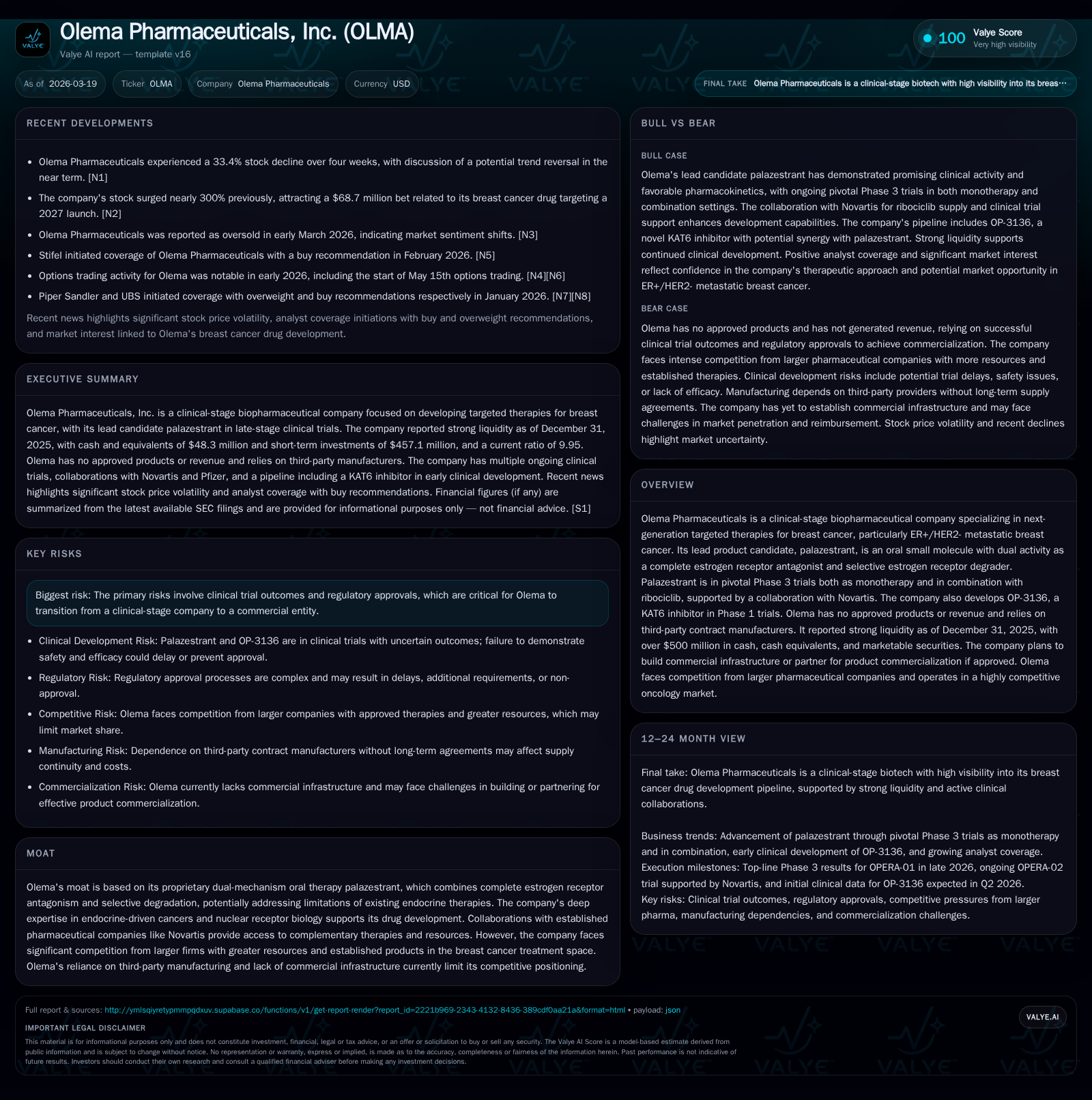

Olema Pharmaceuticals Poised for Breast Cancer Breakthroughs with Palazestrant

Olema’s dual-mechanism oral therapy palazestrant drives late-stage trials in metastatic ER+/HER2- breast cancer amid strong cash reserves and key upcoming milestones.

Olema Pharmaceuticals focuses on next-generation endocrine therapies for ER+/HER2- metastatic breast cancer, led by palazestrant, a novel CERAN/SERD oral agent progressing through pivotal Phase 3 trials both as monotherapy and combined with ribociclib under a Novartis collaboration. The company has reported widening losses consistent with clinical-stage operations but maintains robust liquidity exceeding $48 million in cash and approximately $515 million in current assets to fund ongoing development and potential commercialization. Key readouts are expected in late 2026 and 2028, setting the stage for NDA filings and possible FDA approvals. Olema faces typical biotech risks around trial outcomes and commercial infrastructure build decisions while leveraging partnerships to navigate competitive oncology markets.

Scientific Foundation and Differentiated Therapy Approach

Olema Pharmaceuticals is pioneering a distinct biological approach to combat metastatic ER-positive/HER2-negative breast cancer through its lead candidate, palazestrant. Uniquely characterized as a CERAN (complete estrogen receptor antagonist) combined with selective estrogen receptor degrader (SERD), palazestrant not only binds to the estrogen receptor (ER) but comprehensively inhibits its transcriptional activity across wild-type and mutant forms implicated in endocrine resistance [S1]. This dual mechanism potentially resolves shortcomings observed with traditional SERDs that primarily degrade ER but may incompletely block residual activity.

Supporting extensive preclinical validation, palazestrant demonstrates favorable pharmacokinetic profiles allowing durable drug exposure alongside an encouraging tolerability window. Notably, the compound exhibits synergy potential when co-administered with cyclin-dependent kinase (CDK)4/6 inhibitors — such as ribociclib — without significant pharmacokinetic drug–drug interactions. This integrative modality seeks to overcome acquired resistance pathways common in heavily treated metastatic populations. Additionally, Olema's pipeline includes OP-3136, an orally available KAT6 inhibitor currently in Phase 1 trials targeting epigenetic regulation relevant for oncology frameworks beyond breast cancer, signaling platform diversification [S1].

Track Record of Growth and Operational Investment

From a financial vantage point, Olema reflects hallmark traits of an innovation-driven clinical-stage biopharmaceutical company intensifying investments aligned with strategic pipeline developments. Operating income has declined markedly from -$106.9 million in FY2022 to -$178.7 million by FY2025 — equivalent to a -25.6% year-over-year change from FY2024 to FY2025 — representing escalated R&D spending necessary to fuel pivotal trials [F1]. Net losses have similarly expanded from -$104.8 million in FY2022 to -$162.5 million in FY2025. Operating cash flows have deepened into negative territory reaching approximately -$146.7 million for FY2025.

Capital expenditures remain nominal relative to expenses at approximately $159 thousand annually since FY2024, reflecting minimal fixed asset outlays indicative of outsourcing paradigms common among early commercial-stage biotechs reliant on contract manufacturing [F1]. Equity financing bolstered balance sheet strength: shareholder equity rose from $197.5 million at end-FY2022 to $478.6 million at end-FY2025 via successive capital raises supporting clinical needs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -162 | -147 | -179 | 159000 | -25.5% |

| 2024 | -129 | -104 | -142 | 159000 | -34.0% |

| 2023 | -97 | -84 | -105 | 363000 | +7.8% |

| 2022 | -105 | -82 | -107 | 363000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -147 | -33.9 |

| 2024 | -105 | -31.7 |

| 2023 | -84 | -38.1 |

| 2022 | -82 | -53.0 |

Source: SEC companyfacts cache [F1].

The negative return on equity approximates -34%, a reflection of substantial cumulative net losses without offsetting revenue streams typical at this stage [F1].

Upcoming Phase 3 Trial Milestones and Regulatory Pathway

Olema’s near-term catalyst horizon centers on two pivotal trials investigating palazestrant’s efficacy and safety profile across different lines of metastatic disease management:

OPERA-01 Monotherapy Trial: Initiated November 2023, this Phase 3 study probes second/third-line treatment settings for ER+/HER2- metastatic breast cancer patients resistant or intolerant to prior therapies.

Key timelines include anticipated top-line data release slated for fall of 2026, NDA submission targeted within 2027, followed by potential FDA approval allowing commercial launch projected by late 2027 [S1][N1].

OPERA-02 Combination Trial: Evaluating front-line efficacy of palazestrant co-administered with Novartis-supplied ribociclib; enrollment began in 2025 through collaboration agreement support.

Anticipated top-line results expected by end-2028 with subsequent regulatory submission aiming for approvals potentially enabling market introduction around 2029 [S1][N1].

While these milestones encapsulate transformative opportunity windows, regulatory uncertainties inherent in trial outcomes and FDA review timelines underscore continual risk factors intrinsic to clinical-stage biopharma investment prudence [S1][S2].

Financial Health: Navigating Clinical Stage Costs with Strong Liquidity

Despite operational scale-up costing upward of $146 million annually via R&D and administrative outlays, Olema sustains a fortified liquidity position supported by over $48 million cash and equivalents alongside total current assets approximating $515 million as of December 31, 2025 — yielding an exceptionally strong current ratio near tenfold coverage over short-term liabilities (current liabilities: approximately $51.8 million) [F1].

The absence of product revenue amplifies reliance on equity financing and credit facilities historically tapped to preserve developmental momentum [S17]. Free cash flow remains deeply negative given operating cash outflows vastly exceeding negligible capex commitments (~$159 thousand), consistent with maintenance of an asset-light operational model focused chiefly on clinical progression rather than infrastructural expansion at this juncture [F1].

Capital Allocation Strategy and Shareholder Return Potential

Aligning with biotech norms devoid of commercial returns during extended development cycles, Olema directs capital predominantly into R&D endeavors supporting pivotal trials’ execution and expansion pipelines including early OP-3136 activities. Neither dividends nor share buybacks feature in corporate policy aligning fungible resources towards value-generative endpoints subject to regulatory success [F1].

Liquidity strengthening through public offerings or debt amendments facilitates fiscal runway extending targeted milestones achievement without curtailment risks.[F1][S17]

ROE remains negative given transition phase but hinges fundamentally on approval successes that could pivot earnings profile positively post-commercialization.

Commercial Preparations: Infrastructure or Licensing Debates Ahead

Olema faces strategic decisions whether to construct dedicated salesforce capabilities or pursue licensing/partnering strategies for U.S./global commercialization if regulatory approvals materialize after pivotal readouts [S1]. The Novartis collaboration provides both therapeutic synergies and insight into partnership frameworks facilitating market access, evidenced by Novartis’ ribociclib supply commitment underpinning OPERA-02 trial.

Such alliances alleviate upfront commercial infrastructure costs but may dilute future revenues—yet direct sales might present operational complexities beyond the company’s current scope given its historical outsourcing model to vendors/manufacturers.

Thus, "build versus buy" commercialization options encapsulate standard tradeoffs balancing control against capital efficiency within biopharma go-to-market strategic paradigms.

Industry Competitive Dynamics and Partnership Leverage

The competitive terrain Olema navigates includes entrenched pharmaceutical incumbents marketing approved ER+/HER2- agents spanning SERDs, aromatase inhibitors alongside dominant CDK4/6 inhibitors like palbociclib and abemaciclib.

Olema’s CERAN/SERD unique profile distinguishes it mechanistically offering potential advantages handling resistant disease forms inadequately served by existing therapies.

Partnerships such as the collaboration with Novartis mitigate resource gaps inherent for smaller players ('wallflower-risk') by combining complementary assets—drug supply chains plus clinical expertise—while deploying innovation vectors focused on receptor degradation nuances.

However, formidable challenges persist regarding trial recruitment competition, payer acceptance dynamics amidst evolving oncology standards of care, and eventual physician adoption hurdles characteristic of crowded therapeutic categories [S1][N1].

Cybersecurity and Regulatory Risk Oversight in Biopharma Context

Beyond scientific development risks, Olema dedicates considerable governance focus towards cybersecurity resilience—a growing concern amid sensitive patient data handling across global registries.

Oversight lies primarily within the Audit Committee framework supplemented by leadership roles held by experienced IT executives interfacing directly with Chief Legal Officer and CFO functions ensuring budgetary controls combined with policy enforcement consistent with evolving regulations like GDPR for European data privacy compliance [S1][S4][S8].

Robust incident response protocols mandate escalation workflows involving multidisciplinary teams spanning legal, regulatory affairs, communications alongside IT resources minimizing operational disruption risks tied to cyber breaches or patient data confidentiality lapses.

Such integrative security investments underscore increasing recognition that information security is essential alongside scientific rigour within modern biopharma operational risk frameworks.

This report synthesizes publicly available data from SEC filings up through March 19, 2026 ([S#], [F1]) along with relevant recent news articles ([N#]). Discussion focuses exclusively on verified facts without speculative projections or investment advice related assessments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments