SilverBox Corp V: SPAC Strategy and Growth Outlook After First Quarterly Report

Analysis of SilverBox Corp V’s initial quarterly filing highlights its capital position, seasoned management, and upcoming business combination prospects.

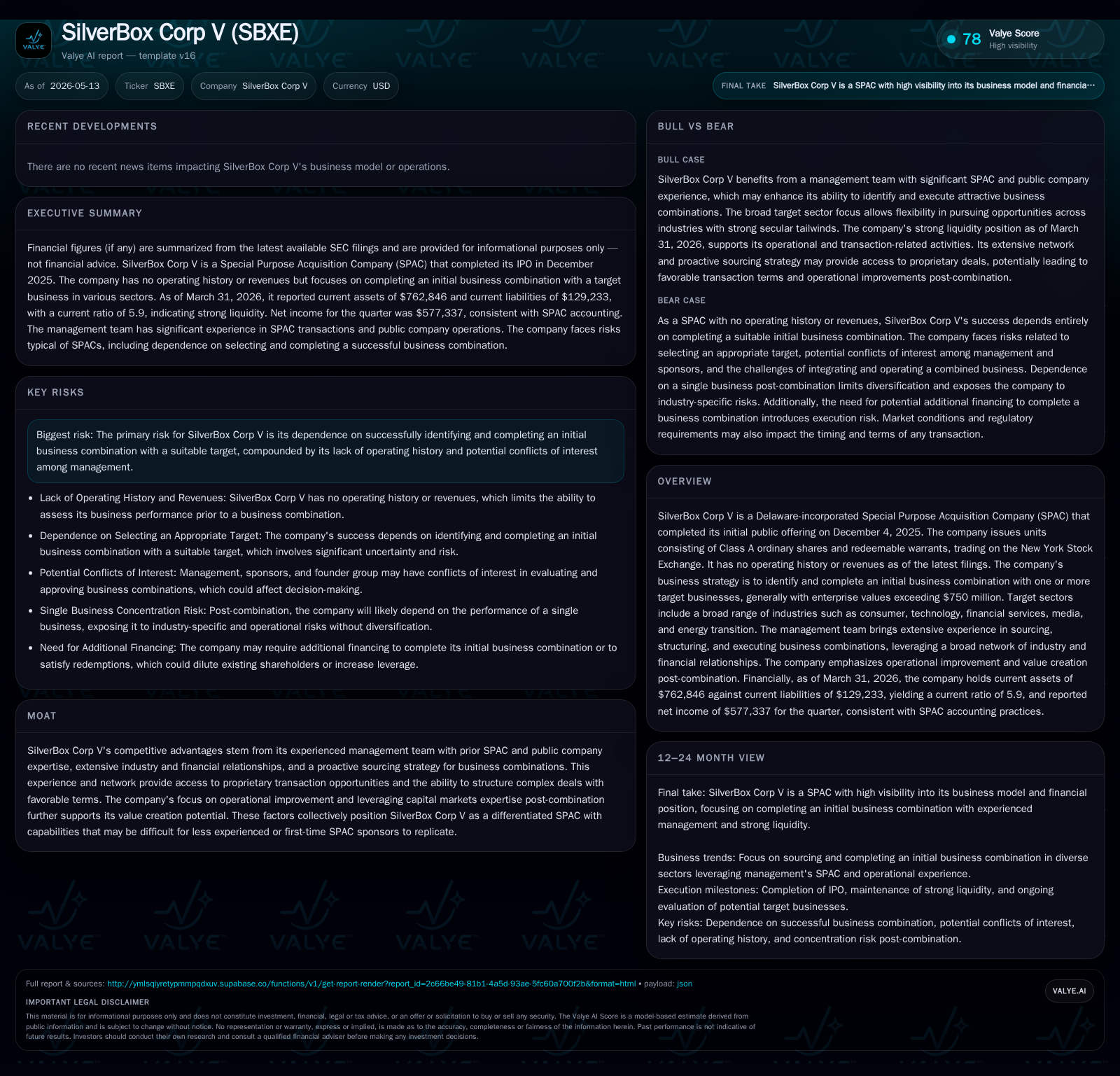

SilverBox Corp V remains a blank-check company with no operating history as of its May 2026 quarterly report, holding substantial capital in trust while pursuing an initial business combination. The company’s differentiated competitive advantage stems from an experienced multi-SPAC leadership team and broad sector focus targeting deals above $750 million enterprise value. Key growth hinges on successful deployment of capital through proprietary pipeline transactions, but execution risks include sponsor conflicts and the challenges inherent in identifying suitable targets. Upcoming milestones to monitor include transaction announcements and shareholder votes that will shape the company’s path toward value creation.

Latest Quarterly Update Clarifies Near-Term Operating Status

SilverBox Corp V’s most recent quarterly filing dated May 12, 2026 (Form 10-Q) reconfirms the company’s status as a nascent SPAC with no operating revenue or business activity aside from capital management and transaction execution preparations [S2]. There were no material changes in risk factors or litigation noted since the prior annual filing. The company reported current assets of approximately $763 thousand against current liabilities of around $129 thousand as of March 31, 2026, translating into a strong current ratio of about 5.9 — indicating solid short-term liquidity to support ongoing organizational functions ahead of a business combination [F1]. This financial position underscores that SilverBox remains a well-funded blank-check vehicle primarily holding proceeds in trust awaiting deployment into a target.

SilverBox Corp V’s SPAC Model: Capital and Deal Sourcing Architecture

SilverBox Corp V was incorporated as a Delaware SPAC that completed its IPO on December 4, 2025, raising gross proceeds of $276 million by issuing units containing one Class A ordinary share and one-third of a redeemable warrant priced at $10 per unit [S1,S16]. These warrants grant holders the option to buy additional shares at $11.50 each post-combination under adjusted terms. The primary mission is to identify and consummate an initial business combination with one or more companies having aggregate enterprise value generally exceeding $750 million [S1].

Unlike narrowly focused peers, SilverBox maintains broad sector flexibility targeting consumer goods, technology segments (including software and SaaS), financial services and fintech, media/entertainment, industrial technology/infrastructure, and energy transition sectors [S1,S12]. This thematic diversification enhances deal sourcing versatility allowing management to pursue a wider array of compelling growth industries.

Investors participate upfront by purchasing units combining equity shares and long-dated warrants that provide optionality tied to successful consummation of an acquisition. Post-combination value creation depends partly on deploying these raised funds judiciously into operationally sound targets with scalable business models.

Management Experience as a Differentiating Competitive Moat

The management team's pedigree is central to SilverBox’s market positioning. This group leads their fifth SPAC vehicle collectively after successfully navigating prior combinations involving entities such as Boxwood Merger Corp and SilverBox Engaged Merger Corp among others [S6]. Their prior public company and transaction experience equips them with rich relationships across investment bankers, private equity investors, credit fund managers, legal firms, and operating executives critical for proprietary deal sourcing [S1,S19].

This deep network affords access to exclusive acquisition opportunities often not widely marketed—a key advantage against less established or first-time sponsors lacking such connectivity. Moreover, the team emphasizes post-transaction operational improvement strategies leveraging hands-on industry knowledge alongside capital markets expertise aimed at accelerating target growth and enhancing margins after deal close [S1].

Industry Dynamics: SPAC Market Challenges and Target Opportunity Scope

The broader SPAC landscape remains intensely competitive but also cautious amid increased regulatory scrutiny from the SEC and evolving investor sentiment shifting towards quality over quantity transactional pipelines [S1]. Many new entrants face challenges sourcing attractive deals that meet both valuation discipline and shareholder approval thresholds.

SilverBox’s broad sector mandate partially buffers these pressures by enabling pursuit across multiple growth areas including sectors characterized by fragmentation ripe for consolidation such as fintech or energy transition infrastructure [S12]. Yet this diversification also demands robust evaluation capabilities given wide variance in industry dynamics.

Pricing power in post-merger entities typically hinges on selecting businesses with recurring revenue streams and defensible market positions—criteria prominently outlined by SilverBox’s investment thesis aiming for margin-accretive acquisitions capable of generating free cash flow over time [S12].

Key Growth Drivers: Transaction Pipeline and Post-Combination Value Creation

The company’s trajectory depends fundamentally on timely identification and closure of one or more initial business combinations leveraging their large trust account capital base plus potential follow-on financings arranged concurrently with deals if needed [S1,S6,S14]. Success factors include uncovering proprietary transactions where management can negotiate favorable terms aligned with shareholder interests.

Post-combination expansion plans revolve around using operational expertise to optimize strategic direction, streamline costs where feasible, scale the customer base through targeted investments, and tap public equity markets effectively if warranted [S1]. These capabilities are expected to drive sustainable value growth beyond initial deal announcements.

Execution cadence is essential; missing deadlines risks forced liquidations or prolonged shareholder uncertainty, which generally depresses ultimate returns.

Risks and Challenges in Executing Successful Business Combination

While experienced sponsors mitigate some execution risk facets, significant hurdles remain. The absence of any historical operating income or cash flow places absolute dependence on management's ability to source viable deals within the mandated timeframe (24 months from IPO) or face liquidation obligations to shareholders at trust account book value plus accrued interest [S7,S9,S22].

A notable complication is the conflict-of-interest potential stemming from overlapping sponsor roles between SilverBox Corp V and its affiliated sibling entity SilverBox Corp IV (SBXD), which is concurrently pursuing a digital asset platform merger but offers no assurance on successful closing [S6]. This overlap could impact resource allocation or bidding competitions for targets.

Further uncertainty arises from typical SPAC governance issues such as retention of key personnel post-merger, reliance on independent valuations subject to market fluctuations, and shareholder voting processes that could impede transaction completion or delay integration efforts.

Upcoming Milestones: What to Monitor Next in Deal-Making Process

Investors should closely watch for announcements signaling selection of initial target(s) within the prescribed search period following IPO—in this case roughly December 2027 unless extended via shareholder approval—as well as any updates on conflicts involving SBXD transactions which may affect competing interests [S1,S2].

Subsequent proxy statements to facilitate shareholder votes will inform redemption rights optimizations impacting capital structure post-combination. The exercise window for public warrants tied to these units also represents a liquidity event worth monitoring for market impacts.

Given management's track record elsewhere though not guaranteed here, early confirmation of firm transaction agreements would meaningfully de-risk the story.

Current Financial Position Supports Execution but Revenue Absence Remains

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $762846 | |

| 2026-03-31 | ||

| Current liabilities | $129233 | |

| 2026-03-31 | ||

| Current ratio | 5.9x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

By quarter-end March 31, 2026—five months post-IPO—SilverBox held about $763K in current assets versus just $129K in current liabilities yielding a healthy liquidity cushion reflected by a current ratio approaching 5.9 times. This snapshot emphasizes strong balance sheet health typical for pre-combination SPACs focusing exclusively on overseeing their trust accounts until deployment [F1].

No revenues or operating income have been recognized yet consistent with this stage; management expenses mostly relate to administrative costs absorbed pre-combination reflecting negative net income last reported [$ -7.69 million year-end Dec 2025] but deemed normal given blank-check status [F1].

Financial leverage is negligible so far without debt issuance indicating low refinancing risk ahead of pending operationalization once acquisitions commence.

Disclaimer: This analysis is based solely on publicly available SEC filings up to May 12, 2026. It does not constitute investment advice or an endorsement of the company's securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments