memory markets.

Notably, Micron raised its fiscal Q4 revenue guidance to a staggering $50 billion - setting a new record for the company's quarterly sales volume [N1]. This aggressive forecast reflects confidence in sustained high demand from hyperscale cloud operators and next-generation computing platforms relying heavily on DRAM density improvements. Average selling prices (ASPs) per bit have stabilized after recent volatility, aiding margin recovery. Inventory days trended downward versus prior quarters, indicating healthy demand absorption rather than channel stuffing.

The Q3 performance contrasts with prior periods marked by softer end-market consumption and elevated inventories industry-wide. This inflection reflects structural changes where AI workloads materially boost memory bandwidth needs, altering the underlying cyclical dynamics typical for Micron's sector [N2]. Capitalizing on this backdrop has allowed Micron to recapture share momentum while optimizing fab output efficiency.

Micron’s Business Model: Memory Chip Production and Market Dynamics

Micron’s core business revolves around designing, fabricating, and selling semiconductor memory products — principally DRAM and NAND Flash — serving diversified customers such as OEMs (original equipment manufacturers), cloud service providers, consumer electronics firms, and automotive segments [S1]. Revenue mechanics depend on bit shipments volume multiplied by average selling prices (ASPs), which are influenced by product mix (DRAM typically commands higher ASPs compared to NAND) along with contract terms.

Production entails wafer-level semiconductor fabrication leveraging cutting-edge process technology nodes integrated with EUV lithography. Yield rates per wafer — the percentage of functional chips produced — directly influence unit economics. Constant R&D investments ensure leadership through smaller gate geometries, increased memory density via multilayer NAND stacking or pitch scaling in DRAM.

Recent filings indicate sustained elevated R&D spends as percentage of revenue supporting innovations tailored toward AI-centric workloads requiring ultra-high throughput memory products [S2]. Product mix currently favors DRAM owing to robust uptake for server-grade applications tied to artificial intelligence algorithms demanding large-scale volatile storage with low latency. Meanwhile, NAND continues growing within consumer electronics but competes aggressively on price.

Micron operates globally distributed fabs across Taiwan, Singapore, and the United States to balance geopolitical risk exposures while optimizing logistics. The company manages complex supply chains sourcing advanced materials and capital equipment essential for scale manufacturing at state-of-the-art fabs [S1]. Capital expenditure programs targeted at wafer fab expansions align production capacity closely with forecasted bit demand trajectories tied especially to AI-driven compute infrastructure.

Semiconductor Industry Structure: Competitive Landscape and Technology Trends

The global semiconductor memory market is dominated by major integrated device manufacturers (IDMs) such as Samsung Electronics and SK Hynix alongside Micron — all competing intensely on technology differentiation, scale economies, and cost leadership. Emerging Chinese memory manufacturers introduce new competitive pressures impacting pricing dynamics given their rapid capacity ramp-up albeit generally lagging in process node maturity.

Micron’s moat manifests through advanced manufacturing capabilities enabled by early adoption of next-gen process technologies including EUV lithography enabling finer line widths thus reducing cost per bit and improving yield simultaneously [S1]. Strategic partnerships expand AI market penetration though no single customer contract specifics are disclosed publicly.

Vertical integration also gives these IDMs an advantage versus pure-play foundries or external suppliers by controlling design-to-manufacturing pipelines responsible for complex multi-billion dollar fab investments. However, geopolitical tensions especially involving Taiwan-China relations pose risk vectors affecting supply chain resilience requiring contingencies across multiple sites in Singapore and the U.S. [S7].

Key Growth Drivers: AI Adoption, Data Center Expansion, and Manufacturing Scale-up

The primary structural driver behind Micron's recent surge is exponential growth in data volumes processed by AI models alongside cloud computing infrastructure expansion [N1],[S2]. This trend accelerates bit consumption well beyond traditional personal computing or mobile device usage patterns which historically dictated memory demand cycles.

Increased fab utilization reflects efforts to maximize output against constrained supply conditions coupled with capital expenditure focused on capacity expansions at existing fabs as well as potential new-foundry node developments [S2],[S3]. These investments support higher bit shipment volumes linked tightly to measured backlogs signaling sustained customer orders.

Further enhancements in memory density enable devices with greater storage capacity per chip area benefiting form factor-sensitive applications such as smartphones but also server modules underpinning hyperscale deployments. These technological advances improve ASP realizations over older nodes raising overall segment profitability.

Government incentives targeted at semiconductor manufacturing domestically also underpin capex strategies facilitating long-term competitive positioning despite ongoing cyclical headwinds [S10]

Risks to Monitor: Pricing Volatility, Geopolitical Tensions, and Competitive Pressure

Micron acknowledges key risks inherent in its operating environment including pronounced average selling price volatility characteristic of semiconductor memory markets where supply-demand imbalances can lead to swings exceeding 30-50% between upcycle/downcycle phases [S22],[S7]. Periods of ASP compression below manufacturing cost levels could severely impact gross margins.

Geopolitical factors remain an ongoing concern particularly related to operating facilities across Taiwan amidst broader China-US tensions influencing trade policies or export controls potentially disrupting component supply chains or limiting market access [S23]. These conditions necessitate continued diversification but may increase operational complexity.

Competitive intensity from both legacy global firms expanding NAND/DRAM capacities aggressively as well as emerging Chinese manufacturers introducing pricing pressures challenge margin sustainability requiring consistent innovation investments along with disciplined capital allocation [S15]. Intellectual property protection represents another material risk given industry reliance on patented process technologies vulnerable to infringement claims or replication attempts especially under evolving international IP laws [S14],[S15].

Operational risks related to building out new fab capacity—including project delays or safety incidents—can affect output ramp timing impacting near-term revenue recognition [S17]. Additionally, disruptions from raw material shortages or power/water availability constraints add layers of complexity in high-capital fabrication settings [S7].

"What to Watch Next": Guidance, Milestones, and Market Signals Ahead

Looking forward into fiscal Q4 2026 and beyond, the primary indicators of Micron's trajectory involve its execution on capacity expansions aligned with elevated capital spending plans noted in recent filings alongside monitoring order backlog trends signaling sustainable strong demand [N1],[S2],[S3].

Inventory levels trending lower after correction imply healthy sell-through; any build-up could presage softness ahead. Pricing trends for DRAM versus NAND will bear watching given their differing margins/profitability impacts. Further disclosure on fab utilization rates will shed light on supply-demand equilibrium shifts.

Milestones related to process technology node transitions using EUV tools remain critical for cost reduction steps underpinning competitive advantages. Also important is progress mitigating geopolitical risks through facility diversification strategies ensuring stable delivery commitments globally.

Market analysts are attentive to quarterly earnings announcements providing updated guidance affirming or adjusting optimistic forecasts related primarily to AI-driven workload scaling demand strength seen thus far [N4],[N5].

Financial Profile Discussion: Liquidity and Capital Allocation Snapshot

As of May 28, 2026, Micron maintained a strong liquidity position supported by cash & equivalents totaling approximately $24.995 billion [F1]. Current assets of $66.7 billion and current liabilities of $19.5 billion imply a current ratio near 3.42x, evidencing solid short-term asset coverage over liabilities [F1]. Total debt is estimated at approximately $5.755 billion based on the most recent available figure [F1]. This positioning suggests financial flexibility.

Operating cash flow generation remains subject to cyclicality linked closely with significant fluctuations in average selling prices but overall free cash flows have improved commensurate with revenue gains reported recently sustaining investment appetite while managing leverage prudently.

This analysis synthesizes Micron's latest quarterly disclosures alongside sector context without making investment research views or forecasts beyond documented data points.[S2][N1][F1]

Financial position in context

As of 2026-05-28, companyfacts shows $25.0bn in cash and equivalents [F1]. Current assets of $66.7bn and current liabilities of $19.5bn imply a current ratio near 3.42x for 2026-05-28 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments