Nucor’s Integrated Steel Model Strengthens with Recycling Scale and Share Repurchase Strategy

Nucor Corporation leverages its leading recycling capabilities and diverse steel production footprint to deliver robust earnings growth and disciplined capital allocation.

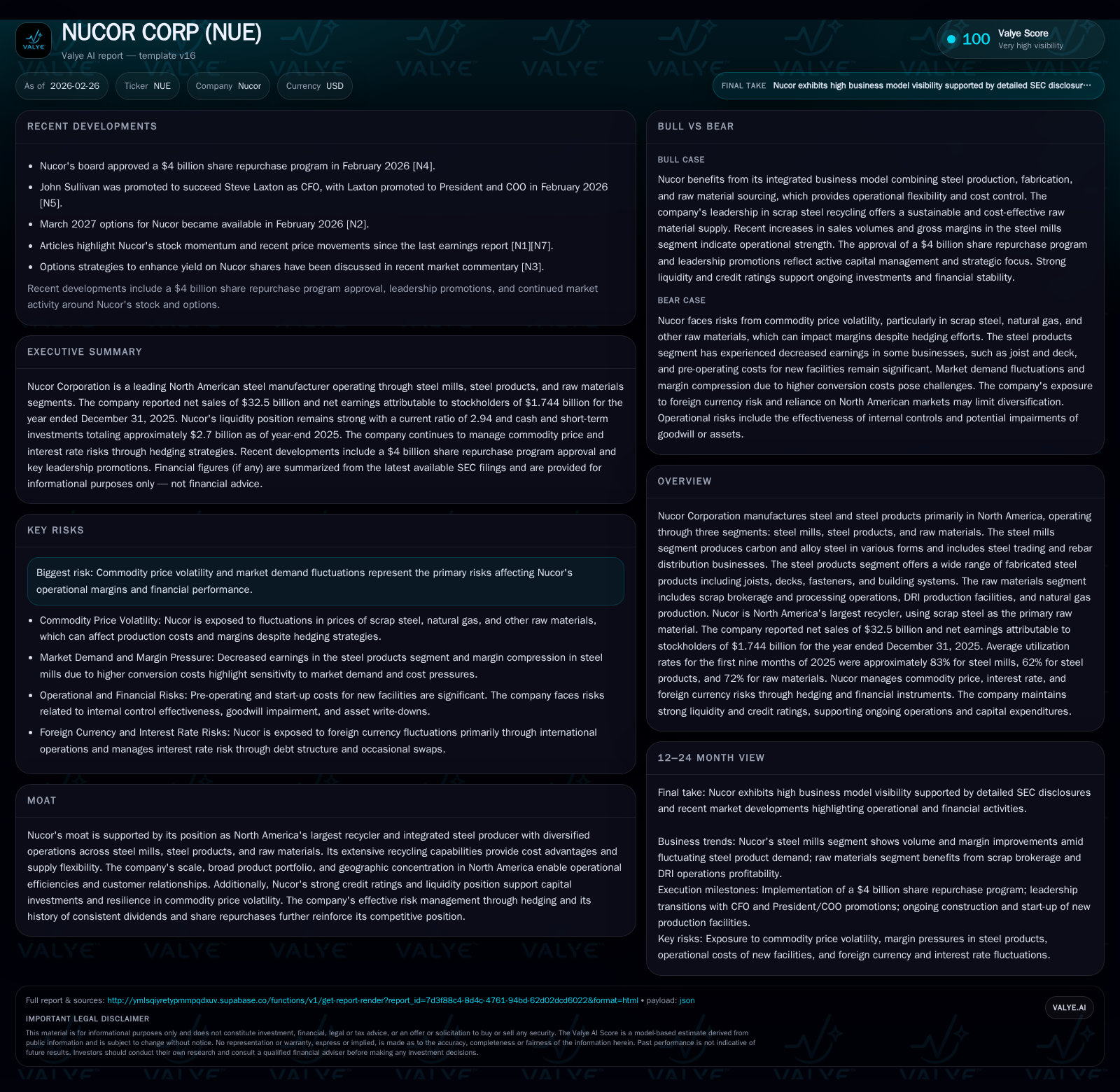

Nucor Corp recorded a strong rebound in net income to $1.744 billion in FY2025, driven by higher metal margins and volume gains, despite moderation in cash flow from operations. The company operates through three interrelated segments—steel mills, steel products, and raw materials—with integrated scrap processing as a core competitive advantage. Capital allocation has prioritized dividends plus substantial share repurchases, including a new $4 billion buyback authorization. Going forward, demand volatility in steel markets and commodity price swings remain principal risks, but Nucor’s scale, operational flexibility, and investment in DRI production support resilience.

Company Overview and Industry Position

Nucor Corporation stands as North America's premier recycler of scrap steel and an integrated steel producer with operations spanning three main segments: steel mills, steel products, and raw materials [S1]. The company's manufacturing footprint primarily serves the North American market but includes trading operations internationally [S2]. Nucor's vertically integrated model allows it to recycle scrap into steel while leveraging direct reduced iron (DRI) facilities in Trinidad and Louisiana for input flexibility [S1][S8]. This positions Nucor uniquely amidst fluctuating commodity prices and shifting demand cycles.

Historical Performance and Earnings Drivers

In fiscal year 2025, Nucor delivered net earnings attributable to stockholders of $1.744 billion, a dramatic rise from $287 million the prior year—a gain of over 500% year-over-year [F1]. This rebound reflects improved metal margins mainly driven by higher selling prices relative to scrap cost increases plus volume growth across key segments [S22][S23]. The average utilization rate at the steel mills segment hit roughly 83% during the first nine months of 2025, compared to around 77% in the same period of 2024 [S2], indicating better capacity use.

The table below summarizes key financial metrics from 2022 to 2025 consolidating reported figures from SEC filings:

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | Capex ($bn) | Net YoY |

|---|---|---|---|---|

| 2025 | 1744 | 3.2 | 3.4 | +507.7% |

| 2024 | 287 | 4.0 | 3.2 | -63.5% |

| 2023 | 785 | 7.1 | 2.2 | -37.5% |

| 2022 | 1256 | 10.1 | 1.9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 0.7 | -0.2 | 8.3 |

| 2024 | 2.2 | 0.8 | 1.4 |

| 2023 | 1.6 | 4.9 | 3.8 |

| 2022 | 2.8 | 8.1 | 6.8 |

Source: SEC companyfacts cache [F1].

¹ Estimated approximate rates due to incomplete revenue figures for prior years.

The operating cash flow seen a decline in absolute terms from previous years despite the net income surge reflecting working capital dynamics amid changing inventory and receivables balances [S7]. Capital expenditures increased steadily in line with plans to expand capacity including investments in newer sheet mills such as West Virginia [S4][S14].

Segment Composition and Financial Contributions

Nucor’s reporting structure breaks down performance into Steel Mills (carbon/alloy steels plus trading), Steel Products (fabricated items like joists, decks), and Raw Materials (scrap brokerage & processing, DRI production) [S8][S23]. In total, these segments generated close to $32.5 billion revenue excluding intercompany activity during FY2025.

Margins expanded particularly within the Steel Mills segment due to favorable metal spreads between selling prices and scrap costs despite scrap costs rising modestly (around +3%) [S22]. Steel products volumes grew but pricing pressures impacted average sales price per ton lowering segment earnings slightly excluding impairment effects seen in prior periods [S2]. Raw materials benefited from higher selling prices and volume growth primarily through The David J Joseph Company’s brokerage operations.

Growth Prospects and Strategic Initiatives

Growth headwinds remain tied to the cyclical nature of steel demand and commodity market swings which influence margin sustainability—this was highlighted as the primary risk factor by management [S21]. However, Nucor’s expanding DRI output offers a controllable alternative to scrap supply constraints that could buffer input cost inflation spikes especially if prime scrap tightens due to heightened domestic production demand [S1][S22].

Recent strategic decisions include ceasing pursuit of a new rebar micro-mill in the Pacific Northwest to optimize existing asset footprint efficacy and leverage supply chain advantages from current locations [S12]. Capital expenditures continue funding modernization of mills aiming at efficiency improvements alongside environmental compliance investments required at facilities such as the Louisiana DRI plant facing regulatory scrutiny [S21].

Forecasts and Near-Term Milestones

While explicit forward guidance on profit or revenue targets is not broadly offered, management anticipates modest margin compression risks within the steel mills segment amidst resilient order backlogs but expects stable performance from steel products and raw materials through Q3-2025 [S24]. Utilization improvements remain an indicator to watch given their correlation with profitability swings.

Close surveillance of commodity cost trends (scrap, alloys, natural gas), regulatory updates related to environmental settlements, and macroeconomic demand signals will be critical milestones influencing short-term outcomes [S21][N1]. Leadership changes at CFO level announced early February suggest emphasis on financial discipline going forward [N3].

Capital Allocation: Returns, Dividends & Buybacks

Nucor’s capital strategy emphasizes shareholder returns through both dividends and aggressive share repurchases supplemented by measured investments into capacity expansion.

The company sustained its record consecutive dividend streak into its over two hundredth quarterly payment in late-2025 with a declared annual aggregate of roughly $2.21 per share—up slightly from prior periods signaling prudent payout growth aligned with earnings improvements [F1][S15].

Share repurchases totaling approximately $700 million occurred during FY2025 down from elevated levels exceeding $2 billion in prior years reflecting operational cash flow moderation yet still affirming commitment to capital returns amid flexible liquidity positions [F1][S14][N7]. Further bolstering buyback activity was the Board's February approval of an additional uncapped $4 billion repurchase authorization replacing previous programs—permitting opportunistic stock purchases dependent on market conditions without expiration limits [N7][S14].

Despite significant capex outlays totalling over $3.4 billion aimed at modernization initiatives, free cash flow narrowly trended negative (-$188 million) given reduced operating cash flow from working capital build-ups—a pattern requiring monitoring for sustainable surplus generation beyond investment cycles [F1].

Return on equity for FY2025 approximated an estimated industry-resonant level near 8.3%, a rebound reflecting stronger profitability though still somewhat below peak levels achieved during stronger cyclical phases hinting at room for incremental efficiency gains or margin stabilization initiatives going forward [F1][S24].

Risk Factors & Regulatory Environment

As described consistently across company disclosures, Nucor faces inherent commodity price volatility risks chiefly affecting raw material procurement costs (scrap metals, alloys) along with energy inputs like natural gas used extensively in production processes—hedging strategies are employed but full mitigation is challenging due to market unpredictability [S1][S21].

Regulatory exposure is primarily linked to environmental compliance matters such as ongoing settlement negotiations related to Clean Air Act allegations at its Louisiana DRI facility where materiality thresholds have been assessed as non-significant but legal monitoring continues [S21]. Additionally, litigation reserves are maintained prudently reflecting routine business risks.

Foreign currency risk exists mainly through European trading subsidiaries but is relatively limited relative to core North American operations given geographic concentration noted by management [S1][S23]. Operational risks inherent within large-scale integrated manufacturing also persist including potential disruptions or labor issues affecting throughput.

Summary Outlook & Considerations for Monitoring

Nucor's mix of scale economies through extensive recycling operations combined with integrated upstream raw material capabilities positions it well among North American peers confronting supply-chain pressures.

Key indicators for tracking future trajectory include:

- Utilization rates across segments as proxy for demand-driven capacity deployment.

- Metal margin trends reflecting balance between raw material cost inflation vs selling prices.

- Operating cash flow evolution relative to capital spending cadence impacting liquidity buffers.

- Execution progress on new mill projects including West Virginia expansion supporting long-term growth potential.

- Regulatory developments around environmental compliance potentially influencing capital requirements or operational constraints.

- Market conditions shaping dividend policy sustainability vis-à-vis free cash flow generation.

- Share repurchase activity which guides shareholder return appetite amid valuation environment.

Adapting dynamically to fluctuating commodity markets while managing capital prudently defines Nucor’s strategic stance going forward.

This report synthesizes publicly available regulatory filings and recent news sources without providing recommendations or forecasts beyond presented factual evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments