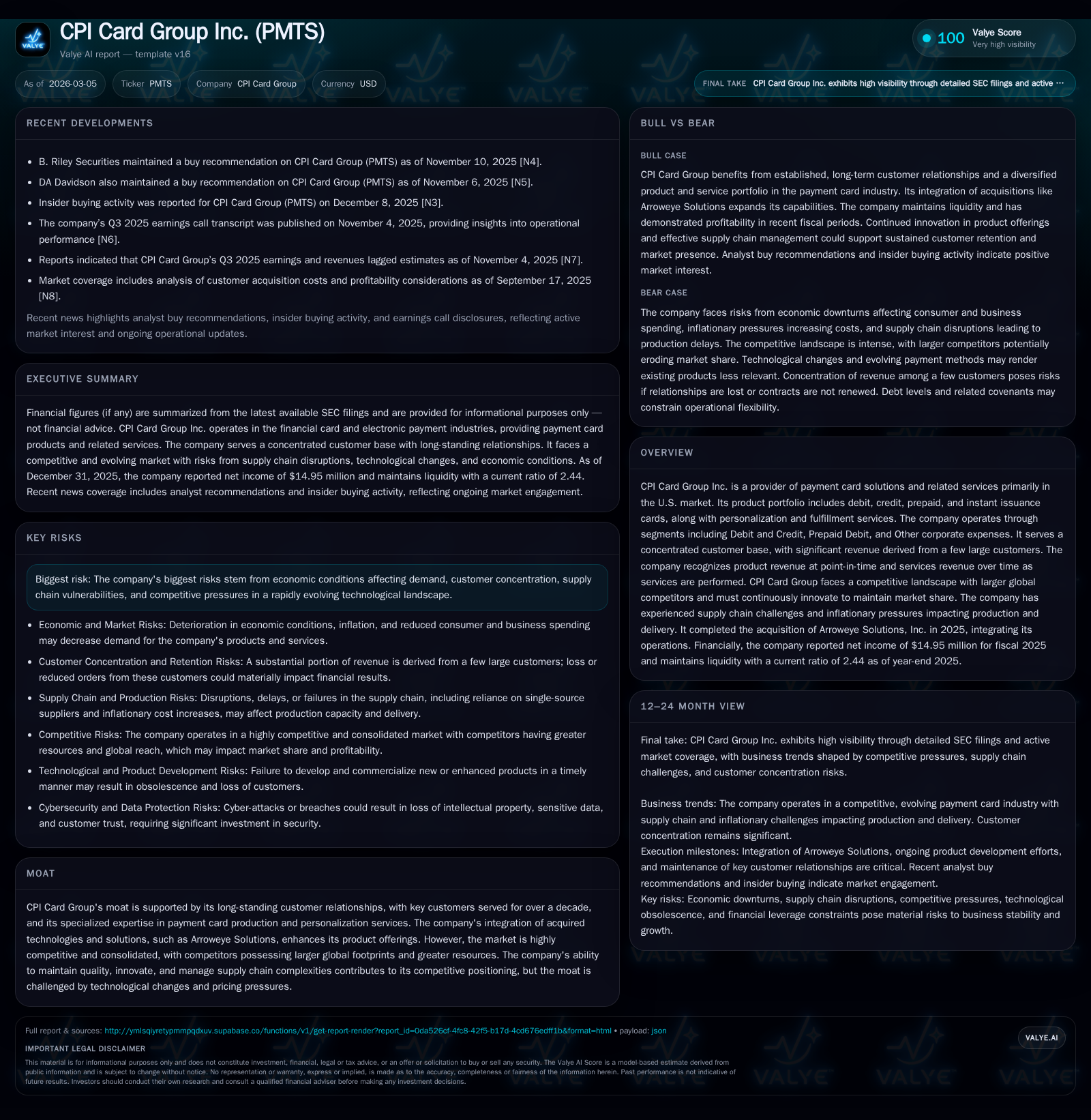

CPI Card Group Navigates Growth Amid Margin Pressures and Strategic Investments

Fiscal 2025 results highlight CPI Card Group’s revenue growth and cash flow strength, counterbalanced by margin compression and increased capital expenditures.

CPI Card Group Inc. reported a 15.9% revenue increase in fiscal 2025 to $84.14 million, driven by sustained demand across its card products and personalization services [F1]. Despite top-line growth, operating income declined 12.7% to $54.8 million due to inflationary pressures and supply chain challenges, while net income fell 23.4% to $14.95 million [F1][S1][S8]. Operating cash flow rose 37.4% to $59.5 million, supporting significant capital investments including a near doubling of capex to $18.2 million focused on capacity expansion and technology upgrades [F1][S16]. The company maintains substantial leverage with over $308 million in long-term debt and negative equity impacting return metrics [F1][S4][S18]. Customer concentration remains high, with one customer representing approximately 16% of revenues and the top ten accounting for more than half [S5]. Strategic integration of Arroweye Solutions aims to enhance product offerings but poses near-term earnings headwinds [N3].

Historical Financial Performance

CPI Card Group demonstrated notable revenue growth in fiscal year 2025, achieving $84.14 million—a 15.9% increase from the prior year—driven by steady demand for its core debit, credit, prepaid card products and personalization services [F1]. However, this top-line expansion was accompanied by a contraction in operating income which declined by 12.7% to $54.8 million despite higher sales volumes, reflecting margin pressures from inflationary cost increases and supply chain disruptions [F1][S8]. Net income fell more sharply by 23.4%, reaching $14.95 million as increased per-unit costs and acquisition-related expenses weighed on profitability [F1][N3].

Operating cash flow bucked this downward earnings trend, rising significantly by 37.4% to $59.5 million due to improved working capital management and effective cash conversion during the period [F1]. This robust cash generation supported substantial capital investments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 15 | 60 | 55 | 18 | -23.4% |

| 2024 | 20 | 43 | 63 | 9 | -18.6% |

| 2023 | 24 | 34 | 62 | 6 | -34.4% |

| 2022 | 37 | 31 | 79 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 9 | 41 | -86.3 |

| 2024 | 9 | 34 | -54.8 |

| 2023 | 0 | 28 | -46.2 |

| 2022 | 13 | -44.5 |

Source: SEC companyfacts cache [F1].

Margin Pressures from Supply Chain Challenges

Margin compression is attributed primarily to extended production lead times resulting from global supply chain constraints and inflationary cost pressures impacting raw materials and logistics [S1][S8]. CPI Card Group’s reliance on single-source suppliers has contributed to these delays, increasing holding costs and complicating delivery schedules.

Pricing flexibility is limited due to competitive dynamics and contract terms that generally lack exclusivity or guaranteed order volumes, constraining the company's ability to fully offset input cost increases through price adjustments [S8][S1]. Gross profit margins have slightly contracted below historical averages typically in the low-30s percentage range.

Customer Concentration Risks

Customer concentration remains a material risk factor; one customer accounted for approximately 16% of total revenue in fiscal year 2025 while the top ten customers—including resellers—represented more than half of sales [S5]. These relationships are longstanding but non-exclusive contracts contribute to potential volatility in order volumes.

Competitive pressures from larger firms with scale advantages exert pricing pressure on CPI’s offerings while periodic customer audits under third-party risk management programs add operational costs and may influence contract renewals or terminations [S6].

Acquisition Integration: Arroweye Solutions

The strategic acquisition of Arroweye Solutions enhances CPI’s product portfolio with advanced instant issuance technologies aligned with growing demands for payment card personalization [N3]. This acquisition supports differentiation amidst evolving fintech program manager needs.

However, near-term earnings have been impacted by integration costs including systems alignment and operational assimilation alongside supply chain challenges affecting production facilities post-acquisition.

Capital Allocation and Liquidity Position

Capital expenditures surged nearly twofold to $18.2 million in fiscal year 2025 reflecting investments in capacity expansion and technology upgrades related to Arroweye integration among other initiatives [F1][S16]. Concurrently, liquidity was bolstered by an amendment increasing the asset-based lending revolver capacity from $75 million to $100 million providing additional financial flexibility [S4].

Despite strong cash flow generation supporting free cash flow estimated at about $41.3 million (operating cash flow less capex), dividend payments remain absent due to restrictions imposed by debt covenants limiting distributions including share repurchases which have been modest historically [F1][S22]. Some debt reduction occurred via planned redemptions on senior notes but overall leverage remains significant.

Balance Sheet Overview and Return Metrics

As of December 31, 2025, CPI holds long-term debt net of current maturities exceeding $308 million with negative shareholders’ equity approximating -$17.3 million reflecting accumulated losses over prior periods [F1][S4][S18]. The current ratio stands at a healthy approximately 2.44x indicating adequate short-term liquidity coverage [F1].

High leverage weighs on return on equity metrics which approximate negative 86%, highlighting challenges in generating shareholder value given the capital structure dynamics.

Forward-Looking Considerations

Looking ahead, CPI Card Group faces multiple risks including the accelerating adoption of digital wallets potentially reducing demand for physical cards, cybersecurity threats necessitating ongoing IT investments, supply chain fragility affecting production reliability, and intense competition impacting pricing power within a consolidated market landscape [S1][S6].

Investors will monitor forthcoming quarterly reports post-segment realignment effective Q1-2026 that may provide clearer insights into revenue mix shifts following Arroweye integration as well as progress on supply chain normalization efforts and customer retention outcomes.

This analysis is based exclusively on publicly available information including SEC filings and press releases without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments