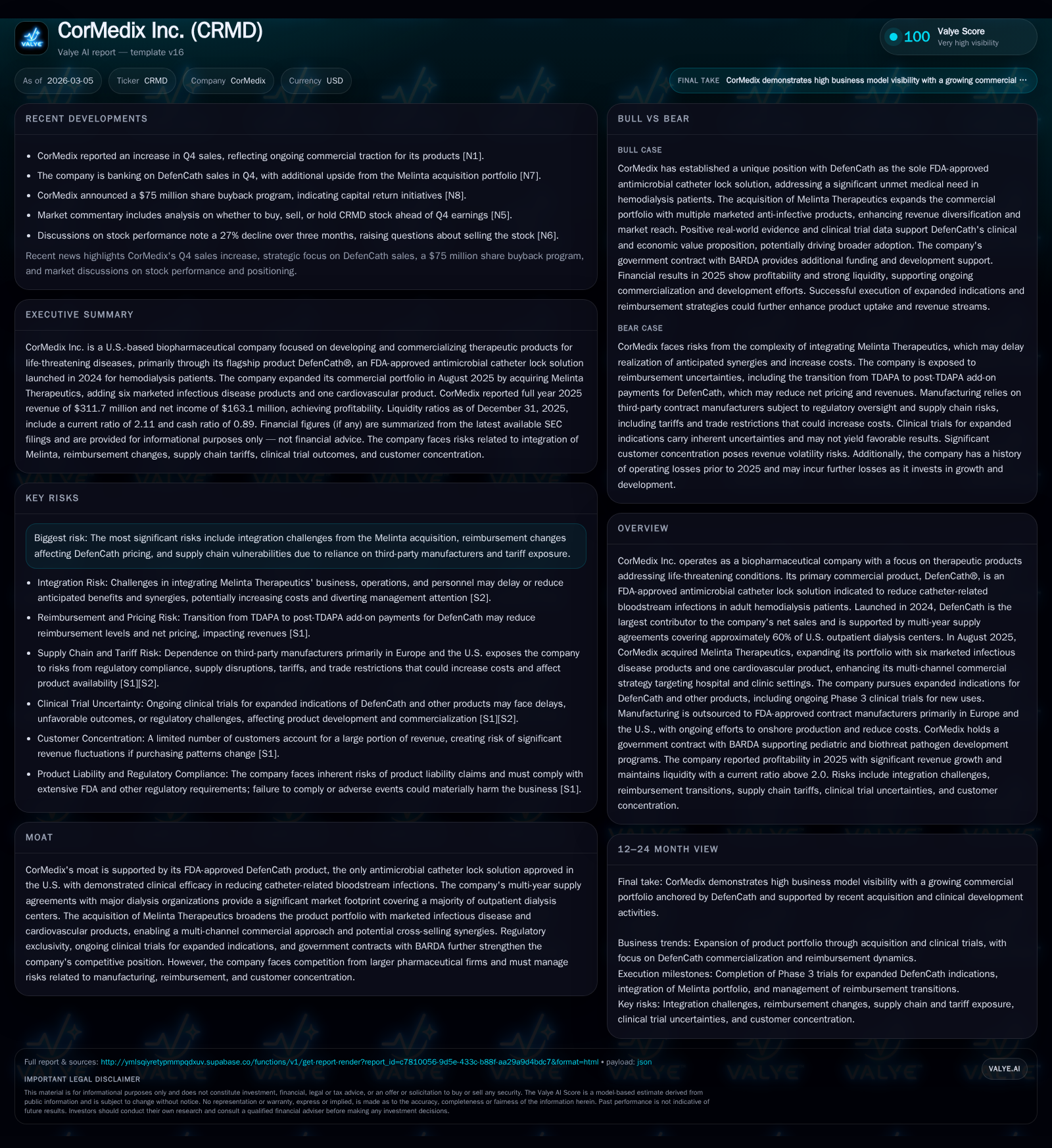

CorMedix Surges on DefenCath's Market Expansion and Strategic Acquisition Push

DefenCath’s commercial ramp alongside the Melinta acquisition propelled CorMedix’s 2025 financial turnaround amid integration and reimbursement risks.

CorMedix Inc. achieved a dramatic financial turnaround in 2025, transitioning from years of losses to profitability largely driven by the commercial launch of DefenCath®, the only FDA-approved antimicrobial catheter lock solution for adult hemodialysis patients. The company accelerated growth with its August 2025 acquisition of Melinta Therapeutics, broadening its infectious disease and cardiovascular product portfolio and enabling a multi-channel commercial strategy across hospital and outpatient settings. Despite impressive revenue growth and operating cash flow generation, ongoing integration challenges, regulatory compliance demands, and reimbursement uncertainties present risks to sustained expansion. Market watchers should track regulatory milestones, sales traction beyond hemodialysis, and synergy realization from the Melinta acquisition.

A Turning Point: CorMedix’s Revenue and Profit Leap in 2025

CorMedix executed one of the most remarkable financial turnarounds among small-cap biopharma companies in recent years. After enduring multi-year net losses exceeding $17 million annually through 2022-24, the company delivered revenue of approximately $312 million in FY2025 — a staggering increase of about 617% compared to $43.5 million in FY2024 [F1]. Operating income reversed course from a $22.4 million loss in FY2024 to a profitable $150.1 million in FY2025, while net income escalated by over tenfold from a loss of nearly $18 million to earnings of $163.1 million [F1]. This translated into an approximate return on equity of 40%, considering year-end equity of roughly $405 million [F1].

Simultaneously, operating cash flow turned positive at $175 million in FY2025 after years of negative cash flows, reflecting improved business scalability amid product commercialization [F1]. Capital expenditures rose modestly but remained low relative to cash inflows at about $2.26 million [F1]. The company ended the year with solid liquidity metrics evidenced by a current ratio above 2.0, underscoring robust financial discipline [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 312 | 163 | 175 | 150 | +617.0% | +1009.4% |

| 2024 | 43 | -18 | -51 | -22 | +66363.1% | +61.3% |

| 2023 | 0 | -46 | -38 | -49 | 0.0% | -56.0% |

| 2022 | 0 | -30 | -24 | -31 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 173 | 40.2 |

| 2024 | -51 | -21.2 |

| 2023 | -39 | -66.1 |

| 2022 | -25 | -53.9 |

Source: SEC companyfacts cache [F1].

DefenCath commercial launch and Melinta acquisition catalyzed the surge.

DefenCath Takes the Helm: Launch, Approval, and Market Penetration Insights

At the core of this transformation is DefenCath®, an FDA-approved antimicrobial catheter lock solution containing taurolidine and heparin formulated specifically to reduce catheter-related bloodstream infections (CRBSIs) for adult patients receiving chronic hemodialysis via central venous catheters (CVCs). Securing FDA approval on November 15, 2023 [S1], CorMedix launched DefenCath commercially in April 2024 for inpatient use followed by outpatient hemodialysis centers starting July 2024 [S1][S3][N7].

DefenCath holds the distinction as the sole FDA-approved antimicrobial catheter lock solution in the U.S., positioning it firmly to address CRBSI risk—a critical concern given these infections cause increased morbidity, hospitalization costs, and mortality among dialysis patients.

The product secured multi-year supply agreements covering around sixty percent of U.S outpatient dialysis centers operated by major dialysis organizations [S1][N7]. This scale offers considerable market penetration leverage but also raises dependency on key partnerships for continued adoption.

Melinta Acquisition: Bolstering Portfolio Amid Integration Complexities

Strategically broadening its commercial reach beyond dialysis-focused products, CorMedix acquired Melinta Therapeutics on August 29, 2025 [S1][S2][N7]. This bolt-on transaction brought six marketed anti-infective therapies targeting serious gram-positive, gram-negative bacterial infections as well as fungal infections—products such as REZZAYO®, MINOCIN IV®, VABOMERE®, KIMYRSA®, ORBACTIV®, BAXDELA®—and Toprol-XL®, a well-established cardiovascular medication [S1].

This acquisition critically expands CorMedix’s multi-channel commercial strategy into hospital ecosystems including emergency departments, outpatient clinics, and home infusion care settings where these infectious disease assets are primarily used.

However, management has explicitly flagged integration execution risks including operational disruption due to differing corporate cultures and management styles between the legacy CorMedix and Melinta teams; retention challenges for key personnel pivotal to commercial success; diversion of leadership attention; unforeseen expenses; and possible delays realizing synergy targets [S2]. Protracted or costly integration could temper near-term margin expansion despite top-line growth opportunities.

Clinical Progress and Regulatory Risks: The Road Ahead for Expanded Indications

Beyond its current label for chronic hemodialysis patients with CVCs, CorMedix is conducting ongoing Phase 3 clinical studies exploring DefenCath’s use for reducing central line-associated bloodstream infection (CLABSI) incidence in adult patients receiving total parenteral nutrition (TPN), a population similarly vulnerable to bloodstream infections but distinct from dialysis cohorts [S1][S6].

Regulatory compliance post-approval presents a demanding operational landscape involving extensive pharmacovigilance for adverse event reporting; adherence to continuous current Good Manufacturing Practice (cGMP) requirements enforced by the FDA through unannounced inspections; constraints on promotional claims strictly aligned with approved labeling; requirement to conduct pediatric post-marketing studies per PREA regulations; supply chain security controls; and adherence to evolving healthcare laws around drug promotion [S4][S5][S6][S20].

Failure or delays arising from clinical or regulatory hurdles could stifle growth prospects or necessitate costly corrective actions including labeling revisions or enforcement sanctions.

Financial Backbone: Capital Allocation, Cash Flow Strength, and Share Buyback Program

CorMedix leveraged its improved profitability profile in early-2026 announcements revealing a substantial $75 million share buyback program designed to return capital to shareholders while signaling confidence in intrinsic value appreciation potential [N8]. Free cash flow generation remains healthy at approximately $173 million after subtracting modest capex from operating cash flow ($175M - $2.26M = ~$172.8M) in FY2025 [F1], providing ample internal funding flexibility.

Cash & equivalents totaled roughly $145 million at year-end while working capital remained comfortably positive with current assets more than double current liabilities ($367M vs $174M), highlighting liquidity robustness that supports ongoing R&D investment as well as operational scale-up without immediate reliance on external financing [F1].

Market Positioning: Competitive Pressures and Reimbursement Landscape

While DefenCath enjoys regulatory exclusivity as the lone FDA-approved antimicrobial catheter lock solution indicated specifically for CRBSI reduction in U.S hemodialysis patients via CVCs [S1], CorMedix confronts competitive threat dynamics from larger pharmaceutical incumbents potentially developing equivalent or superior therapies [S1][S6]. Sustaining market leadership depends heavily on maintaining coverage and reimbursement from government payers including Medicare/Medicaid programs as well as private insurers.

Reimbursement presents pronounced risks given ongoing U.S legislative initiatives such as CMS's GENEROUS Model promoting supplemental rebates tied to international reference pricing benchmarks—mechanisms that could compress pricing power or shift coverage favorability away from higher-priced novel therapies like DefenCath over time [S6][S14]. Reimbursement uncertainty therefore bears significantly on realized margins and adoption velocity.

Investor Watchpoints: Upcoming Milestones, Commercial Traction, and Risk Factors

Explicit forward-looking guidance remains limited as CorMedix navigates multiple moving parts encompassing clinical development timelines for label expansions especially related to TPN patient populations; effective integration—and synergy capture—from Melinta Therapeutics products spanning infectious disease hospitals channels; evolving reimbursement frameworks within federal programs impacting product pricing strategies; manufacturing rigor sustaining cGMP compliance without disruption; patent litigation particularly concerning Minocin Injection that could expose generics entry risk; cybersecurity safeguards protecting data integrity amidst third-party reliance; plus product liability insurance adequacy protecting against adverse event claims [N3][S13][S15][S16][S18][S21][S22].

Future performance hinges on financially materializing expanded indications approval wins; growing sales penetration beyond dialysis exclusively into adjacent hospital segments enabled by Melinta assets; managing supply chain efficiencies post-acquisition; preserving exclusivity windows amidst IP challenges; navigating reimbursement pressures tactically.

This analysis synthesizes CorMedix’s recent performance milestone disclosures alongside detailed SEC filing risk discussions to provide an evidence-grounded view without recommendation bias or speculative forecast extrapolation. Continued due diligence around regulatory updates, commercial feedback loops including real-world effectiveness data capturing reduction in CRBSIs incidence rates post-DefenCath usage adoption—in addition to effective integration execution—will be essential lenses through which stakeholders can evaluate CorMedix’s evolving valuation underpinnings.

-- Analysis by Valye News --

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments