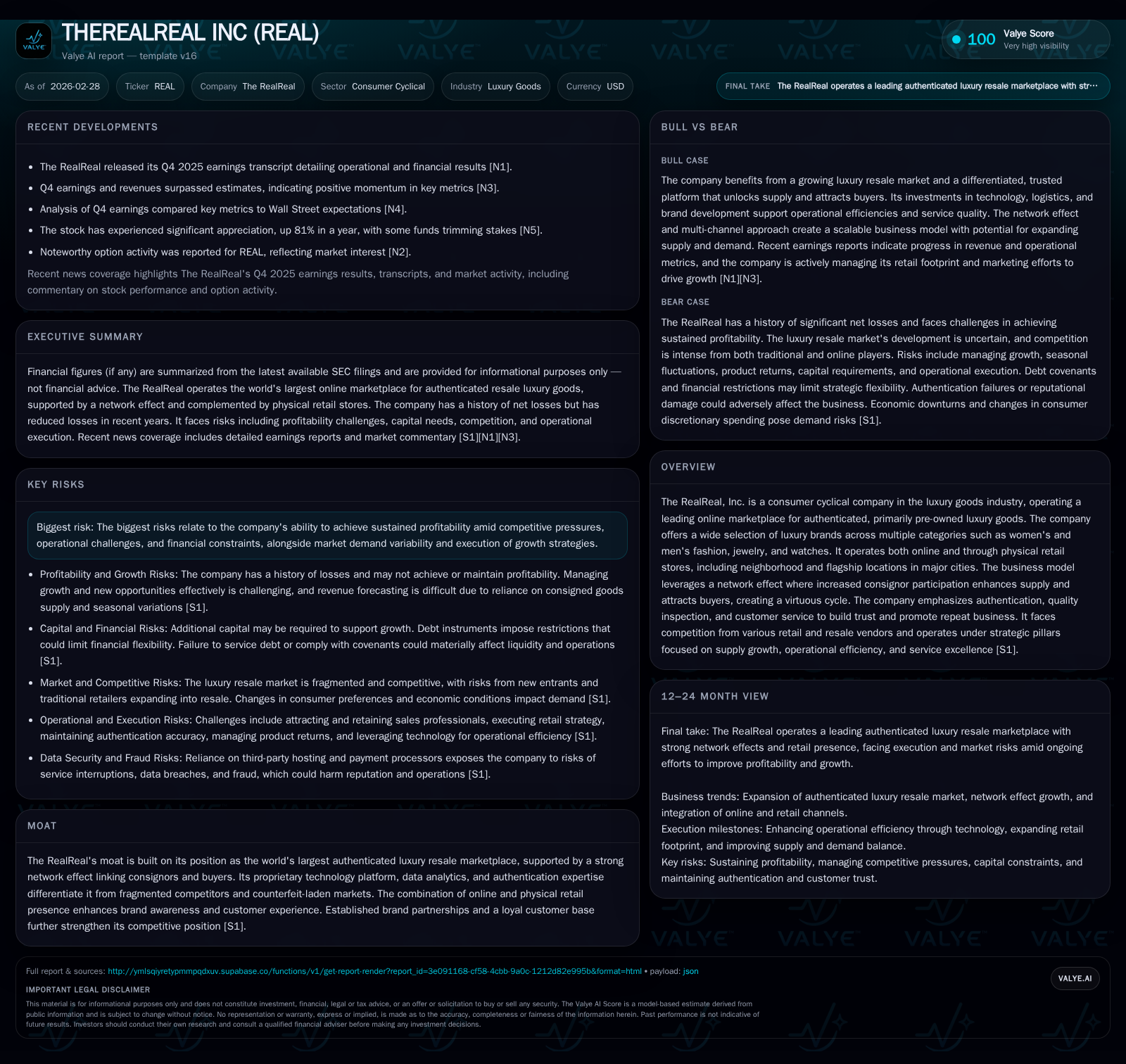

The RealReal’s Strategic Pivot: From Shrinking Losses to Growth Acceleration

The RealReal is reshaping its financial path by expanding supply, improving operational efficiency, and leveraging its unique network effect in luxury resale.

Over the past few years, The RealReal has markedly reduced its operating losses and improved cash flow generation despite ongoing net losses, signaling a strategic shift. This transformation is driven by unlocking consignor supply through proprietary technology and retail expansion, alongside operational efficiencies that enhance margin profiles. The company's distinctive flywheel marketplace model ties buyers and consignors closely, boosting sales velocity and marketplace liquidity. Capital allocation remains cautious given negative equity and liquidity pressures, with no dividends or buybacks currently. Key risks include profitability sustainability amid competitive market dynamics and execution challenges, while future growth hinges on continued supply growth and operational leverage.

Historical Financial Trajectory: Turning Around Deep Operating Losses

The RealReal's financial evolution over recent fiscal years illustrates a concerted effort to curtail substantial operating losses while advancing towards positive operational cash flows. Between FY2022 and FY2025, operating income improved significantly from a loss of -$189.2 million to -$23.9 million by the end of FY2025 — reflecting a notable 57.6% improvement year-on-year from FY2024 to FY2025 [F1]. Net losses followed a similar trend but remained material at -$41.8 million for FY2025.

Critically, operating cash flow (CFO), which lagged into deep negative territory at -$91.6 million in FY2022 and -$61.3 million in FY2023, turned positive by FY2024 ($26.8 million) before surging further to $37.0 million in FY2025 [F1]. This CFO rebound indicates improving operational discipline alongside growing marketplace liquidity. The firm's ability to convert operating income reductions into meaningful cash flow gains underpins its narrative of shifting from loss-heavy phases towards sustainable operations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -42 | 37 | -24 | 19 | +68.9% |

| 2024 | -134 | 27 | -56 | 14 | +20.3% |

| 2023 | -168 | -61 | -166 | 29 | +14.2% |

| 2022 | -196 | -92 | -189 | 23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 18 | 10.1 |

| 2024 | 13 | 32.9 |

| 2023 | -90 | 55.5 |

| 2022 | -114 | 115.5 |

Source: SEC companyfacts cache [F1].

Table: The RealReal Annual Financial Summary (FY2022-FY2025) [F1]

The capital expenditure profile shows a recent rise in investment funding technological infrastructure expansion supporting operational scalability — up approximately 31% year-over-year in FY2025 to $18.6 million [F1].

Unlocking New Supply: The Engine of Expanding Market Reach

Central to The RealReal’s rebound story is the effective unlocking of consignor supply — a cornerstone strategic pillar that expands marketplace assortment depth and breadth across luxury segments such as women’s fashion through watches [S1]. This is enabled by a proprietary technology platform that streamlines consignment logistics and pricing optimizations based on rich transactional data.

Physical retail presence complements the digital model with neighborhood stores ranging roughly between 1,800 to 3,500 square feet that provide curated selections reflective of the online inventory mix [S1]. These stores facilitate first-hand consignment experiences for sellers while flagship locations in San Francisco, Los Angeles, and New York offer large-format assortments with strong foot traffic exposure — critical for engaging higher-value consignors.

This multi-channel approach not only attracts first-time consignors who might traditionally vend through brick-and-mortar third-party channels but also accelerates repeat consignment activity through trust-building authentication processes [S1]. Flagship brand partnerships further deepen category offerings with top designers including Cartier and Hermès that boast strong resale value.

Nurturing this supply side creates an expanding virtuous cycle where more quality products attract additional buyers who may themselves become consignors — reinforcing marketplace liquidity through dense network effects uncommon in standard luxury resale models [S1][N1].

Operational Efficiency Gains Fueling Margin Improvements

Complementing supply-side growth are initiatives aimed at enhancing operational efficiency via automation technologies and proprietary data analytics that improve fulfillment workflows and reduce friction at authentication centers [S1][N2]. Through these efforts The RealReal has narrowed its negative margin footprint even as it scales operations.

Among these initiatives is "Athena," an artificial intelligence system deployed for initial authenticity assessments and product characteristic identification that helps accelerate throughput while maintaining stringent quality standards [S1][S20]. Such technological progress reduces manual costs associated with inspection without compromising buyer trust.

Financially this manifests as improving operating income — narrowing losses from nearly $56.5 million in FY2024 to $23.9 million in FY2025 — alongside rising CFOs supporting positive free cash flow (~$18.4 million = CFO minus capex) despite increased capital investments [F1][N2]. This dynamic suggests growing operating leverage enabled by technology-driven cost controls while tackling complex inventory management challenges intrinsic to single-SKU luxury products.[F1]

Strategic Pillars Driving Marketplace Network Effects

The RealReal’s business strategy coheres around three interlinked pillars: unlocking supply through an iterative growth playbook; driving operational efficiencies via tech enablement; and obsessing over buyer-consignor service excellence that fuels loyalty [S1].

These elements work synergistically to reinforce liquidity—the metric measuring how quickly luxury items sell—and underpin growing commission income streams for consignors combined with repeat purchaser activity driving GMV expansion.

A key differentiator lies in the duality where a substantive share of users act both as consignors supplying inventory and buyers consuming it [S1]. This interconnected membership base elevates sales velocity beyond simple two-sided marketplaces seen elsewhere.

Such flywheel economics foster competitive barriers difficult for fragmented peer marketplaces or counterfeit-prone platforms to replicate fundamentally strengthening The RealReal's moat [S1][S21].

Capital Allocation, Cash Flow Trends, and Return-on-Equity Analysis

Despite significant improvements in cash generation capacity evident from CFO trends reaching $37 million in FY2025 [F1], The RealReal contends with balance sheet challenges including deeply negative equity near -$415.5 million at fiscal year-end 2025 signaling cumulative retained earnings deficits following prior losses [F1].

Liquidity metrics reveal working capital pressure: current assets total approximately $227 million against current liabilities around $264 million resulting in a current ratio of roughly 0.86 below the benchmark threshold often interpreted as terminal stress for short-term coverage [F1][S8][S22].

While The RealReal does not currently pay dividends or repurchase shares—likely constrained by both capital preservation needs and restrictive covenants linked with outstanding debt tranches totaling several hundreds of millions across notes maturing between 2028–2031 [S8]—an approximate return on equity calculation using net income over equity points toward a modestly positive figure near +10%, representing nascent profitability shifts but requiring cautious interpretation due to negative book equity base distortion characteristics [F1].

Collectively these metrics underscore ongoing capital allocation discipline; reinvestments primarily target capacity expansion rather than shareholder distributions amid evolving pathway out of historic deficit positions.

Risks in Balancing Growth Ambitions with Profitability Pressures

Identified risk vectors pivot around the steep challenge of sustaining profitable scale against sizeable competitive forces including entrenched new luxury retail channels offering fresh goods at controlled discounts affecting resale price perceptions; proliferation of resale niche players fragmenting seller attention; rising authentication enforcement costs; volatile discretionary consumer behavior influenced by macroeconomic cycles; plus intensified regulatory scrutiny over data privacy impacting marketing efficiency [S1][S4][S21].

Operationally securing optimal geographic real estate for authentication centers remains nontrivial amid labor market tightness threatening fulfillment capacity expansion timelines; shipping dependencies add vulnerability to cost inflations or disruptions harming customer satisfaction metrics critical for network effect maintenance [S1][S20].

Furthermore legal uncertainties manifest notably in ongoing trademark litigation (e.g., Chanel lawsuit), potential adverse intellectual property rulings could impose costly restrictions or compel practice alterations undermining brand referencing crucial to marketplace identity [S7][S12][S19]

Server security vulnerabilities pose persistent threat vectors risking operational continuity or consumer trust erosion should cyber incidents transpire given platform data centrality [S18]. Lastly social media communication risks coupled with evolving ESG disclosures introduce reputational volatility dimensions impacting stakeholder perception tangentially affecting market positioning [S16]

Looking Ahead: Key Metrics and Catalysts to Monitor

Absent explicit company guidance on future quarters ([N1],[N2],[S1]), prudent monitoring entails scrutiny on key KPIs aligned with strategic pillars:

- Consignor volume growth rates signaling success in supply unlocking,

- Improvements in sales velocity indicating network density gains,

- Operating leverage evidenced by continuing margin recoveries,

- Cash flow resilience balancing increased capex deployments versus free cash flow sustainability,

- Authentication accuracy rates mitigating fraud risk,

- Retail store performance contributing incremental high-value consignment transaction flows,

- Customer retention ratios encapsulating service obsession effectiveness. Tracking these signals promises insight into whether The RealReal's pivot translates into durable profitability amidst luxury resale sector nuances.

Disclaimer: This analysis synthesizes disclosed financials and company-reported strategies without providing investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments