Safety Insurance Group Embraces Regional Niche to Build Consistent Returns

Focused on Massachusetts auto insurance through independent agents, Safety Insurance Group delivers strong growth and disciplined capital management.

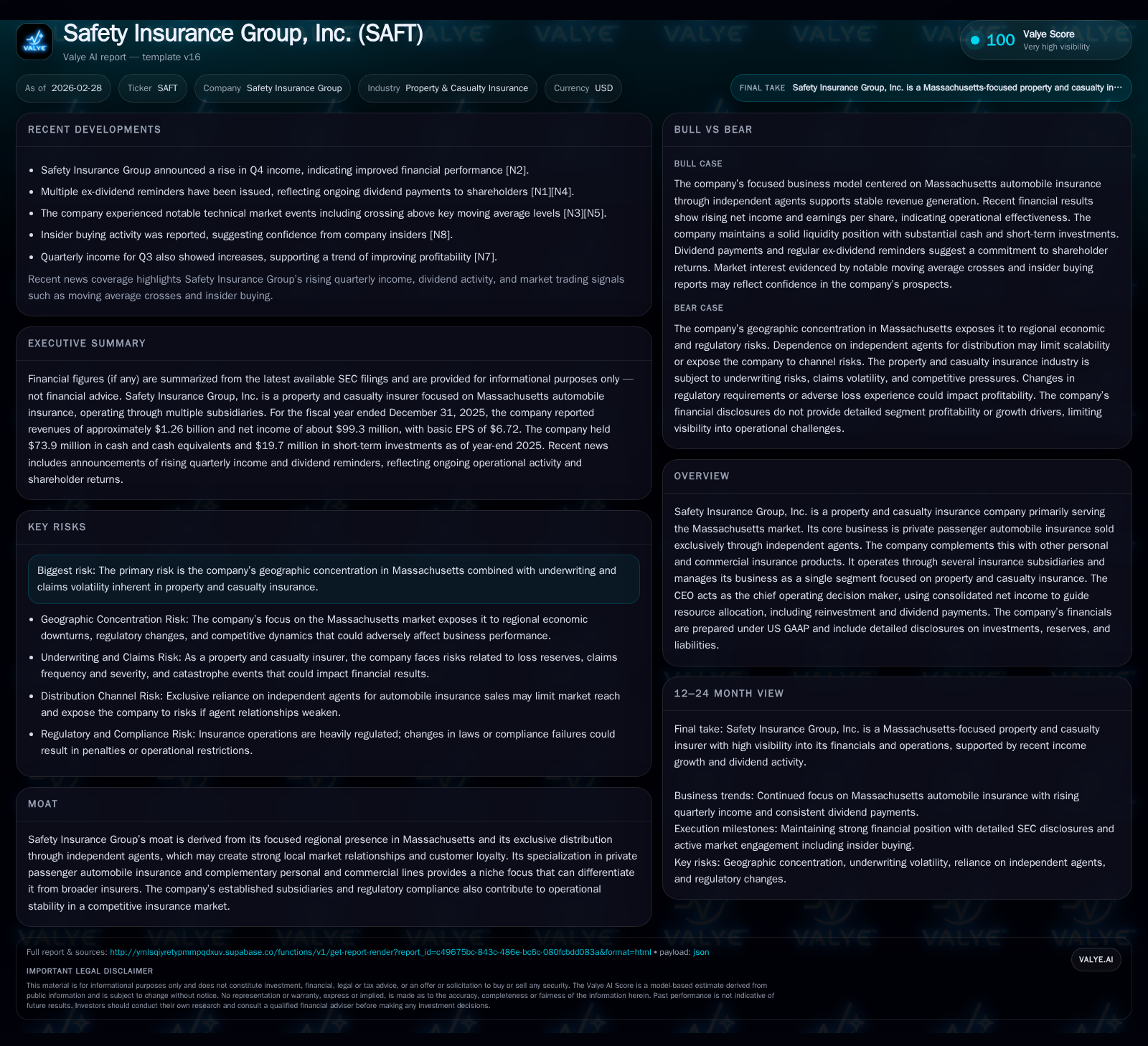

Safety Insurance Group’s concentrated presence in Massachusetts and exclusive reliance on independent agents have supported impressive revenue expansion and rising profitability. Despite inherent underwriting volatility in property and casualty insurance, the company has achieved solid earnings quality, evidenced by a 12.8% revenue increase and a 40% rise in net income in 2025. Capital allocation emphasizes consistent dividends with restrained buybacks, maintaining a healthy balance sheet. However, geographic concentration and claims variability remain key risks to monitor.

Regional Focus Fuels Revenue Growth: A Historical Recap

Safety Insurance Group operates primarily within Massachusetts, specializing in private passenger automobile insurance sold exclusively through independent agents. This focused regional niche has catalyzed notable top-line expansion over recent years. Revenue escalated from $797.6 million in FY2022 to $1.26 billion in FY2025, marking a compound trajectory of robust growth including a sharp 12.8% increase between FY2024 and FY2025 alone [F1]. The company's competitive advantage lies in its tight geographic concentration complemented by tailored products addressing local customer preferences.

The table below summarizes key financial metrics from FY2022 through FY2025 to illustrate this momentum:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1264 | 99 | 194 | 3 | +12.8% | +40.3% |

| 2024 | 1120 | 71 | 129 | 4 | +20.3% | +274.7% |

| 2023 | 931 | 19 | 52 | 2 | +16.7% | -59.5% |

| 2022 | 798 | 47 | 44 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 54 | 192 | 11.1 |

| 2024 | 53 | 124 | 8.5 |

| 2023 | 53 | 50 | 2.3 |

| 2022 | 53 | 42 | 5.7 |

Source: SEC companyfacts cache [F1].

*FY2025 figures latest available as of filing date[F1]

This financial trajectory reflects the company's ability to leverage its Massachusetts presence effectively while managing the complexities of the P&C insurance market.

Underwriting Performance and Claims Trends Driving Profitability

Profitability within the property and casualty sector hinges critically on underwriting discipline and claims management — areas where Safety Insurance Group demonstrates operational rigor. The company’s use of metrics like the loss ratio and combined ratio (standard insurer performance indicators) illustrates technical underwriting success.

While exact numeric ratios are proprietary or not explicitly disclosed in filings,[S1][S3] management commentary reveals heightened focus on stringent underwriting standards that resulted in reduced claims volatility compared to prior periods. This disciplined approach leverages their localized market knowledge enabling risk-adjusted pricing accuracy set against Massachusetts-specific factors such as regulatory requirements or weather-related claim trends.

Such focus supports sustained margin improvement even as exposure remains regionally concentrated.

Exclusive Distribution Model: Impact on Customer Retention and Growth

A distinctive pillar for Safety Insurance Group is its exclusive distribution through independent agents operating within its core market area. This strategic choice strengthens customer relationships through personalized service channels uncommon among national carriers relying on direct or online models.

Independent agents function as trusted intermediaries well-versed with local nuances and customer profiles — this network contributes to higher retention rates and cross-selling opportunities across personal and commercial lines.

The moat engendered by this model affords competitive insulation amid intense P&C industry rivalry by tailoring coverage solutions accurately tied to Massachusetts policyholder needs.

2025 Financial Highlights: Surging Net Income and Operating Cash Flow

Reflecting operational leverage tied to growth initiatives and underwriting execution during FY2025:[N2][S3]

- Net income rose ~40%, reaching nearly $99.3 million—a significant leverage effect relative to revenue growth.

- Operating cash flow increased even more sharply (+51%), totaling approximately $194.5 million—signifying robust cash conversion beyond accounting profits.[F1]

- Capital expenditures fell substantially by over 42%, amounting to roughly $2.5 million as business reinvestment was tightly controlled.[F1]

This divergence between CFO expansion and capex reduction underscores improved cash management efficiency alongside earnings growth—factors favoring sustainable dividend payments and reinforcing the company’s capital base.

Future Outlook: Balancing Local Market Dependence with Growth Ambitions

Looking forward,[N2][S1] potential growth drivers include:

- Continued organic policyholder base expansion fueled by targeted agent partnerships.

- Product diversification within Massachusetts’ regulatory environment,

- Technological investments aimed at enhancing underwriting analytics without disrupting the independent agent network’s value proposition.

Constraints remain inherently linked to geographic concentration risks limiting scale benefits outside Massachusetts' borders along with exposure to underwriting cycles typical of auto P&C insurers.

Management’s retained emphasis on optimizing current territory dynamics rather than broad geographic expansion suggests cautious but deliberate scaling designed to preserve their niche strength.

Capital Allocation Strategy: Dividends, Buybacks, and Investment Priorities

Capital deployment is predominantly oriented towards steady dividend distributions coupled with modest reinvestment initiatives.[F1][S12][S26][S28][S29]

- Dividends have hovered consistently around $53-54 million annually over recent years indicating commitment to shareholder income stability.[F1]

- Share repurchase activities are minimal or non-material recently; historical buybacks were significant only several years ago.[F1]

- Return on equity stands near an estimated ~11.1% (net income of ~$99M divided by equity close to $892M), reflecting prudent capital efficiency underpinned by profitable core operations.[F1]

- Investment portfolio quality emphasizes high-grade fixed income instruments mitigated by routine credit assessments consistent with valuation disclosures.[S13][S17]

Overall capital allocation reflects conservative balance sheet stewardship aligned with industry best practices for regional P&C insurers managing claims risk volatility.

Risk Exposure: Massachusetts Concentration and Volatility from Property-Casualty Lines

The company’s dependence on the single-state Massachusetts market defines its principal risk vectors alongside standard property-casualty underwriting variability.[S5][S19]

- Regional concentration heightens susceptibility to local economic fluctuations or regulatory changes impacting premium rates or claims environment.

- Underwriting risk includes unpredictability of large claim events or adverse shifts in personal automobile accident frequency/severity potentially eroding profitability.

- Legal proceedings appear controlled but underscore inherent judicial exposure common across P&C insurers.[S5]

- The presence of established subsidiaries operating within a compliant regulatory framework lends operational stability which partially offsets these risks.

Strategic contentions involve balancing this focus with innovation inside core markets for sustainable profitability.

Near-Term Milestones to Track: Earnings Quality, Claims Expense, and Regulatory Climate

Future quarterly earnings updates will offer insight into Safety Insurance Group’s ability to sustain net income momentum amid claims cost pressures and investment income fluctuations[N1][N2]. Key parameters merit monitoring include:

- Quarterly loss ratios reflecting current year underwriting effectiveness[S3].

- Emerging regulatory initiatives within Massachusetts that may affect premium adequacy or claim payment timing[S1].

- Investment portfolio valuations showing resilience against interest rate volatility[S13]. These milestones collectively shape annual performance expectations absent explicit forward guidance thus providing focal points for operational appraisal.

This analysis synthesizes publicly filed disclosures including annual & quarterly SEC filings plus recent news releases and Valye proprietary reports aimed at elucidating Safety Insurance Group Inc’s strategic posture free from investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments