C3AI Inc: Restructuring and Innovation Amid Enterprise AI Expansion

C3AI pursues operational efficiency through restructuring while deepening its AI platform’s technological lead in enterprise software.

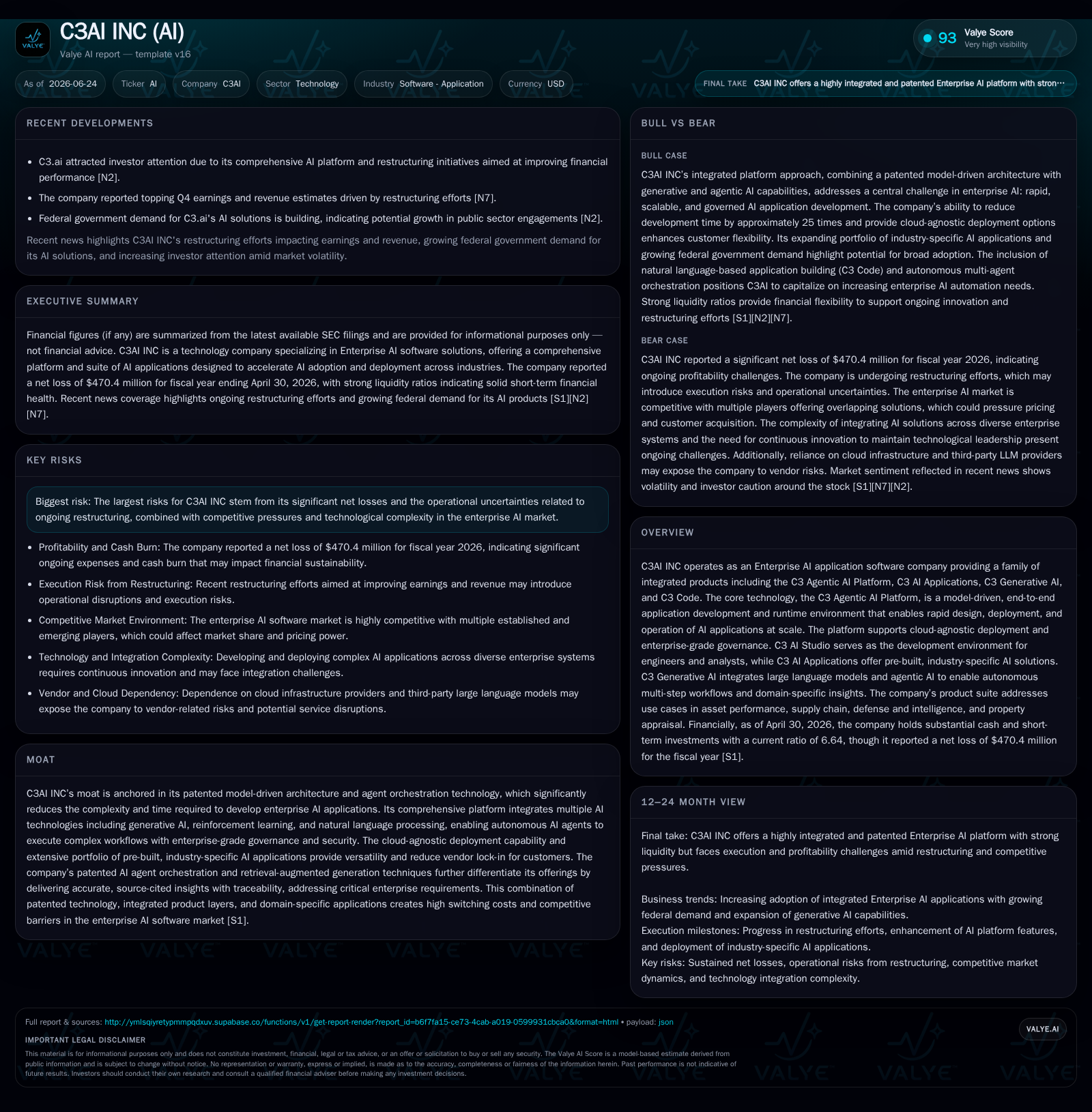

In its latest Q3 filing, C3AI reported significant restructuring efforts, including a 26% workforce reduction aimed at improving operating efficiency and positioning for profitability, while continuing to invest in its patented enterprise AI platform integrating generative and agentic AI technologies. The company leverages a subscription SaaS model anchored by industry-specific AI applications deployed on a cloud-agnostic platform, enabling rapid time-to-value and autonomous AI orchestration. Despite ongoing net losses driven by high R&D costs and structural challenges, C3AI’s moat rests on its patented model-driven architecture and strategic partnerships with leading cloud providers and consulting firms. Growth will hinge on expanding generative AI use cases, partner ecosystem scale, and execution improvements post-restructuring amid intense competition and regulatory complexities.

Q3 Operating Update Highlights: Restructuring Impact and Revenue Dynamics

While top-line growth faced headwinds from the organizational changes, the company continues to prioritize ramping subscription revenues—its principal source of recurring income—through its comprehensive AI software solutions [N1][S2]. The focus remains on converting pilot projects into sustainable production deployments that fuel longer-term renewal streams with large enterprise customers

C3AI’s Business Model: Subscription SaaS with Industry-Centric Applications

C3AI operates on a subscription-based SaaS revenue model complemented by professional services that facilitate initial production deployments (IPDs). The bulk of revenue stems from subscriptions granting customers access to the C3 Agentic AI Platform, pre-built industry-specific applications, generative AI capabilities, runtime hosting fees, and stand-ready Center of Excellence (COE) support services [S7][S11]. Customers are typically large enterprises across diversified verticals including manufacturing, energy, defense, healthcare, financial services, and government sectors.

Contracts often span multiple divisions or operating units under enterprise-wide agreements structured for multi-year durations. This arrangement supports steady annual recurring revenue (ARR) growth driven by new customer acquisition as well as account expansion through additional applications or increased platform usage [S15]. The modular portfolio enables customers to rapidly adopt tailored AI solutions aligned with their industry workflows reducing deployment friction—a strategic advantage connected to shorter time-to-value metrics critical for enterprise renewals

Technology Moat: Patented Model-Driven Architecture & Agentic AI Integration

At the core of C3AI's competitive edge lies its patented model-driven architecture which replaces traditionally complex coding with declarative programming that encapsulates conceptual models of enterprise data elements and processes. This innovation drastically reduces development time for sophisticated Enterprise AI applications by allowing developers to focus on value rather than plumbing intricate data pipelines or system integrations [S1][S14][S26].

Furthermore, C3AI's agentic orchestration technology powers autonomous AI agents capable of executing complex multi-step workflows involving data retrieval, cross-system reasoning, and action initiation within governed enterprise environments. The native embedding of generative AI fused with reinforcement learning enables high-fidelity domain-specific insights that maintain traceability and audit controls—a critical requirement differentiating it from generic large language models (LLMs) lacking enterprise governance rigor [S17][S11].

Cloud-agnostic deployment across Azure, AWS, Google Cloud Platform (GCP), on-premises infrastructures or FedRAMP-authorized government clouds ensures customers avoid vendor lock-in while meeting stringent security demands—another pillar enhancing adoption across regulated industries [S1][S26].

Industry Context: Competitive Positioning Among Enterprise AI Providers and Cloud Giants

C3AI occupies a distinct niche as an enterprise-focused provider emphasizing integrated application platforms enriched with advanced generative capabilities—a profile somewhat differentiated from broad cloud vendors such as Microsoft Azure AI which offer wider but less specialized portfolios. Compared to peers like Palantir Technologies or BigBear.ai who also target analytics-intensive enterprise use cases, C3AI’s patented intellectual property particularly in agent orchestration provides unique barriers against commoditization [S14][S17].

The company's strategy leverages ecosystems made up of consulting powerhouses (McKinsey & Company), industrial resellers (Baker Hughes), system integrators (PwC, Capgemini), and cloud giants (AWS, Microsoft) to amplify market coverage while controlling capital intensity inherent in direct sales expansion [S12]. This collaborative channel approach helps mitigate customer concentration risks while accelerating pipeline velocity.

Growth Drivers: Generative AI Adoption, Partner Ecosystem Expansion, Customer Penetration Progress

The integration of agentic generative AI into the C3 Agentic AI Platform constitutes a leading-edge development poised to broaden use case applicability—from autonomous asset performance optimization to supply chain risk mitigation across verticals. These advancements aim to shorten deployment cycles further through tools like C3 Code allowing natural language driven application generation dramatically compressing time from concept to live solution [N1][S11].

Strategic alliances remain integral; renewed multi-year deals with partners like Baker Hughes reinforce co-selling motions in oil & gas while expansions with Fractal Analytics and Cathexis enable scale in government intelligence sectors. Such partnerships foster co-investment in domain-specific solutions accelerating go-to-market effectiveness beyond direct sales constraints [S12]

Expanding penetration into mid-market segments represents an identifiable growth runway where digital transformation demand is rising but IT budgets remain constrained—making the ability to deliver rapid ROI via pre-built applications essential [N1][S4]. Key KPIs highlighted include ARR growth rates reflective of contract renewals plus incremental expansions along with improved time-to-value performance metrics driving customer satisfaction.

Risks and Constraints: Operating Losses, Execution Challenges, Competitive Intensity, Regulatory Compliance

C3AI faces notable challenges stemming chiefly from sustained operating losses driven by heavy R&D spending essential for maintaining technology leadership—the fiscal year ended April 2026 saw net losses around $470 million contributing to a cumulative deficit nearing $1.8 billion [F1][S1]. Execution risk remains elevated given recent CEO health constraints impacting management continuity alongside ongoing effects from workforce restructuring.

Competition spans entrenched cloud providers leveraging broader platforms at scale alongside nimble startups aggressively innovating in narrow domains complicating customer acquisition dynamics. Additionally, regulatory environments such as the EU’s recently implemented AI Act impose new compliance burdens necessitating costly governance enhancements within products potentially delaying feature rollouts [S5][S27]. Privacy regulations also raise exposure risks for customer data use requiring adaptive operational controls.

High dependency on third-party cloud infrastructure entails contractual cost commitments exposing the company to penalties if consumption falls short or rapid scale is impeded—caution around managing these obligations remains paramount [S22]. These multiple factors collectively underscore sizeable execution risk requiring disciplined sales scaling post-restructuring.

What to Watch Next: Guidance Signals, Customer Metrics, Product Roadmap Milestones

Investors should monitor forthcoming quarterly updates for evidence of ARR growth acceleration alongside retention metrics signaling successful transition beyond IPD pilots into multi-year production contracts. Expansion within lighthouse accounts especially federally focused customers would indicate traction progress.

Operationally, observable improvement in sales efficiency ratios post-labor reductions would validate restructuring intent. Product roadmap milestones encompassing generative AI feature enhancements such as expanded autonomous workflow capabilities or new industry-specific applications would signal continued innovation leadership inline with stated strategy [N1][S2]. Strategic partnership developments or additional reseller agreements may further indicate scaling momentum.

Financial Overview: Balance Sheet Strength & Operating Cash Flow

As of April 30, 2026, C3AI held approximately $66 million in cash and equivalents against current liabilities just over $106 million resulting in a strong current ratio near 6.6x which reflects robust near-term liquidity buffered by positive working capital balances [F1]. Despite this cushion, the company continues generating significant negative operating income approaching $498 million during fiscal 2026 reflecting ongoing investments in R&D and go-to-market capability buildout [F1].

The cash runway supported by existing reserves coupled with cost-saving measures implemented through restructuring are intended to sustain product development momentum while addressing path-to-profitability challenges over the medium term.

This analysis leverages detailed disclosures from C3AI’s latest SEC filings alongside reported market developments without forecasting financial outcomes or making investment research views. It highlights the intersection of operational adjustment efforts with technology advancements driving competitive positioning within the dynamic Enterprise AI software sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments