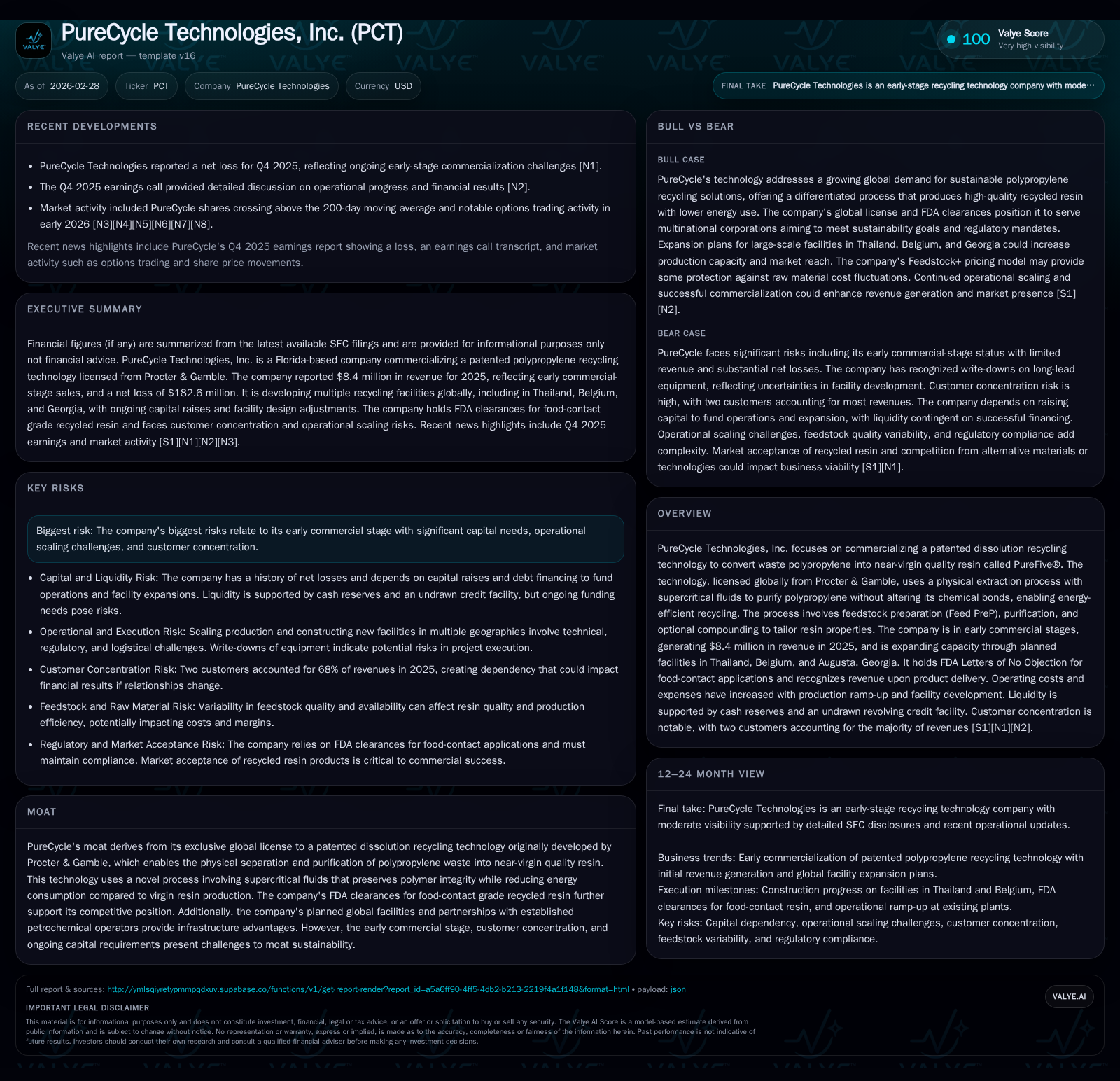

PureCycle Technologies Advances Commercial Scale-Up Amid Significant Operating Losses and Expansion Plans

A detailed review of PureCycle's financial trajectory and operational progress as it transitions from development to commercial production of recycled polypropylene resin.

PureCycle Technologies reported $8.36 million in revenue for 2025 as it progresses its proprietary polypropylene recycling technology toward industrial scale with planned expansions in Thailand, Belgium, and Augusta, Georgia. The company incurred a net loss of $182.6 million in 2025 driven by scaling costs and ongoing investments. Capital raises including a $300 million Series B preferred stock issuance and convertible notes underpin growth funding. Liquidity remains supported by $157 million cash on hand and an undrawn $200 million credit facility extended through 2027. Key risks include high capital intensity, operational scale-up challenges, sustained negative cash flows, and customer concentration. Upcoming milestones include new facility commissioning and potential redemption of Series A Preferred Stock contingent on warrant exercise.

Transitioning from Development to Early Commercial Sales

PureCycle Technologies is commercializing a proprietary polypropylene recycling technology licensed exclusively from Procter & Gamble that uses a dissolution process with supercritical fluids to produce near-virgin quality resin branded as PureFive®. This approach preserves polymer integrity while reducing energy consumption relative to conventional resin manufacturing [F1][S11].

In fiscal year 2025, PureCycle generated revenue of $8.355 million reflecting early commercial sales primarily linked to product shipments from its operational Ironton facility [F1]. Revenue recognition occurs upon transfer of control consistent with contractual terms [S11]. While nascent, this revenue marks a key milestone transitioning the company from pilot to commercial operations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -183 | -143 | 41 | +36.9% |

| 2024 | -289 | -145 | 56 | -184.3% |

| 2023 | -102 | -95 | 154 | -20.0% |

| 2022 | -85 | -65 | 287 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 5 | -184 | -397.9 |

| 2024 | 2 | -200 | -160.2 |

| 2023 | 1 | -249 | -24.2 |

| 2022 | 2 | -353 | -16.6 |

Source: SEC companyfacts cache [F1].

Revenue reflects early-stage sales as operations scale; net losses have deepened due to increased operating costs; capex declined year-over-year following peak investment phases [F1].

Operating Expenses Reflect Scale-Up Investment

Operating expenses rose notably as the company invested in staffing, utilities, repairs, maintenance, depreciation, feedstock procurement, and corporate overhead aligned with plant startups and R&D initiatives [S11][N2]. Research efforts focus on feedstock preparation enhancements and analytical capabilities to support scalable purification processes.

Selling, general & administrative expenses increased with professional fees related to new facility development across Thailand, Belgium, and Augusta sites as well as executive compensation including equity-based awards [S11]. These cost dynamics are typical for companies transitioning from pilot to commercial stages.

Net operating losses of approximately $182.6 million for FY2025 emphasize the current negative leverage driven by fixed costs absorption without yet achieving sufficient throughput or positive margins [F1].

Strategic Capacity Expansion Across Three Facilities

Expansion plans center on three primary manufacturing hubs: Thailand and Belgium facilities targeting regional markets plus a significant upgrade at Augusta to increase purification capacity [S1][N2]. The integrated manufacturing flow includes Feed PreP units for sorting feedstock impurities followed by proprietary purification using supercritical fluids.

Each site presents engineering challenges typical of scaling novel physical extraction technologies where solvent management, energy efficiency relative to virgin resin benchmarks, and product consistency are critical [N2]. Operational learnings from Ironton inform design improvements incorporated into subsequent builds.

Capital Structure Supports Growth Initiatives

To finance expansion and operations, PureCycle completed several significant capital raises:

- A $300 million Series B Convertible Perpetual Preferred Stock issuance closed mid-2025 provides substantial growth capital [S7][S16].

- Earlier Series A Preferred Stock issuance raised approximately $21.8 million [S6].

- Total gross long-term debt stands at approximately $363 million including $250 million Green Convertible Senior Notes issued in August 2023 and related-party bonds totaling roughly $150 million [S4][S7][F1].

- The company maintains a $200 million revolving credit facility extended through September 30, 2027 which was undrawn as of December 31, 2025 [S4][S14].

At year-end 2025 cash and cash equivalents were approximately $157 million with restricted cash around $11 million providing liquidity buffers [F1][S9]. No dividends have been paid as earnings are retained for reinvestment; limited share repurchases occurred totaling around $4.9 million in fiscal 2025 [F1][S24].

Financial Metrics Highlight Continued Investment Phase

Despite revenue growth signs, profitability remains out of reach with net losses widening though improving sequentially versus prior year [F1]. Operating cash flow deficits persisted at approximately $142.7 million reflecting ongoing deployment into scaling infrastructure.

Capital expenditures declined by about one-quarter year-over-year to roughly $40.8 million indicating movement beyond peak investment periods while maintaining maintenance spending [F1]. Free cash flow remains significantly negative.

Equity decreased sharply from about $180 million at end-2024 to roughly $45.9 million at end-2025 due largely to accumulated losses diminishing book value [F1]. Resulting approximate return on equity is deeply negative at nearly -398%, consistent with early-stage industrial biotech companies investing heavily ahead of commercial profitability.

Market Positioning Supported by Licensing Moat and FDA Approvals

PureCycle holds exclusive global licensing rights for the patented polypropylene dissolution recycling technology developed by Procter & Gamble that leverages physical extraction via supercritical fluids rather than chemical bond alteration—yielding energy efficiencies over virgin resin manufacture [N2][S1].

The company's PureFive® recycled resin has received FDA Letters of No Objection enabling food-contact applications which differentiates the product within recycled plastics markets expanding potential downstream use cases beyond industrial commodities into consumer-packaged goods sectors [N2][S1].

Customer concentration risk persists given initial sales contracts remain limited; however strategic facility locations aim to broaden market access aligned with feedstock availability and customer networks.

Risks Amid Growth Execution Challenges

Key risks include:

- High capital requirements with continued financing needs until achieving scale economies capable of reversing losses [S12][N1];

- Technical complexities inherent in scaling supercritical fluid dissolution processes across multiple sites while maintaining quality consistency;

- Regulatory compliance demands in emerging recycled food-contact resin markets requiring ongoing FDA engagement;

- Dependence on a limited customer base constraining revenue diversification;

- Persistent negative cash flow generating liquidity pressures despite available credit facilities currently undrawn [S12][N1].

These factors typify challenges faced by industrial biotechnology ventures pioneering circular economy solutions in plastics recycling.

Outlook: Milestones and Potential Financial Triggers in Focus

Investors should monitor:

- Commissioning timelines for Thailand and Belgium plants alongside capacity upgrades at Augusta;

- Volume ramp metrics signaling operational throughput improvements enabling better margin profiles;

- Progress on capital raising or refinancing particularly tied to potential redemption of Series A Preferred Stock contingent on warrant exercises expected by March deadlines [N2][S3];

- Quarterly financial results indicating revenue growth inflection points alongside narrowing operating losses;

- Enhancements in feedstock sourcing quality supporting purification efficiency;

- Strategic partnerships or integration deals broadening technology adoption across packaging or automotive sectors requiring specialty polypropylene grades.

While explicit numeric guidance remains undisclosed recently by management, these indicators will serve as key signals validating PureCycle’s execution progress through its early commercialization phase.

This analysis is based on publicly available filings and news releases without investment recommendations or price forecasts. Readers should consider these data points within broader due diligence frameworks relevant to industrial biotechnology growth-stage companies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments