OSR Holdings Advances 4PL Medical Device Strategy Amid Tight Liquidity and Patent Asset Base

Latest quarter reveals strategic investments in medical distribution and immunotherapy platforms alongside financial constraints.

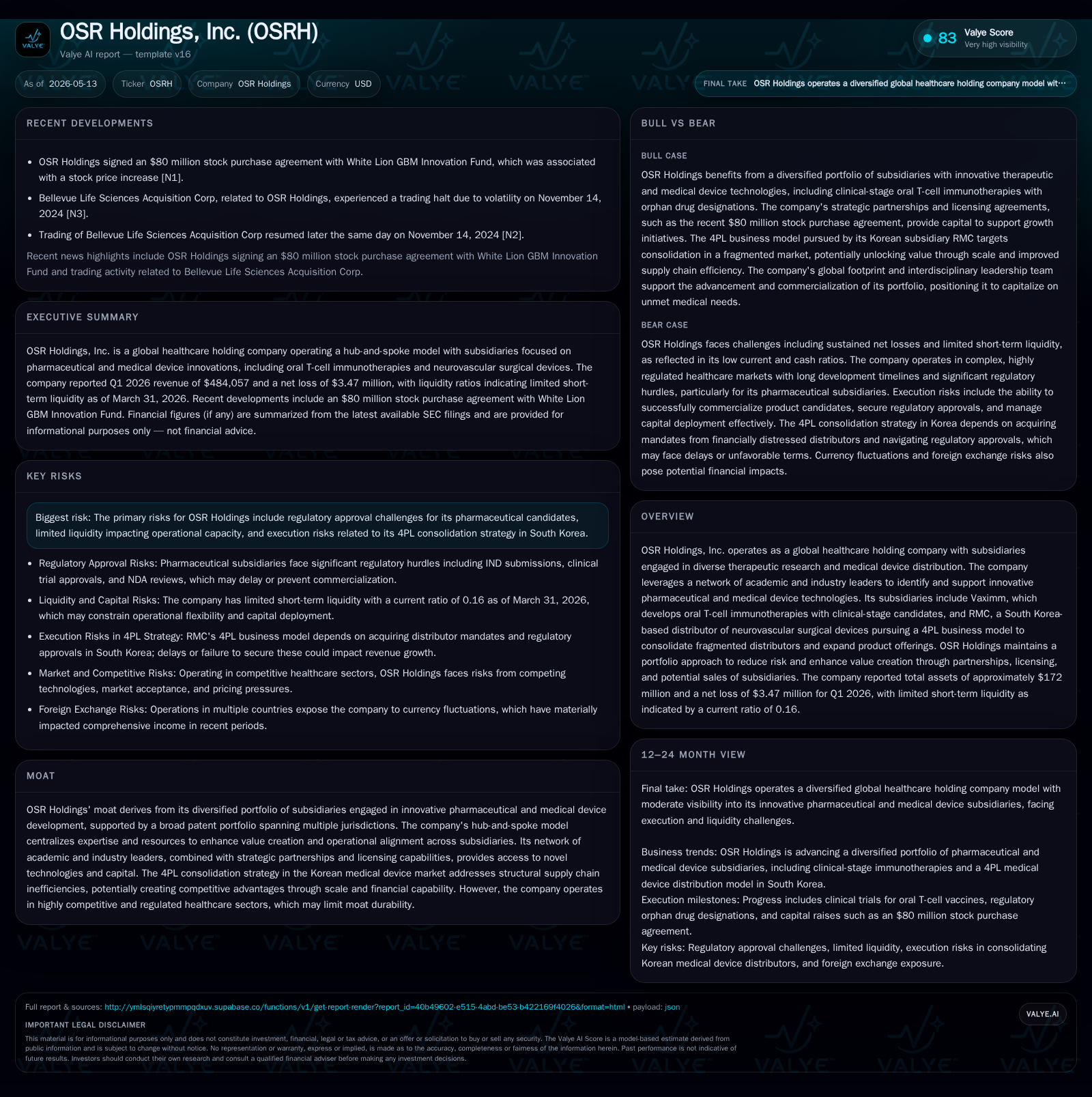

In Q1 2026, OSR Holdings continued its complex transformation as a global healthcare holding company by advancing its subsidiaries focused on oral T-cell immunotherapies and South Korean medical device distribution. The quarter highlighted impairment charges related to its nascent IT subsidiary, consolidation activities, and ongoing negotiations affecting supplier contracts for its core RMC subsidiary. The 4PL (fourth-party logistics) rollout remains a pivotal growth driver expected to commence revenue generation in 2027. However, the company faces liquidity pressures with a current ratio of 0.16 and ongoing operating losses, underscoring the financial challenges inherent in executing its multi-subsidiary portfolio approach within highly regulated and capital-intensive healthcare sectors.

Recent Operating Update

The latest quarterly report filed on May 13, 2026 [S2] sheds light on several critical operational developments impacting OSR Holdings. A significant immediate change was the incorporation of Taction Co., Ltd., a technology-focused entity aimed at software development and IT consulting. Due to absence of clear near-term commercialization plans, OSR recognized an impairment charge equal to Taction’s acquisition cost, signaling prudence in managing non-core assets.

Financially, the company reported total assets of roughly $172 million, sustained chiefly by intangible assets including a substantial patent technology portfolio valued at about $139 million net [S2]. Current liabilities at $17.9 million dwarf current assets of approximately $2.9 million resulting in a precariously low current ratio of 0.16, highlighting ongoing short-term liquidity constraints [F1].

Furthermore, milestone payment commitments from BCME amounting to up to $815 million anchored around the progression of Vaximm AG’s oral T-cell immunotherapy programs were reaffirmed [S3]. This underpins the strategic value OSR places on pharmaceutical innovation within its subsidiary ecosystem.

On the distribution front, the South Korea-based RMC subsidiary is actively shifting towards a fourth-party logistics (4PL) model designed to consolidate fragmented neurovascular surgical device distributors [S1]. Revenue from this initiative is not yet realized but projected to launch in 2027 after receiving requisite mandates and MFDS regulatory clearances. Management anticipates rapid expansion, forecasting revenues growing from KRW 4.1 billion in 2026 to KRW 44.8 billion by 2030 (approximate annualized growth rate near 82%), with stabilizing net margins near 8% by 2028 [S1]. Executing this complex rollout depends critically on capital allocation, regulatory timelines, FX considerations due to USD debt obligations, and successful pipeline conversion of distributor mandates [S6].

An operational headwind stemmed from renegotiations with Penumbra Inc., whose prior distribution agreement expired mid-2024 without renewal resulting in RMC ceasing purchases of key products but continuing limited existing inventory sales pending resolution [S1]. This affected sales volume mix and gross margin dynamics.

Business Model Overview

OSR Holdings operates as a global healthcare holding company leveraging a hub-and-spoke model where centralized executives align subsidiary strategies while facilitating partnership and capital access [S1]. Revenue generation stems mainly from subsidiaries focusing on two verticals: innovative therapeutics (notably Vaximm’s cancer immunotherapy development) and medical device distribution (chiefly RMC’s neurovascular devices). Additionally, OSR acquired Woori IO in January 2026—a biosensing company developing non-invasive glucose monitoring technologies—to diversify its medtech portfolio further [S15].

Revenue mechanics vary significantly across subsidiaries:

- Pharmaceutical/licensing sector: Income primarily involves milestone payments from collaborators like BCME upon meeting clinical or commercial milestones plus potential royalties structured via license agreements [S3]. Direct product sales revenue is not currently recognized given early-stage clinical pipelines.

- Medical device distribution: RMC traditionally operated purchase-resale agreements which have evolved into commission-based consignment contracts lowering reported net sales but stabilizing margins due to reduced inventory risk [S16]. Its pivot toward a consolidated 4PL model aims to capture broader control over supply chain fragmentation typical in Korea’s medtech importer landscape.

Margins remain suppressed reflecting heavy investment phases: research & development expenditures are expected to ramp significantly through subsidiaries active in clinical trials starting late 2026 while SG&A costs expanded substantially post-business combination due to professional services necessary for public reporting compliance [S23].

Switching costs create moderate customer stickiness especially within distributions given mandate ownership constraints but overall competition remains intense both at pharmaceutical innovation fronts and within fragmented regional medtech markets.

Industry Structure and Competitive Position

OSR operates within two intersecting but distinct markets:

Biopharmaceutical therapeutic development, specifically next-generation immunotherapies targeting cancer and degenerative diseases through subsidiaries like Vaximm. This domain features high barriers including extensive regulatory approvals, long clinical development cycles, and substantial capital requirements but offers high value if successful.

Medical device distribution in South Korea focused on neurovascular surgical devices via RMC. The market here is characterized by high fragmentation among distributors causing inefficiencies — OSR aims for competitive advantage via its emerging 4PL model that consolidates mandates financially backed by OSR’s capital strength relative to smaller players.

While OSR's strategy leverages diversified subsidiaries reducing concentration risk, the overall moat is moderate given evolving product pipelines with uncertain commercial outcomes and regulatory hurdles common to healthcare sectors globally. The company’s patent portfolio provides defensibility primarily on IP fronts within pharmaceuticals but less so within distribution where scale and regulatory licenses matter more.

Growth Drivers

- 4PL Model Rollout at RMC: Central driver projecting accelerated revenue growth starting FY2027 contingent on acquiring distributor mandates, obtaining Korean MFDS approvals, effectively managing working capital amid structural hospital payment delays, and navigating foreign exchange impacts due to USD-denominated obligations [S1], [S6].

- Pharmaceutical Milestones: BCME’s contractual milestone payments up to $815 million linked to clinical/regulatory advancements offer episodic upside dependent on successful trials predominantly with Vaximm’s immunotherapy candidates [S3].

- New Technology Platforms: Integration of Woori IO’s non-invasive biosensing technologies introduces potential expansion into chronic disease monitoring markets enhanced further through collaboration with Samsung Electronics signaling strategic synergies under evaluation [S15].

- Intellectual Property Leverage: Extensive patent portfolio supporting innovative therapies can spur licensing deals or eventual asset monetization providing additional capital formation paths.

Risks / Watchpoints / Growth Constraints

- Regulatory Approval Uncertainty: Pharmaceutical candidates face inherent risks related to securing timely FDA/MFDS approvals which could delay or derail milestone-triggered payments.

- Liquidity Constraints: With a current ratio of only about 0.16 and current liabilities surpassing current assets by a wide margin ($17.9M vs $2.9M), OSR must carefully balance capital deployment for growth initiatives against operational cash needs and dilution risks associated with ongoing equity raises [F1], [S2].

- Execution Complexity: Scaling the Korean 4PL network demands swift mandate acquisitions under acceptable commercial terms; failure here would stall projected revenue jumps.

- Supplier Negotiation Outcomes: Loss or renegotiation failures such as those encountered with Penumbra impact product mix stability hence gross profits adversely.

- Currency Exposure: Depreciation of KRW against USD elevates cost structures given USD-denominated borrowings which could pressure margins further during platform scale-up phase.

- Legal Disputes: The company faces pending lawsuits regarding brokerage fees adding litigation risk which may impose additional costs or distractions.[S12]

What To Watch Next

Market participants should focus on several upcoming milestones:

- Progress updates on RMC’s acquisition of new distributor mandates and receipt of MFDS import licenses enabling full operation of the planned 4PL model.

- Clinical trial advancement news or milestone triggers related to Vaximm's oral T-cell immunotherapy candidates that could unlock significant contractual payments from BCME.

- Capital raising activity details especially concerning ELOC utilization pace or new equity facilities introduced post Q1 filings aimed at extending liquidity runway with minimized dilution impact [S21], [S22].

- Resolution developments surrounding Penumbra contract negotiations or other supplier relationships influencing RMC inventory management.

- Operational progress integrating Woori IO into OSR’s medtech portfolio including any strategic collaborations announced particularly involving Samsung Electronics partnership.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1566701 | |

| 2026-03-31 | ||

| Total debt | $469810 | |

| 2026-03-31 | ||

| Net debt | $-1096891 | |

| 2026-03-31 | ||

| Current assets | $3mm | |

| 2026-03-31 | ||

| Current liabilities | $18mm | |

| 2026-03-31 | ||

| Current ratio | 0.16x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, OSR Holdings' financial snapshot presents an asset-heavy position ($172 million total assets) largely concentrated in intangible assets such as patents ($139 million net) alongside goodwill ($29.7 million) mostly stemming from recent acquisitions [F1],[S13]. Current liabilities stand at nearly $18 million dwarfed against current assets just under $3 million yielding a low current ratio around 0.16 indicating tight short-term liquidity conditions that require careful cash flow management [F1]. Total reported debt approximates half a million dollars while cash balances hover near $1.57 million leaving net debt negative though overall working capital remains strained [F1],[S2].

Operating losses are substantial ($18.3 million annually ending December 2025) reflecting early commercialization phases across subsidiaries compounded by elevated selling & administrative costs linked partly to transition into public company status post business combination completed February 2025 [F1],[S23]. Research & Development expenses are accruing steadily with plans for significant ramp in late 2026 aiming at advancing therapeutic candidates through clinical stages [S23]. Financing activities have shifted away from convertible notes fully repaid earlier in 2026 toward controlled utilization of an equity line of credit facility complemented by loans from affiliates aimed at balancing dilution against capital needs [S11], [S17], [S21].

The data highlights capital intensity characteristics typical of diversified healthcare holdings with long investment horizons.

This analysis is based exclusively on publicly filed SEC documents through May 13, 2026 ([S1]-[S29]) and companyfacts data ([F1]). It does not constitute investment advice or recommendations but aims to provide an informed perspective on OSR Holdings’ operational trajectory within its industry context considering recent developments disclosed by management.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments