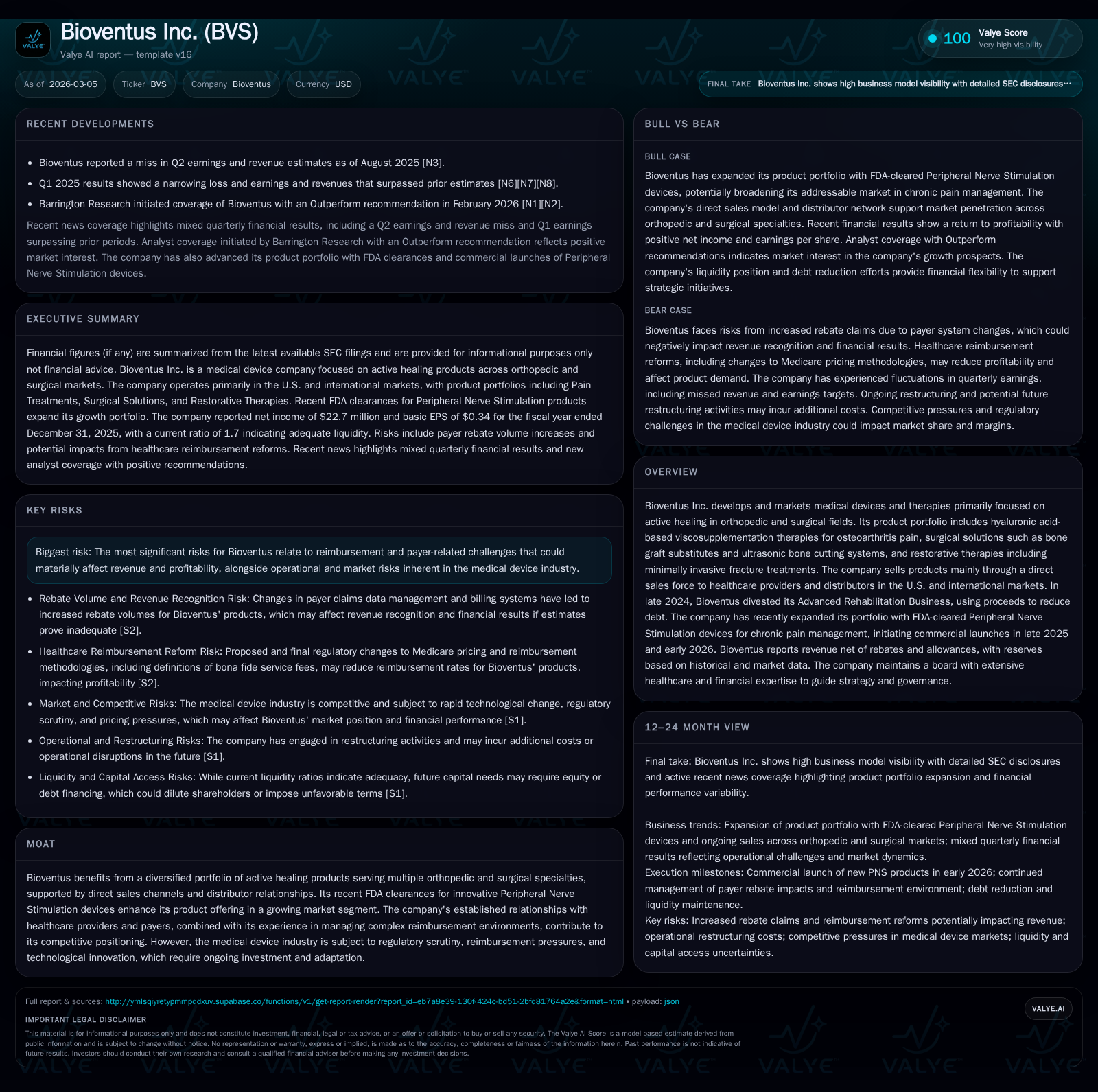

Bioventus Returns to Profit with New Product Launches and Debt Refinancing Extending Maturity to 2030

Bioventus Inc. reversed prior losses in 2025, driven by portfolio innovation, focused divestitures, and refinancing that lowered interest costs.

After years of operating losses, Bioventus Inc. reported a net income of $22.7 million for 2025, reflecting a remarkable turnaround supported by an expanded product portfolio and operational efficiencies. The company strategically divested its Advanced Rehabilitation Business in late 2024 to reduce debt and sharpen its focus on core orthopedic and surgical devices. Refinancing in mid-2025 extended debt maturities to 2030 while decreasing annual interest expenses by about $2 million. Launches of Peripheral Nerve Stimulation devices and expanded PRP offerings should fuel future growth but reimbursement risks and regulatory pressures persist.

Company Overview

Bioventus Inc., a global medical device company, focuses on active healing through orthopedic and surgical product portfolios. These include hyaluronic acid-based viscosupplementation for osteoarthritis pain, bone graft substitutes, ultrasonic surgical tools, and restorative therapies such as low-intensity ultrasound fracture treatment. More recently, the firm augmented its portfolio with FDA-cleared Peripheral Nerve Stimulation (PNS) devices addressing acute and chronic pain [S1]. Its commercial model leverages a direct salesforce complemented by distributor channels domestically and internationally.

In late 2024, Bioventus divested its Advanced Rehabilitation Business—a unit that was capital-intensive and non-core—with net proceeds of approximately $24.7 million that were largely applied towards long-term debt repayment [S14][S22]. This strategic repositioning sought to streamline operations and strengthen the balance sheet.

Historical Financial Performance

After enduring notable losses for several years due primarily to high leverage costs, operating inefficiencies and integration expenses from recent acquisitions, Bioventus achieved a significant operational turnaround in fiscal year ended December 31, 2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 23 | 75 | 54 | 3 | +167.8% |

| 2024 | -34 | 39 | -12 | 1 | +78.5% |

| 2023 | -156 | 15 | -82 | 7 | +1.6% |

| 2022 | -159 | -14 | -251 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 72 | 12.3 |

| 2024 | 38 | -22.7 |

| 2023 | 8 | -90.0 |

| 2022 | -24 | -50.1 |

Source: SEC companyfacts cache [F1].

(Source: [F1],[S1])

Key observations:

- Revenues remained generally flat around the mid-$500M range from 2024 to 2025 despite divestiture-related headwinds [S1,S14].

- Operating income swung positively by approximately $66 million year-over-year due to reduced operating expenses including successful cost containment post-divestiture [F1,S10,S25].

- Net income turned positive from large losses the past three years marking critical profitability improvement [F1].

- Operating cash flow almost doubled enabling incremental deleveraging while capital expenditures increased modestly reflecting investments in infrastructure [F1,S25].

Segment & Geographic Revenue Details

More than 90% of net sales originate within the U.S., with the remainder international markets partially served through distributors [S6,S14]. The U.S segments break down roughly as follows:

- Pain Treatments: Includes hyaluronic acid injections for knee osteoarthritis; platelet-rich plasma therapies like the XCELL PRP system which launched full market availability across Sports Medicine specialties as of August 2025 [S1].

- Surgical Solutions: Ultrasonics for precision bone resection used in spine, brain, and liver surgeries; bone graft substitutes facilitating fusion procedures.

- Restorative Therapies: Low-intensity pulse ultrasound aiding fracture healing — including plans for expanding indications to fresh fractures especially among high-risk patients.

International growth has been steady but at a lower scale; sales are conducted through distributors or direct channels depending on region [S6,S14].

Future Growth Prospects

Bioventus’s growth trajectory is underpinned by new product innovations and expansion of clinical indications:

- The commercial launch of FDA-cleared Peripheral Nerve Stimulation devices starting late 2025 marks entry into a rapidly growing chronic pain management segment offering alternatives to opioids [S1,N1,N2]. This portfolio targets both acute post-operative pain relief and longer-term neuromodulation therapy.

- Expansion plans around PRP systems leveraging synergies with existing HA injection users could boost Pain Treatment segment revenues domestically.

- Surgical Solutions benefit from aging demographics driving spine surgeries alongside technological improvements enhancing precision [S1].

- Potential broadened indications planned for restorative fracture care products targeting fresh fractures may unlock incremental revenue streams.

However, growth faces challenges particularly related to reimbursement environment uncertainties impacting pricing dynamics predominantly under Medicare Part B frameworks [S19]:

"Certain proposed legislative or regulatory reforms may reduce Medicare funding or tighten coverage criteria potentially pressuring revenue" [S19]. Additionally, recent payer claims processing changes have increased rebate volumes which could affect net realized prices though current reserves appear adequate [S2,S19].

Monitoring adoption rates of PNS devices and performance against earn-out milestones related to the Advanced Rehabilitation divestiture contingent payments will also be key indicators going forward [S14].

Capital Allocation & Financial Health

Following the sale of Advanced Rehabilitation business late December 2024 receiving net proceeds near $24.7 million (after fees), management deployed approximately $20 million towards debt reduction promptly at year-end improving leverage ratios [S14,S22].

In July 2025, Bioventus completed refinancing through execution of a new Credit Agreement providing:

- A $300 million term loan facility ($294 million outstanding at year-end post amortization)

- A $100 million revolving credit line ($98M unused with letters of credit reducing capacity slightly)

- Interest savings expected at approximately $2 million annually compared with prior agreements due to lower spread and refined structure

- Extended debt maturity pushed out to July 2030 from earlier schedules under previous agreements [S4,S5,S7]

Interest rate swaps covering half the term loan fixed a rate near ~3.6%, mitigating SOFR floating rate exposure amid rising interest rates environment [S12,S16].

Liquidity metrics remain solid with cash & equivalents around $51 million at December end plus near full revolver availability supporting operational needs without near-term liquidity concerns [F1][S6,S7].

Returns reflect the turnaround from previous losses:

- ROE approximated at ~12.3%, calculated as net income divided by equity [$22.7M / $184M] for fiscal year ended December 31, 2025 [F1]

- Free cash flow estimated above $72 million after accounting for capex investment was robust driven by operational improvements including working capital management [F1]

No dividends or share repurchases were reported during this period indicating prioritization of reinvestment and deleveraging over capital returns currently.

Risks & Uncertainties

The foremost risks facing Bioventus derive from exposure to reimbursement volatility tied to large private payers implementing billing system changes raising rebates volume unpredictably; these can materially compress revenues if reserves are inadequate or if payers further restrict payments [S2,S19].

Regulatory oversight—particularly evolving policies on Medicare Part B reimbursement methodologies—may impose pricing pressure or limit coverage scope which could affect medium-term earnings power despite ongoing product innovation aimed at enhancing value proposition [S8,S15].

Operational risks exist given competitive dynamics within orthopedics & surgical device markets requiring sustained innovation investments balanced against cost discipline [S8]. Litigation risks are limited presently after settlement of shareholder lawsuits concluded without material impact but remain potential latent exposures [S15].

Additionally, covenant compliance under the new credit facility must be maintained lest liquidity constraints arise; however current compliance is satisfactory as reported along with healthy interest coverage levels at fiscal year-end [S26,S29].

What To Watch Going Forward (Analysis)

Key metrics meriting attention will include:

- Uptake velocity and clinical feedback related to Peripheral Nerve Stimulation across targeted pain segments,

- Progress toward broadening fracture care indications,

- Impact trajectory regarding payer rebate volumes especially as more claims data accrue,

- Margins sustainability amid cost inflation risks,

- Achieving potential earnout targets linked to former Advanced Rehabilitation Business,

- Maintaining covenant compliance amid macroeconomic uncertainties impacting capital markets access,

- R&D pipeline developments sustaining next-generation innovation beyond current launches.

Enhancing international presence remains an opportunity but requires careful channel expansion aligned with regulatory variation globally.

Summary Impression

Bioventus has navigated an impressive financial turnaround from several years of steep losses driven mainly by high leverage burdens and restructuring costs into sustainable profitability accompanied by strengthened liquidity following strategic asset divestitures and thoughtful refinancing anchored until mid-decade next horizon. Innovation-driven portfolio expansion notably via Peripheral Nerve Stimulation represents promising avenues supporting growth prospects while offsetting pressures facing legacy segments tied closely to reimbursement trends. Continued vigilance around payer dynamics remains imperative alongside disciplined capital management as Bioventus seeks to capitalize on its broad active healing platform spanning multiple orthopedic specialties with tailored commercial execution.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments