FDCTech Advances Offshore Regulated Brokerage Reach Amid Financial Restatements

FDCTech’s recent quarterly update confirms operational stability post acquisition-driven expansion and financial restatement remediation.

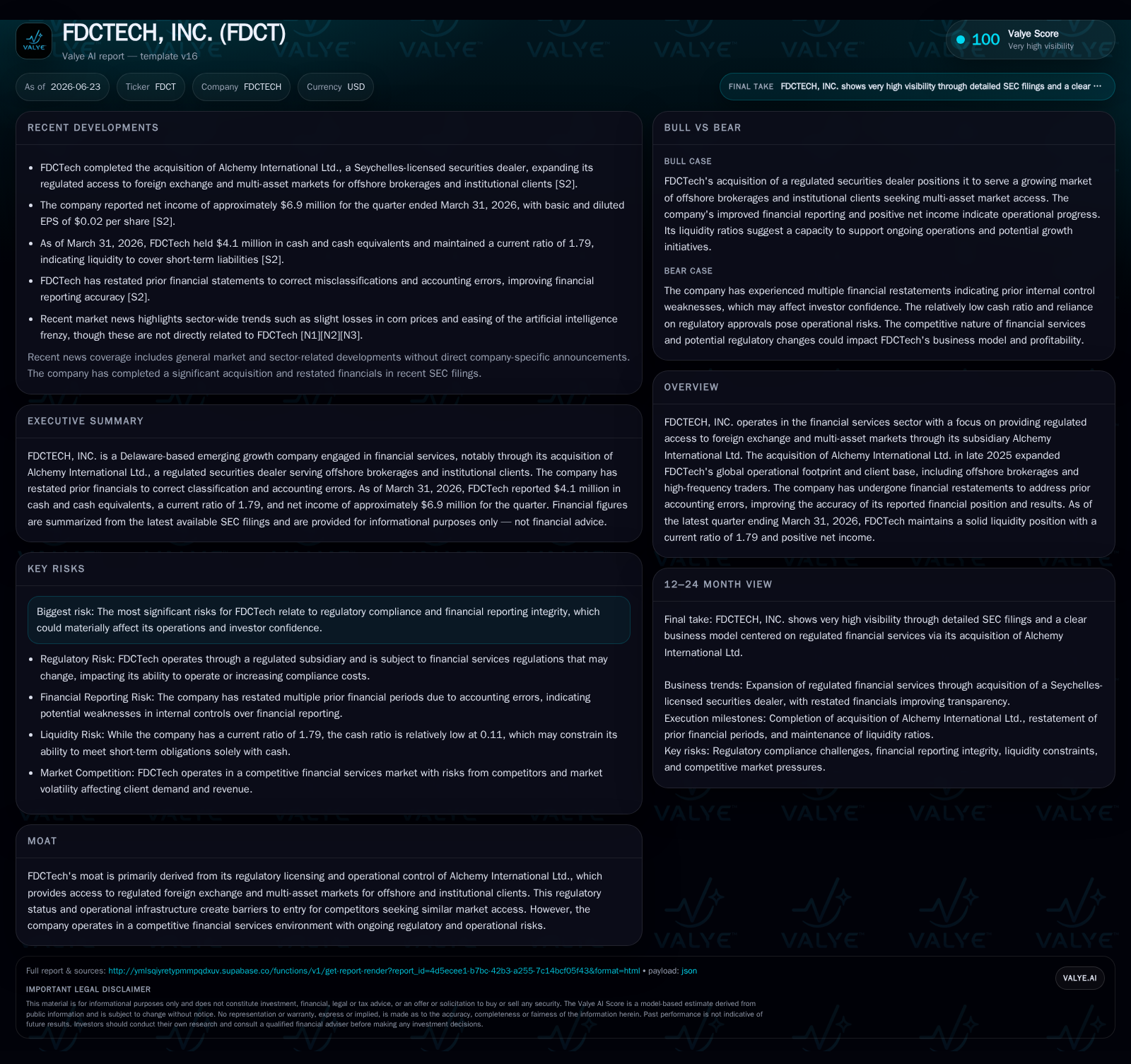

FDCTech, Inc. reinforced its position in the fintech-enabled regulated brokerage sector with its latest quarter ending March 31, 2026, marked by solid liquidity and positive net income. The company’s integration of Alchemy International Ltd. has broadened its offshore multi-asset trading footprint, serving institutional and retail clients across multiple jurisdictions. While the extended restatement process has improved financial reporting integrity, regulatory compliance and litigation risks remain watchpoints as the firm navigates competitive and jurisdictional complexities.

Recent Operating Update and Why It Matters

In its latest quarterly filing for the period ended March 31, 2026 [S2], FDCTech has demonstrated operational resilience following a significant expansion phase culminating in the acquisition of Alchemy International Ltd. in late 2025 [S13]. This Seychelles-regulated brokerage extends FDCTech's geographic reach into key Asian offshore markets with services aimed at sophisticated retail and institutional investors including high-frequency traders. The quarter reveals strong liquidity metrics, notably a current ratio of 1.79 supported by $41.2 million in cash and equivalents relative to current liabilities of roughly $38 million [F1]. Net income remains positive post-restatement processes that addressed material financial reporting deficiencies identified over the past two years [S22], which had involved client fund misclassifications, subscription receivables reclassifications, and foreign currency translation adjustments.

This update underscores a pivotal transition for FDCTech from a U.S.-based fintech provider towards a global regulated brokerage platform operator with diversified revenue streams anchored in trading commissions, spreads, and technology licensing [S1]. Importantly, this advancement occurred amidst ongoing remediation of internal controls and accounting practices overseen by its current independent auditor LAO following the replacement of Olayinka Oyebola & Co. due to regulatory prohibition [S22]. Although the net income figures have been broadly confirmed after adjustments ($6.87 million attributable to shareholders for Q1 2026), continuous vigilance on financial governance remains critical given prior material weaknesses.

Business Model: Revenue Mechanics and Strategic Position

FDCTech operates primarily through fully regulated margin brokerage subsidiaries: Alchemy Markets Ltd. (Malta), Alchemy Prime Ltd. (UK), Alchemy International Ltd. (Seychelles), complemented by wealth management services via AD Advisory Services Pty Ltd. (Australia) [S1]. Revenue stems predominantly from brokerage commissions and spreads derived from forex (FX), contracts for difference (CFDs), equities, commodities, and emerging digital assets trading activities conducted on its Condor Trading Technology platform.

The company strategically integrates proprietary technology—Condor Trading supports multi-asset order execution, sophisticated risk management tools, and dynamic pricing engines—which represents a core differentiator in delivering fast, reliable trading experiences vital for client retention especially among active traders [S1]. Clients pay transactional fees based on volume and leverage deployed; pricing power hinges on maintaining competitive spreads with efficient compliance to regulatory capital adequacy rules.

The business also benefits from fee-based revenue streams associated with wealth management advisory under ASIC licenses in Australia as well as payment intermediary services through Xoala Asia targeting Asian cross-border merchants [S1]. This diversified segment mix helps mitigate reliance on cyclical FX volatility but demands regulatory finesse across multiple jurisdictions.

Industry Structure and Competitive Landscape

FDCTech occupies a mid-to-late value-chain position typical of global fintech-enabled regulated brokerages that act as intermediaries between end-users—retail clients, institutional traders—and the complex web of multi-asset financial markets. Its main competitors span established forex/CFD brokers like Interactive Brokers or IG Group, plus fintech providers offering advanced trading platforms such as MetaQuotes or Saxo Bank.

The firm’s competitive moat is substantially fortified by stringent regulatory licensing across Malta’s MFSA, UK's FCA, Seychelles FSA, Australia’s ASIC, Cyprus CySEC, and Mauritius FSC—an asset creating significant operational barriers for prospective entrants seeking approved market access for their clients [S1]. These licenses underpin trust and transparency in an industry often scrutinized for AML compliance risks.

However, FDCTech's growth as a new entrant in payments intermediaries faces headwinds linked to competing against entrenched players like PayPal or Stripe whose scale offers pricing leverage enhanced security features—the company candidly acknowledges these challenges within its filings [S1]. Operationally, latency benchmarks on its Condor platform will be critical to sustain high-frequency trader adoption.

Growth Drivers

Several structural factors underpin FDCTech’s growth outlook:

- Global Expansion of Retail & Institutional Trading: Increasing participants are accessing multi-asset digital trading instruments requiring regulated offline brokerages capable of servicing cross-border flows.

- Acquisition Strategy: The integration of Alchemy International enlarges FDCTech’s footprint across key offshore jurisdictions with growing FX/CFD activity.

- Technology Innovation: Constant enhancements to the Condor system aim to improve pricing engine accuracy and order execution speed—a necessary condition for attracting volume-sensitive high-frequency traders.

- Regulatory Reforms: Licensing enabled by international cooperation facilitates FDCTech providing broader market access compliant with capital adequacy norms.

- Diversification into Payment Services: Xoala Asia targets merchant onboarding growth amid rising eCommerce transactions requiring reliable payment intermediaries [S1]

These drivers correspond directly to KPIs such as trading volume growth (notional value), active client counts expanding beyond traditional geographies into Asia-Pacific regions served by Seychelles entities, improving average revenue per user via tech upgrades enhancing spill-over revenues from wealth management advisory fees.

Risks and Constraints

Despite promising positioning, FDCTech faces several watchpoints:

- Regulatory Compliance Risks: Prior AML deficiencies discovered post-acquisitions have led to ongoing litigation with former shareholders alleging undisclosed liabilities from anti-money laundering breaches at Alchemy Markets Ltd.; court proceedings are scheduled November 2026 [S1]. Such compliance issues pose operational disruption risks alongside reputational consequences.

- Financial Reporting Integrity: The extensive restatement process unveiled material weaknesses necessitating remediation plans overseen by both management and auditors [S22]. Continuous transparency around these controls is essential to uphold investor confidence.

- Competitive Pressure: Price compression from larger incumbents with deeper pockets could limit margin expansion prospects particularly in payments segments where achieving scalable merchant acceptance remains elusive [S1].

- Technology Dependency: Persistent demands for low-latency execution expose vulnerabilities if infrastructure outages or cyber incidents occur.

- Geopolitical Factors: Cross-border trading volumes may be sensitive to macroeconomic tensions affecting client discretion or regulatory environments shifting unfavorably.

Management has acknowledged these factors candidly within SEC disclosures but maintaining stringent oversight will be a determinant factor for sustained growth.

What to Watch Next

Key milestones include:

- Trial outcomes scheduled November 2026 relating to acquisition-period AML lapses litigation impacting Alchemy Markets Ltd.’s shareholder disputes [S1].

- Continued rollout enhancements of Condor Trading Technology targeting integration efficiencies that improve latency metrics critical for high-frequency trader adoption rates.

- Quarterly filings updating remediation progress on internal control improvements reshaping financial governance frameworks started post-2025 announcements [S22].

- Client base growth signals from net new account openings among institutional offshore brokerages serviced through Seychelles jurisdictional licenses.

- Regulatory developments influencing licensed capacities in existing jurisdictions or entry into additional offshore markets expanding multi-asset offering spread.

Investor communications highlighting improvements in compliance frameworks or diversification into payment intermediary scale would be important guidance markers when available.

Financial Profile Summary

As of the quarter ending March 31, 2026, FDCTech maintained cash & equivalents totaling approximately $4.12 million against current liabilities near $38 million yielding a healthy current ratio of 1.79 [F1], indicating short-term liquidity sufficiency despite operating in a capital-intensive regulatory regime. Total debt appears modest by comparison at approximately $550 thousand as last known at end-2022 [F1], suggesting conservative leverage usage supportive of balance sheet flexibility. While reported revenue figures are limited outside historical context given restatements effects [F1], net income attributable to shareholders was positive at about $6.87 million for Q1 2026 per amended filings [S2]. This underscores improved profitability though operating margins must be analyzed carefully considering prior accounting irregularities now rectified.

DISCLAIMER: This analysis is based solely on publicly filed SEC documents dated through June 23, 2026 (), verified company facts ([F1]), and contextualized industry knowledge without proprietary insights or forward-looking projections. It does not constitute investment advice or research views but aims to provide an informed perspective rooted in documented operational data and sector trends.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments