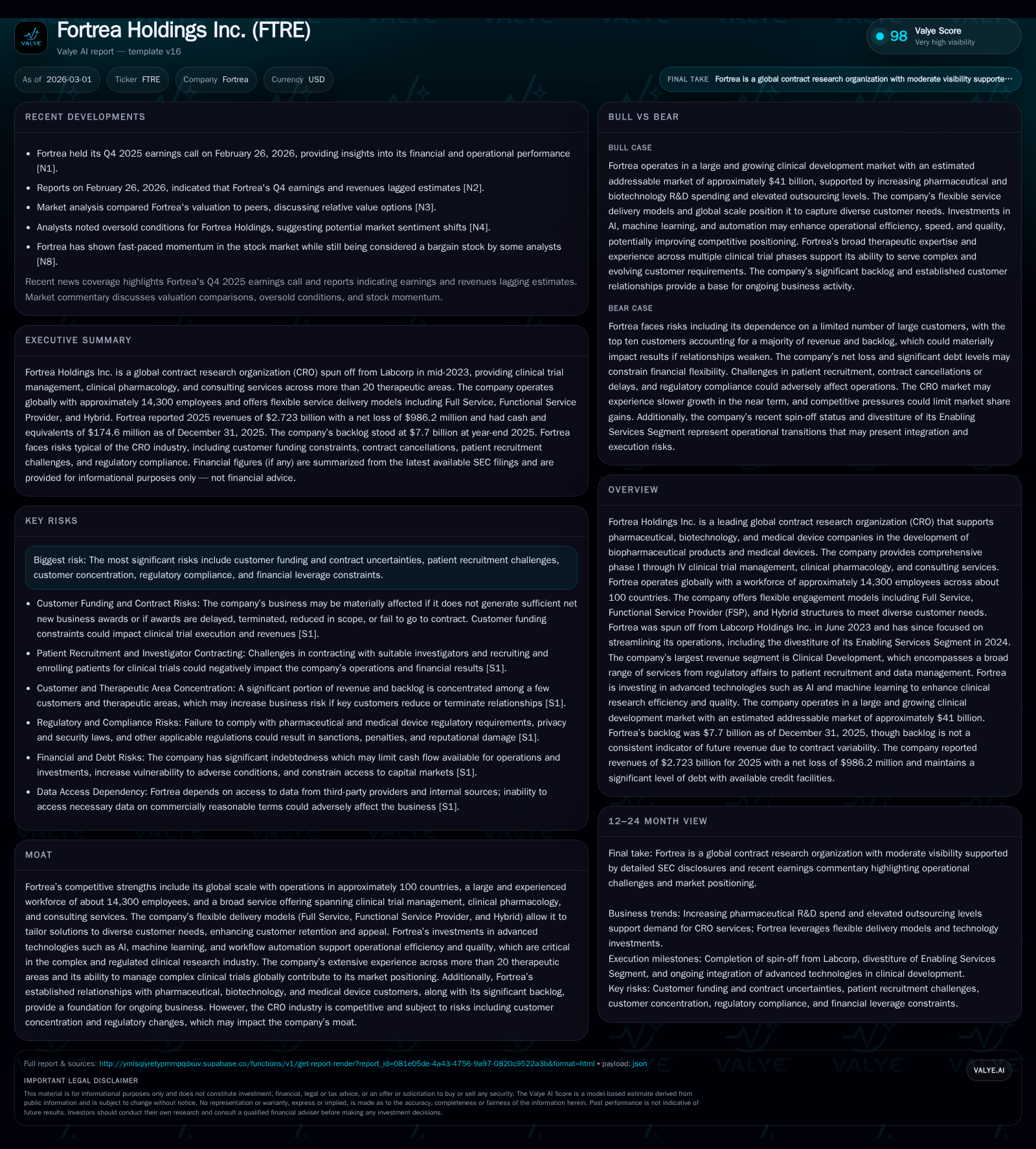

Fortrea Holdings Faces Profitability Challenges Amid Strategic Portfolio Shift and Debt Load

The newly independent CRO navigates operational restructuring, customer concentration risks, and evolving clinical trial market demands.

Fortrea Holdings Inc., a global contract research organization spun off from Labcorp in mid-2023, leverages broad clinical expertise and a flexible service model across approximately 100 countries. While operating cash flow remains positive, the company has reported significant net losses driven by restructuring costs and legacy operational challenges, alongside a substantial debt burden. Its exit from the Enabling Services segment marks a strategic focus on core clinical services but underscores transitional pressures. Customer concentration and regulatory complexities persist as notable risks in the near to medium term.

Company Overview

Fortrea Holdings Inc., established as an independent entity upon spinoff from Labcorp Holdings on June 30, 2023, operates as a global contract research organization (CRO) focused on supporting pharmaceutical, biotechnology, and medical device companies through the entire clinical development lifecycle — phases I through IV.

With approximately 14,300 employees spanning nearly 100 countries, Fortrea offers comprehensive clinical trial management, clinical pharmacology services, and consulting solutions covering over 20 therapeutic areas. The company prides itself on delivering services via a combination of Full Service (turnkey project delivery), Functional Service Provider (FSP - providing dedicated teams embedded within sponsor organizations), and Hybrid engagement models tailored to meet diverse client needs [S1][S16].

Post-spinoff operational refinement included the sale in Q2 2024 of its Enabling Services segment for $340 million to Arsenal Capital Partners’ affiliate Endeavor Buyer LLC. This divestiture aims to concentrate resources on its primary Clinical Development business unit [S1].

Historical Financial Performance

Fortrea's financials reflect typical spin-related burdens including legacy cost allocations from Labcorp operations pre-separation as well as transitional complexities linked to restructuring initiatives post-separation.

The company's operating income swung significantly negative in FY2025 at -$872.6 million compared to a loss of -$161.9 million in FY2024 but against a modest operating profit of $63.1 million from combined operations before independence in FY2023 [F1]. Net losses deepened correspondingly expanding from -$328.5 million in FY2024 to -$986.2 million in FY2025 (FY2023 was near breakeven at -$3.4 million). These steep declines largely trace to one-time charges related to the separation process, asset sales impacts including non-cash impairments, plus ongoing investments in technology transformation [F1][S1].

Operating cash flows have remained positive albeit reduced year-over-year declining from $262.8 million in FY2024 to $113.5 million by end-2025 reflecting working capital changes after receivables securitization transactions began in mid-2024 [F1][S6]. Capital expenditures stayed relatively stable near $25 million annually post-sale of non-core assets [F1]. Equity contracted substantially reflecting losses incurred from over $1.7 billion at FY2023 combined operations down to about $563.5 million by end-2025 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -986 | 114 | -873 | 25 | -200.2% |

| 2024 | -328 | 263 | -162 | 26 | -9561.8% |

| 2023 | -3 | 167 | 63 | 40 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 88 | -175.0 |

| 2024 | 237 | -24.1 |

| 2023 | 127 | -0.2 |

Source: SEC companyfacts cache [F1].

Operating income and net income swung negative post-spinoff; cash flow remains positive though subdued.

Growth Drivers and Future Prospects

Fortrea's growth outlook hinges on several interconnected factors:

- Flexible Engagement Models: Continued emphasis on flexibly deploying Full Service vs. FSP or Hybrid models supports wider client demand preferences.

- Global Scale & Therapeutic Diversity: Operating across approximately 100 countries and servicing over twenty therapeutic fields provides resilience against geographic or therapy-specific volatility.

- Technological Investments: Deployment of AI-enabled analytics and workflow automation enhances operational efficiencies critical for meeting heightened regulatory standards across markets [S15].

- Industry Trends: Outsourcing levels among large biopharma clients remain elevated as companies seek cost-effective trial execution; although short-term growth may slow due to macroeconomic pressures creating cautious R&D budgeting [S12].

- Strategic Focus Post-Divestiture: Narrowing scope to Clinical Development aligns Fortrea with areas expected to exhibit higher demand given ongoing innovation in cell/gene therapies and biosimilars.

Key constraints include customer funding uncertainties impacting contract volumes or delays; patient recruitment challenges that could affect trial timelines; concentrated revenue base wherein top ten customers represented around 57% of total revenue in FY2025 with one single customer providing ~18% posing dependency risk [S18].

Forecasts & Milestones

While explicit formal guidance was not detailed in disclosed filings as of early 2026 [N1][S1], critical indicators for tracking Fortrea’s trajectory include:

- Monitoring new business awards volumes and conversion rates amid tightening sponsor budgets.

- Completion impact assessments of Enabling Services divestiture integration benefits.

- Progress on cost control measures aimed at reducing high operating losses.

- Execution updates on technology rollouts targeting improved trial data management efficiency.

- Debt reduction plans outcome following prior tender offers for senior notes conducted during late-2025 [S4].

Investor calls point toward a multi-year horizon before returning to profitability based on current expense structures and investment programs [N1].

Returns & Capital Allocation

Return metrics are presently challenged:

- ROE stands deeply negative near -175% calculated by dividing the large net loss against diminished equity base for FY2025 [F1].

- Positive free cash flow approximated at $88.3 million (operating cash flow minus capex), signaling underlying operational cash generation despite accounting losses [F1].

- Dividends have not been declared recently; no public buyback activity noted likely due to focus on deleveraging post-spin-related indebtedness.

- Gross debt principal outstanding approximates $1.07 billion with access to a revolving credit facility largely undrawn at nearly $448 million as of end-2025 [F1][S4][S17].

Capital allocation priorities currently favor debt repayment—as evidenced by notable repayments toward term loans A and B during fiscal years ending December 31st of both 2024 and 2025—and financing strategic acquisitions or technologies remain conditional on credit market access [S4][S6][S17].

Operational & Legal Risks

Fortrea faces layered risks typical of CRO operations intensified by spin-off circumstances:

- Contract Reliance: Dependence on acquiring sufficient new contracts underpins revenue sustainability; delays or cancellations can materially harm cash flows.

- Recruitment & Site Management: Challenges recruiting investigators and enrolling patients can extend trial duration and associated costs.

- Compliance Burden: Strict regulatory regimes worldwide increase complexity; failure leads to potentially severe penalties including fines or suspension of operations [S10][S20].

- Customer Concentration: High concentration exposes the firm to sudden revenue volatility if large sponsors alter outsourcing strategies [S18].

- Litigation Exposure: Pending shareholder litigation alleges disclosure deficiencies post-spin but is considered defendable; routine professional liability claims add contingent liabilities requiring cautious insurance management [S7][S10].

- Technology Dependencies: Growing use of third-party AI systems presents risks around intellectual property rights enforcement as well as maintaining data security compliance under evolving privacy laws globally [S15][S21].

- Employment Liability Risks: Embedded Functional Service Provider arrangements necessitate robust compliance with workforce classification laws across jurisdictions lest they invite penalties or damage reputations [S14][S18].

Industry Context (Analysis)

The CRO sector is experiencing moderate near-term growth constraints driven by macroeconomic uncertainties that temper sponsor R&D expenditures despite secular trends favoring outsourcing due to innovation complexity and cost controls. The shift towards Functional Service Provider models is particularly prominent among large pharma seeking flexible resource deployment versus full-service engagements.

Consolidation within biopharma clients continues altering competitive dynamics placing premium on CRO partners offering global scalability plus technological sophistication enabling real-time data insights for accelerated approvals — areas Fortrea is actively developing capabilities around.

Conclusion & Monitoring Priorities

Fortrea Holdings navigates its formative years post-spinoff marked by heavy restructuring costs but supported by a sizable global footprint with diversified offerings essential for long-term competitiveness in clinical development services.

Critical factors warranting attention moving forward include execution success regarding cost rationalization efforts; stabilization or expansion of net new business awards amid client budget scrutiny; progress leveraging AI tools for operational advantage; managing risks tied to customer concentration; maintaining compliance amidst complex multi-jurisdictional regulations; prudent capital stewardship balancing debt reduction with growth investments.

This analysis is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments