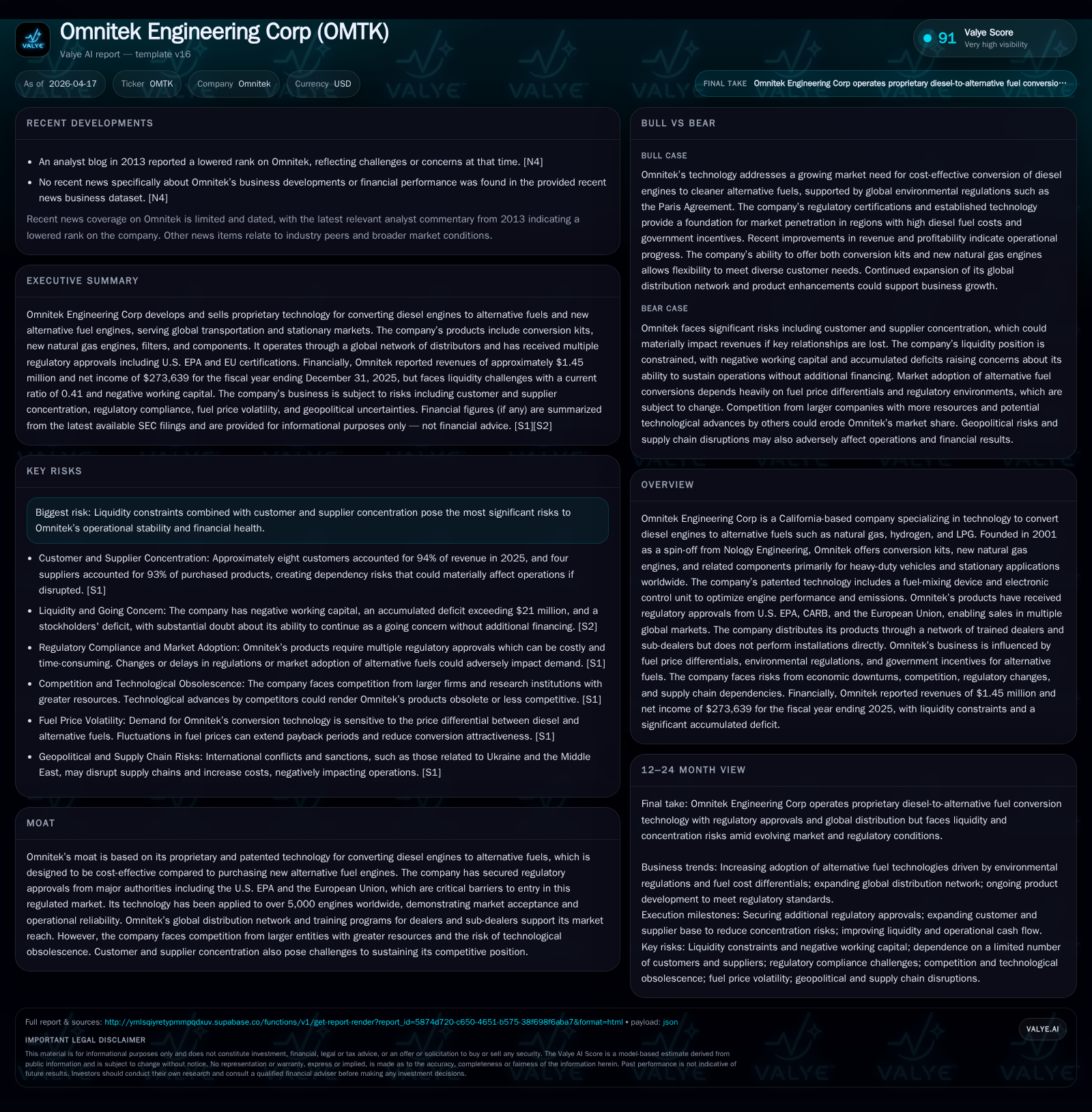

Omnitek Engineering’s Rebound: Growth, Risks, and Capital Challenges

Omnitek Engineering Corp shows a 2025 earnings turnaround alongside persistent liquidity and concentration risks.

Omnitek Engineering Corp achieved notable top-line growth of 42.2% in 2025 with a transition to net profitability, reversing several years of losses. Despite improving operating income and net income figures, the company continues to grapple with significant negative operating cash flow and negative equity, reflecting ongoing capital constraints. Revenue sustainability hinges on fuel price differentials, regulatory approvals, and market acceptance amid concentrated customer and supplier bases. Monitoring liquidity and diversification efforts will be essential for supporting future expansion in alternative fuel engine conversions.

Turning Point: Omnitek’s Financial Revival in 2025

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1449950 | 273639 | -244348 | -85891 | +42.2% | +263.7% |

| 2024 | 1019726 | -167137 | 30077 | -148500 | -3.4% | +22.4% |

| 2023 | 1055314 | -215406 | 17211 | -196140 | -1.4% | -9.5% |

| 2022 | 1070787 | -196709 | 9239 | -174420 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -25.6 |

| 2024 | 12.4 |

| 2023 | 18.2 |

| 2022 | 19.9 |

Source: SEC companyfacts cache [F1].

Omnitek Engineering Corp's financial statements reveal a meaningful shift in fiscal year 2025 from prior years characterized by operating losses and net deficits. The company reported revenue climbing to $1.45 million (up 42.2% YoY from $1.02 million in 2024) [F1], driven by expanded product adoption and favorable market conditions outlined below. Operating loss shrank substantially by about 42%, falling from -$148,500 in FY2024 to -$85,891 in FY2025 [F1]. Notably, net income transitioned sharply from losses spanning the previous three years (-$196k in 2022 through -$215k in 2023) into positive territory: $273,639 for FY2025 [F1].

However, this improved profitability masks lingering liquidity concerns. Cash flow from operations remained negative at approximately -$244,000 despite net profits [F1], which signals ongoing challenges managing working capital effectively. This gap may impair Omnitek's ability to fund operations internally without external financing or partnerships.

Drivers Behind Historical Growth and Market Acceptance

Omnitek’s proprietary technology converts legacy diesel engines for operation on alternative fuels including compressed natural gas (CNG), liquefied natural gas (LNG), renewable natural gas (RNG), hydrogen (H₂), and liquefied petroleum gas (LPG). The company's patented fuel-mixing device coupled with its electronic control unit optimizes combustion efficiency and emissions profiles for heavy-duty vehicles and stationary engines worldwide [S1].

The recent surge stems partly from fleet operators opting for overhaul-conversions—leveraging engine service lifecycles that can extend up to two decades—rather than purchasing costly new natural gas engines. This economic choice is especially appealing when diesel fuel prices remain elevated relative to gaseous alternatives, lowering payback periods on conversions.

Regulatory certifications from the U.S. EPA, California Air Resources Board (CARB), and European Union provide critical market access barriers that reinforce Omnitek’s competitive moat [S3]. These approvals allow deployment across multiple regulated jurisdictions mitigating legal risks associated with engine emissions standards.

Omnitek distributes via a network of trained dealers who perform installations independently—streamlining scalability but necessitating control over dealer training quality to maintain performance consistency.

Navigating Concentrated Customer and Supplier Dependencies

Concentration risk poses a pronounced threat: eight customers accounted for roughly 94% of revenues in 2025, amplifying vulnerability to customer loss or demand reduction [S3]. Similarly, supplier concentration is intense with four suppliers providing upwards of 93% of purchased components.

This profile exposes Omnitek to disruptions either in purchasing arrangements or contractual relationships with these key partners. Given the specialized technology and customized components required—often involving single-source or limited-supplier parts—any supply chain hiccup could delay production schedules or increase costs adversely affecting margins.

Maintaining diversified supply lines or securing long-term agreements will be crucial mitigants in an industry where component quality directly influences engine conversion reliability.

Liquidity Tightness and Its Impact on Operational Stability

Financial metrics underscore severe liquidity constraints that cloud Omnitek’s operational resilience despite profit gains.

At December 31, 2025, current liabilities ($1.62 million) considerably outweighed current assets ($664k), yielding a current ratio near 0.41—a level signaling difficulty meeting short-term obligations without raising additional funds or generating immediate cash flows [F1].

Operating cash flow remained negative (-$244k) indicating that profits recorded were not yet converting into positive net liquidity from core business operations [F1]. This persistent cash burn intensifies dependence on external financing sources such as equity raises or strategic partnerships noted previously [S4][S6].

Absent improvement in working capital management or materially higher sales volumes generating positive cash flow, Omnitek risks straining vendor relationships or missing growth opportunities due to funding shortfalls.

Revenue Sustainability and Potential Market Constraints

The attractiveness of Omnitek’s offerings largely depends on favorable fuel economics; specifically the differential between diesel prices versus lower-cost natural gas fuels primes demand through shortened payback periods.

Latest disclosures highlight narrowing fuel price spreads which elongate conversion cost recovery periods, potentially undercutting customer willingness for retrofits [S1]. Geopolitical tensions stemming from conflicts like Ukraine-Russia and Israel-Gaza contribute uncertainty regarding supply chains for key petroleum derivatives impacting raw materials costs [S1].

Furthermore, evolving environmental policies under frameworks such as the Paris Agreement drive regulatory complexity that demands continual product innovation and certification expenditures—which may constrain margins or delay product rollouts particularly if emission standards tighten abruptly in major markets [S7][S10].

Competitive pressures also arise as larger OEMs develop their own alternative-fuel engine technologies which benefit from scale advantages not accessible to Omnitek currently.

Capital Allocation Priorities amid Negative Equity

Despite gaining profitability in FY2025 with net income near $274k, Omnitek's balance sheet reflects ongoing structural challenges including an accumulated deficit resulting in stockholders’ equity remaining negative at about -$1.07 million as of year-end 2025 [F1].

Capital expenditures have remained low historically—approximately $1,445 in FY2022—and stable R&D investment around $52k–53k annually signals a disciplined spend focus primarily sustaining core technology development rather than aggressive expansion initiatives [F1][S5][S14][S22].

The company has not paid dividends nor engaged in share buybacks given lack of distributable equity; capital allocation thus prioritizes maintaining operational continuity and incremental innovation over shareholder returns at this stage.

Strategic capital discipline remains vital amid tight liquidity conditions.

Future Growth Prospects Under Environmental and Regulatory Trends

Market tailwinds include expanding regulatory mandates worldwide aimed at reducing carbon emissions from transportation sectors compelling fleet operators toward cleaner fuel conversions inspected under rigorous EPA/CARB/EU testing protocols endorsed by Omnitek’s certifications [S3].

Technological evolution toward incorporating hydrogen as an alternative fuel represents an opportunity avenue for diversification though scale barriers limit near-term penetration given hydrogen fueling infrastructure constraints compared with more established natural gas options.

Growth is thus likely paced by gradual retrofit cycles within heavy-duty fleets responsive to tightening emission standards aligned with global climate policies — a structural but steady market dynamic requiring continued regulatory compliance agility by Omnitek.

Investor Watchpoints: Key Metrics and Upcoming Milestones

Direct forward guidance remains sparse; therefore investors should monitor quarterly organic revenue trends juxtaposed against refining gross margins as indicators of product mix shifts or pricing power.

Tracking improvements in operating cash flow metrics will serve as bellwethers for alleviating working capital stress critical before sustainable profit reinvestment could occur.

Efforts aimed at reducing customer concentration risk or broadening supplier networks would be key qualitative developments enhancing operational stability prospects discussed herein [S3].

Additionally, resolution details related to legal proceedings settled late 2025 suggest limited lingering litigation exposure but warrant watching for any knock-on reputational effects influencing partner confidence [S1].

Lastly, macroeconomic factors such as energy price volatility and geopolitical developments retain potential impact on demand forecasts underscoring external risks beyond internal controls.

This report is prepared solely for informational purposes based on currently available data from company filings and public records as of April 17, 2026. It does not constitute investment advice nor a recommendation to buy or sell securities. Users should independently verify facts before making decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments