Public Storage’s Dominance in Self-Storage Faces Evolving Market and Operational Challenges

Public Storage maintains industry leadership, yet rising economic pressures, competitive forces, and international ventures shape a complex outlook.

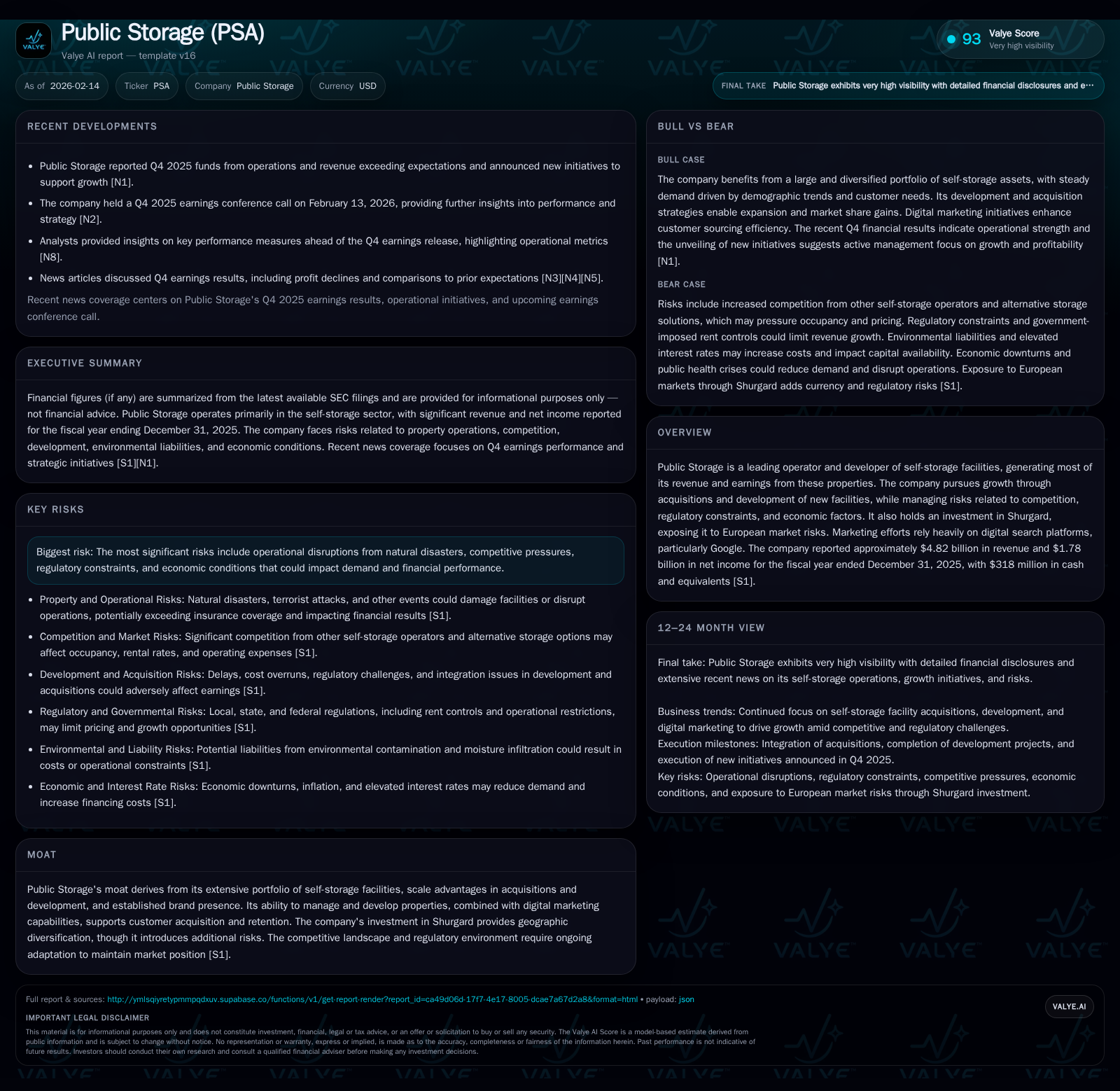

Public Storage, the largest self-storage operator with a strategic portfolio valued in billions, delivered a Q4 2025 earnings beat despite contracting profits. The company’s growth remains anchored in acquisitions, new developments, and its European stake via Shurgard, which introduces fresh risk dimensions. Competitive pressures, regulatory shifts—especially tax increases in key states—and operational vulnerabilities to natural disasters present mounting challenges. Meanwhile, PSA leans on digital marketing engines like Google to fuel customer acquisition amid a dynamic sector landscape.

A Colossus in Self-Storage: Public Storage’s Core Business and Scale

Public Storage stands as an unmistakable titan within the self-storage industry. Managing a vast portfolio of properties across key U.S. markets—with additional European exposure through Shurgard—the company generated approximately $4.82 billion in revenue for the fiscal year ending December 31, 2025, alongside a net income of $1.78 billion [F1], underscoring its deep operational footprint. This scale is not incidental; it confers significant advantages in acquiring high-quality assets at favorable prices and developing new facilities efficiently.

The company’s brand recognition acts as an intangible asset that bolsters customer trust and repeat business—a critical factor in what might otherwise be regarded as a commoditized real estate segment. As documented in its 10-K filing (S1), Public Storage’s core business centers on owning and operating these self-storage facilities where rental fees and ancillary services constitute steady income streams. While economic cycles influence demand elasticity to some extent, the overall resilience of the model has anchored the firm’s moat.

Distinctively, the firm's moat is augmented by integration of digital marketing strategies that enhance consumer reach (to be elaborated later), combined with scale-driven efficiency gains that smaller operators find challenging to replicate. Despite recent macro headwinds such as supply chain disruptions or inflationary pressures that impact construction costs and operating expenses [S1], PSA continues leveraging its established name to maintain top-line momentum.

Insight: Public Storage’s dominant footprint is both its strength and a strategic lever shaping how it confronts evolving market realities—scale affords leverage but also necessitates sophisticated risk management.

Decoding Q4 2025: Earnings Beat but Rising Profit Pressures

In February 2026, PSA reported fourth-quarter earnings that surpassed consensus estimates for both funds from operations (FFO) and revenue [N1][N4]. This topline outperformance illustrated continued underlying demand for storage space even amid rising inflationary burdens. However, closer scrutiny reveals nuanced trends beneath the headline beat:

- Operating margins faced compression linked to increased maintenance costs, utility expenses, property taxes (notably regional variances), and wage inflation [N3][N8].

- Net income declined compared with prior quarters despite higher revenues, signaling cost structure stress points challenging profitability sustainability.

- Competitive pressures necessitated promotional pricing tactics in certain urban centers to retain occupancy rates amid growing alternatives.

These dynamics encapsulate the classic tension experienced by large REITs amid current economic cycles: balancing growth ambitions with margin integrity as input costs climb and competitors react aggressively [N8]. Importantly, management highlighted proactive initiatives aimed at operational efficiencies and selective capital deployment plans for future quarters designed to temper these impacts without stalling expansion [N1].

Insight: The Q4 results function as a reality check—Financial beats affirm business durability while tightened profits foreshadow intensified margin management battles ahead.

Growth Engines: Acquisitions, Development, and International Investments

Public Storage propels its growth chiefly through three avenues: acquisitions of existing self-storage assets or companies domestically; ground-up development projects; and strategic investments abroad via stakes like that in Shurgard—a European-focused facility operator representing geographic diversification but also increased external exposure [S1][N1].

Segmenting these growth pillars reveals important considerations:

- Acquisitions: PSA faces stiff competition from private equity funds and real estate investors alike in identifying accretive properties or operating companies. Pricing pressure risks eroding anticipated returns post-acquisition if due diligence misses latent liabilities or if local governments revise property tax assessments upward following transactions [S1].

- Development: New facility projects carry inherent execution risks including delays caused by permitting processes or labor/material cost surges. Nevertheless, moderate pipeline activity underscores measured confidence in select markets with strong demand-growth fundamentals.

- International Investment: The Shurgard stake exposes PSA to different regulatory frameworks and macroeconomic variables distinct from U.S. conditions—introducing currency fluctuation risks and political uncertainties alongside diversification benefits.

Management’s disclosures emphasize vigilance around integration challenges post-acquisition (e.g., environmental remediation needs or tenant turnover issues) along with cautious project scalability reflective of evolving market feedback loops [S1]. Further growth efforts communicated during Q4 earnings highlight iterative capital allocation judgments balancing expansion with risk mitigation [N1].

Insight: Growth ambitions remain intact but are tempered by heightened scrutiny over cost escalations and complexity amplifications deriving from cross-border exposures.

The Moat Under Pressure: Competitive Landscape and Regulatory Hurdles

While Public Storage benefits from formidable scale advantages and brand cachet, these attributes do not render it immune to intensifying competitive threats or shifting regulatory sands. As noted in regulatory filings (S1) alongside analyst commentaries (N6)[N7], several factors are converging:

- Competition Intensifies: New entrants deploying innovative service models or aggressive pricing challenge PSA’s traditional base. Regional operators often tout localized expertise while emerging tech-enabled platforms are reshaping convenience metrics.

- Regulatory Pressures: Governmental bodies increasingly scrutinize zoning laws related to self-storage development; moreover, property tax regimes have grown more onerous especially in high concentration states like California where valuation reassessments can materially increase expense lines [S1].

- Operational Constraints: Environmental mandates regarding construction materials or energy usage impose potential delays or cost burdens affecting development economics.

Against this backdrop, sustaining differentiation demands agility across operational tactics—from leasing innovation to community engagement—as well as disciplined capital expenditure governance.

Insight: The moat remains intact but requires continual fortification through adaptive strategies addressing both competitive innovations and heightened regulatory vigilance.

Weathering the Storm: Operational Risks from Natural Disasters and Economic Factors

Public Storage confronts tangible risks tied to physical asset vulnerability alongside broader economic fluctuations. Detailed disclosures (S1) list exposures including:

- Natural Disasters: Earthquakes, fires, hurricanes pose material threats potentially exceeding third-party insurance caps given partial self-insurance structures; tenant claims linked to property loss amplify risk profiles.

- Cost Inflation: Escalating repair/maintenance expenses driven by labor shortages or commodity price surges increase operating leverage downside.

- Taxation Risks: Property tax hikes pending reassessment methodologies threaten profit margins particularly within concentrated regions such as California.

- Demand Sensitivity: Macroeconomic stressors influencing disposable incomes could reduce short-term self-storage utilization rates despite longer-term secular growth trends.

The confluence of these factors suggests an operational environment requiring robust contingency planning alongside prudent financial buffers.

Insight: Despite scale-based resilience advantages, operational risk exposures demand ongoing vigilance lest episodic shocks erode returns disproportionately.

Digital Marketing and Customer Acquisition: The New Frontier

Diverging from typical real estate REIT peers reliant predominantly on location advantage alone, PSA actively leverages digital channels—primarily Google search platforms—to attract tenants directly [S1]. This reflects an evolving marketing paradigm amidst consumer behavior shifts toward online research before physical visits.

Harnessing targeted pay-per-click advertising campaigns paired with optimized landing pages enhances lead conversion rates while enabling granular measurement of marketing ROI relative to traditional offline methodologies. Moreover, effective digital presence contributes significantly toward brand reinforcement particularly among younger demographics exhibiting greater internet reliance.

However, this strategy carries inherent risks including platform algorithm changes impacting traffic quality or escalating bidding costs driven by industry-wide competition for ad space.

Insight: PSA’s distinctive embrace of digital marketing underpins customer acquisition advantage but necessitates ongoing adaptation amid changing technology landscapes.

Balance Sheet Snapshot: Cash Flow Strengths and Liquidity

Financially, Public Storage exhibits solid liquidity fundamentals heading into 2026—holding approximately $318 million cash & equivalents at fiscal year-end coupled with stable cash flow generation streams matching its sizable operational scale ($4.82B revenue FY 2025) [F1][S1]. This liquidity provides managerial flexibility to navigate cyclical volatility while sustaining investment capacity.

Notably absent are major debt maturities due imminently that could pressure refinancing risk profiles. Capital allocation strategies will likely balance dividend commitments against opportunistic acquisitions or development ventures consonant with market conditions.

Insight: The firm’s capital structure underpins operational resilience though vigilant credit management remains integral amid shifting macroeconomic currents.

Valuation Debates: Where Does PSA Fit in Defensive Portfolios?

Amid volatile equity markets early in 2026 marked by broader economic uncertainties—including potential rate hike repercussions—discussion around Public Storage frequently centers on its defensive stock attributes versus valuation concerns.[N9][N10][N12–N14]

Dividend reliability positions PSA favorably among income-focused investors seeking steadier yield streams amidst turbulence; however share price softening beneath critical technical levels (such as the 200-day moving average) signals caution.[N10]

Comparative analyses weighing PSA against other real estate securities highlight divergent investor priorities between pure value plays versus dividend longevity narratives.[N9][N13] Notwithstanding near-term margin pressures discussed earlier,[N8] many market participants treat Public Storage as a resilient bastion within diversified defensive allocations given fundamental demand stability underlying self-storage usage patterns.[N12]

Insight: PSA’s portfolio mix straddles current income appeal tempered by valuation-driven headwinds—investors face decisions balancing safety against growth impact risks.

Investor Takeaways: Navigating Opportunity amid Uncertainty

Bringing these threads together yields a nuanced portrait of Public Storage entering 2026:

The company stands distinguished by unparalleled scale within self-storage operations marked by steady revenue generation ($4.82B annually) supported through diligent acquisitions plus internal development pipelines[ S1,F1 ]. Yet recent quarterly earnings reflect emerging cost escalations compressing profits despite top-line beats[N1,N3,N8], while expansion efforts internationally via Shurgard introduce layered uncertainty[S1,N1]. Competitive pressure intensifies among nimble regional players complemented by growing regulatory scrutiny notably property taxes[S1,N6,N7]. Natural disaster exposure compounds operating risks notwithstanding adequate insurance coverage[S1]. Simultaneously, PSA’s concerted commitment to digital marketing creates differentiated customer engagement avenues driving tenant acquisition[S1], aligned with strong liquidity buffers positioning it well against economic fluctuations[F1,S1]. Market observers remain divided between championing its consistent dividends against valuation softness evident since late 2025[N9–N14].

In short: Public Storage exemplifies resilient market leadership challenged by contemporaneous economic realities requiring active mitigation strategies grounded in operational discipline and strategic foresight.

Disclaimer: This analysis is for informational purposes only. It does not constitute investment advice or recommendations regarding Public Storage securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments