MediWound Ltd. Faces Revenue Decline Amid Investment in Manufacturing and R&D Expansion

The Israeli biopharmaceutical company balances a shrinking top line with significant capital allocation towards capacity expansion and advanced wound care development.

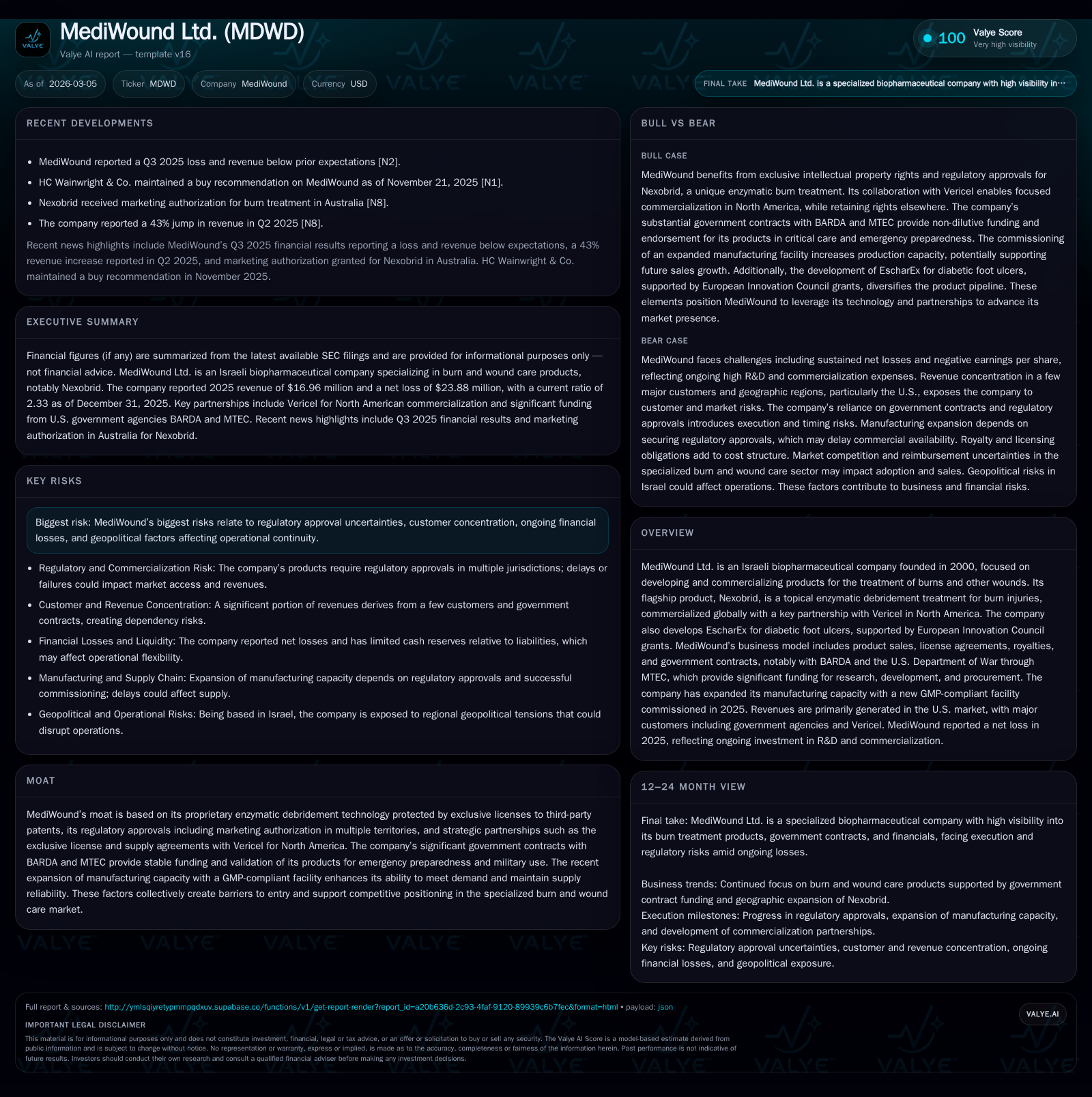

MediWound Ltd. operates in the specialized burn and wound treatment sector with its flagship product Nexobrid, supported by robust government contracts and key partnerships. Despite a 16% revenue decline in 2025, the company has invested heavily in expanding manufacturing capacity via a new GMP-compliant facility and sustained growth in R&D expenses, particularly for its diabetic foot ulcer product EscharEx. Persistent net losses highlight operational challenges amid high execution costs, while government funding through BARDA and MTEC remains crucial. The company's liquidity profile shows a healthy current ratio with active equity raises backing its strategy, but customer concentration and regulatory uncertainties suggest ongoing risk factors.

Company Overview

MediWound Ltd., founded in Israel in 2000, specializes in enzymatic debridement treatments targeting burns and chronic wounds such as diabetic foot ulcers. Its flagship commercial product Nexobrid is distributed worldwide with significant presence in the U.S. through an exclusive license agreement with Vericel Corporation. The company is also developing EscharEx for venous leg ulcers (VLU), supported by European Innovation Council grants.

The business model combines product sales revenues, licensing agreements including royalties from Vericel, and substantial government contracts principally from U.S. federal agencies BARDA (Biomedical Advanced Research and Development Authority) and MTEC (Medical Technology Enterprise Consortium), which support emergency preparedness initiatives.

Historical Financial Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 17 | -24 | -16.1% | +21.0% |

| 2024 | 20 | -30 | +8.2% | -350.0% |

| 2023 | 19 | -7 | -29.5% | +65.7% |

| 2022 | 26 | -20 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -54.7 |

| 2024 | -97.0 |

| 2023 | -21.3 |

| 2022 | -179.6 |

Source: SEC companyfacts cache [F1].

Revenues declined notably to $16.96 million in FY2025 from $20.22 million in FY2024. While net losses persist at $23.88 million for FY2025, there was a year-over-year improvement of approximately 21%. This reflects ongoing investment in research & development and manufacturing scale-up efforts.

Growth Outlook

Manufacturing Expansion: In 2025, MediWound commissioned a new GMP-compliant manufacturing facility dedicated to Nexobrid production designed to increase capacity up to six times prior levels [S17]. This expansion supports anticipated demand linked to government stockpiling programs.

Pipeline Development: The EscharEx candidate is advancing through pivotal Phase III trials under the VALUE program with contractual commitments exceeding $18 million over multiple years [S17]. Success could extend the company’s reach into chronic wound care markets.

Partnership Revenues: The licensing agreement with Vericel includes upfront payments received and potential milestone payments plus royalty streams based on sales performance [S24].

Government Funding: Contracts with BARDA and MTEC provided over 60% of total revenues in recent years underscoring reliance on these agencies for funding related to biodefense applications [S22].

Risks include regulatory hurdles inherent to biopharmaceutical products; geopolitical instability given Israeli headquarters location; concentrated customer base; and continued negative earnings necessitating capital support.

Capital Allocation & Financial Position

At December 31, 2025, cash and cash equivalents stood at approximately $4.8 million against current liabilities of about $25.7 million ([F1]), yielding a current ratio near 2.33x indicative of sound short-term liquidity.

Capital raises have been significant:

- A registered direct offering completed in late 2025 generated gross proceeds of around $30 million at $17.30 per share [S9].

- Series A warrant exercises contributed nearly $4.7 million over recent years.

Research & development expenses rose markedly from approximately $8.9 million in FY2024 to about $14.3 million in FY2025 reflecting intensified pipeline activities including clinical trials on EscharEx [S7][S8].

No dividends or share repurchases have been reported due to reinvestment priorities amid operating losses [S9]. Return on equity remains negative at roughly -55%, consistent with net losses relative to equity of about $43.6 million at FY25 end [F1].

Geographic & Customer Concentration

Approximately 70% of revenues derive from the United States driven chiefly by government contracts (BARDA/MTEC) and commercial agreements via Vericel [S6][S22]. European markets including Germany ($0.8m), Italy ($1m), Spain (~$1.3m) contribute more modestly.

Customer concentration is significant: BARDA and MTEC together account for about two-thirds of revenues while Vericel contributes around 6%, with no other customers exceeding single-digit shares individually [S22]. This concentration elevates counterparty risk depending on government policy continuity.

Risks Summary

Key risks include regulatory approval uncertainties for pipeline products; dependence on a small number of large customers; ongoing operating losses requiring capital raises; geopolitical tensions affecting Israeli operations; intellectual property licensing constraints; currency exposure; commercialization challenges outside core territories; and industry-specific litigation or compliance risks typical for pharmaceutical companies [S13][S15][S27].

Conclusion & Monitoring Points

MediWound is positioned between strengthening its burn care leadership through enhanced manufacturing capacity while advancing clinical-stage assets such as EscharEx amid persistent losses demanding prudent capital management.

Investors should monitor:

- Clinical trial progress for EscharEx,

- Renewal or extension of BARDA/MTEC contracts beyond current terms,

- Commercial uptake trends reported by Vericel affecting royalty income,

- Geopolitical developments impacting operational continuity,

- Liquidity relative to capital expenditure plans,

- Regulatory filings related to next-generation wound care products.

This report is based solely on publicly available SEC filings as of March 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments