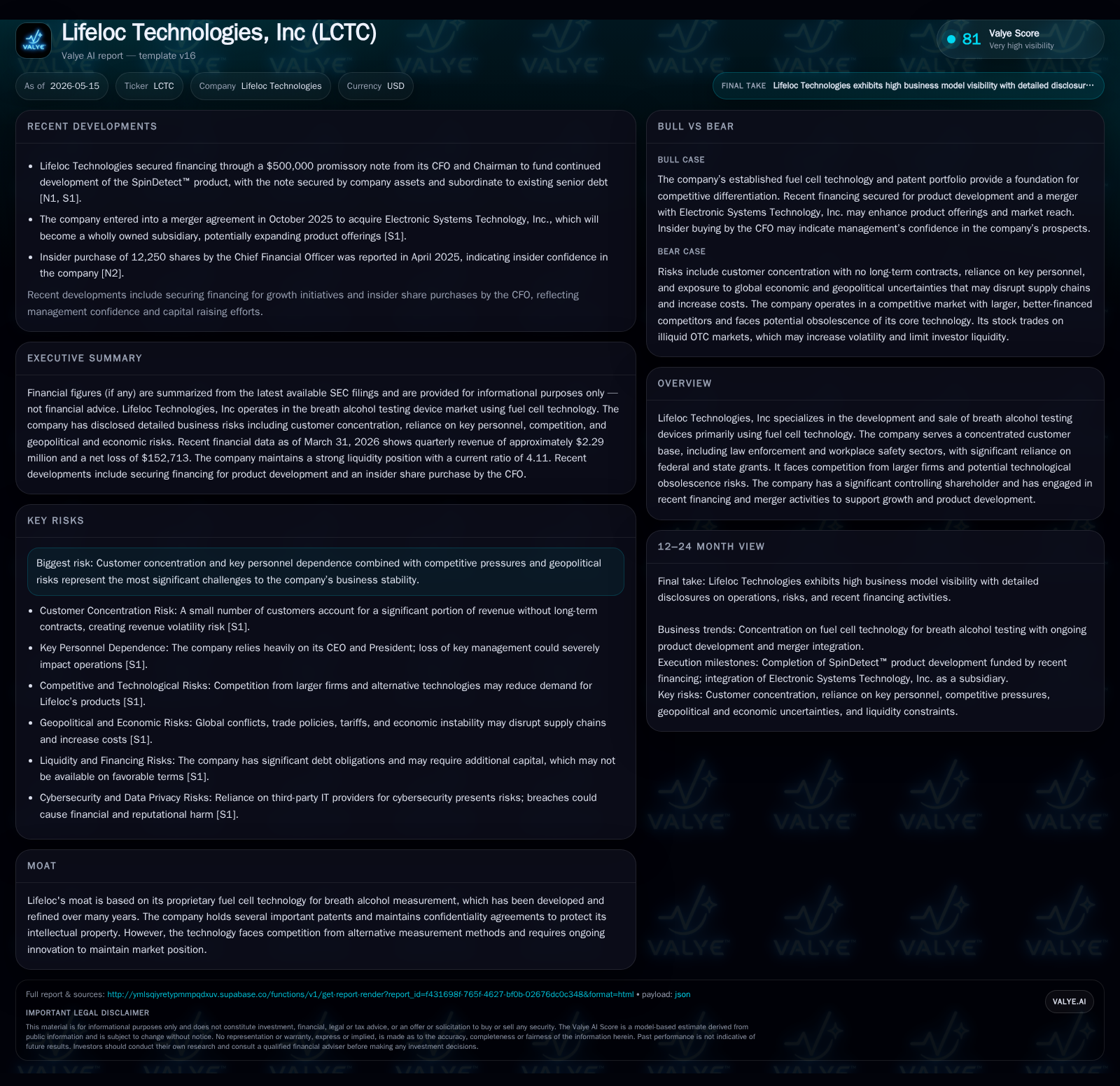

Lifeloc Technologies Advances Breath Alcohol Innovation Amid Grant Dependency and Competitive Pressure

Lifeloc Technologies secures internal financing to accelerate SpinDetect development while managing concentrated client base and competitive risks.

In its latest quarterly filing, Lifeloc Technologies announced a $500,000 promissory note from its CFO/Chairman to fund SpinDetect breath alcohol test development, underscoring a leadership-aligned innovation push amidst flat revenues. The company’s proprietary fuel cell technology remains central to its business model, targeting law enforcement and workplace safety sectors reliant heavily on government grants. Competitive pressures from alternative technologies and concentration risks persist, while recent financing supports growth ambitions. Lifeloc maintains solid liquidity to underpin these initiatives despite ongoing operating losses.

Latest Quarterly Developments: Strategic Step Towards SpinDetect Advancement

Lifeloc Technologies’ most immediate operational update comes from the May 14, 2026 10-Q filing detailing a $500,000 secured promissory note extended by CEO/CFO Vern Kornelsen to the company effective May 1, 2026 [S2][S3]. This infusion is earmarked exclusively for accelerating development of their next-generation breath alcohol testing product branded as SpinDetect™. The loan terms offer an initial interest rate of 10.5%, interest-only payments through year-end 2026, followed by equal monthly installments over five years starting January 2027; prepayment carries no penalty. Security for the note includes a deed of trust on corporate property and a security interest subordinate to existing senior debt [S3].

This financing structure reflects a significant internal capital commitment given Mr. Kornelsen's controlling shareholder position (approximately 77%) which aligns leadership incentives tightly with product innovation outcomes. It underscores Lifeloc’s approach to navigating limited external financing options while prioritizing R&D pipeline progression within the company’s constrained cash flow environment.

Core Business Model and Technological Moat in Fuel Cell Breathalyzers

Lifeloc’s core revenue derives from sales of breath alcohol analyzers based on proprietary fuel cell sensor technology, primarily sold into law enforcement agencies and workplace safety markets [S1]. The fuel cell technology is lauded for its accuracy and specificity in measuring blood-alcohol content through breath samples, supported by multiple patents protecting key elements of the design. Confidentiality agreements further guard against IP leakage.

The company leverages regulatory mandates such as the U.S. Department of Transportation's (DOT) Omnibus Transportation Employee Testing Act that obligates safety-sensitive transportation employees to undergo alcohol testing using approved devices—an important structural driver for demand [S1]. Customers typically include police departments, transportation companies in trucking and rail sectors, and industrial employers in oil & gas or other hazardous environments.

Revenue generation mechanics involve device sales with associated consumables (e.g., mouthpieces), calibration services, maintenance contracts, and software for data management. These recurring elements provide some revenue stability but are limited by overall market size and customer concentration dynamics.

Market Context: Customer Concentration and Competitive Challenges

Lifeloc operates within a niche yet competitive segment dominated by companies offering alternative breathalyzer technologies including semiconductor oxide sensors, infrared analyzers, and increasingly popular portable electronic devices driven by digital innovations [S1][S20]. While fuel cell methods maintain regulatory favor due to proven accuracy, emerging sensor technologies could erode this advantage over medium term if validation or cost structures shift favorably for competitors.

Additionally, Lifeloc’s dependence on government grants — primarily federal/state funding that underwrite equipment procurement mainly for law enforcement — creates volatility in sales volume tied closely to political budget decisions [S1]. Procurement cycles can be unpredictable; delayed or reduced allocations directly depress revenue flows.

Trade tariffs pose further pressure on input costs as components sourced domestically and abroad face price fluctuations impacting production economics. Ongoing geopolitical instability including international conflicts has raised supply chain risk, potentially affecting lead times for assembly parts or consumables [S1][S29].

Customer switching costs remain moderate; although safety certifications deter random vendor changes, customers may switch providers based on pricing competitiveness or newer technology adoption trends.

Innovation and Growth Catalysts: Product Development and Market Penetration

SpinDetect represents a critical growth vector designed to refresh Lifeloc’s product portfolio with anticipated enhancements possibly in detection speed, device size reduction, integration with digital platforms, or improved user interface — all aimed at capturing additional market share within existing clients and enticing new sectors such as private workplace drug/alcohol testing programs outside traditional transportation markets [S3][S1].

The recent $500K loan explicitly finances this development phase spotlighting management intent to maintain innovation momentum despite constrained external capital access [S2][S3]. Success here could translate into an expanded addressable market if the technology achieves recognition beyond legacy segments.

Additionally, the company pursues deeper engagement with grant programs that offer renewals or expanded scopes potentially supporting new deployments geographically or across more safety-sensitive industries. Ongoing investments in calibration service capabilities also aim at improved margins through recurring revenue streams tied to installed base expansion.

Risks and Constraints: Grant Reliance, Governance Concentration, and Regulatory Headwinds

A dominant concern resides in customer concentration stemming largely from government grant dependency. Interruptions or cutbacks in public sector funding would incur immediate adverse volume effects due to direct correlation between grant availability and equipment ordering schedules [S1]. This risk is compounded by economic uncertainties shaping political budgetary priorities.

Governance is notably concentrated with Mr. Kornelsen controlling approximately 77% of outstanding shares providing disproportionate influence over board composition and strategic direction [S7]. While this consolidation ensures aligned leadership focus especially evident in financing transactions like the SpinDetect loan, it raises potential governance scrutiny from minority shareholders regarding decision-making transparency or conflict-of-interest scenarios.

Regulatory landscapes add compliance burdens including Sarbanes-Oxley Act mandates and evolving SEC disclosure standards which escalate administrative expenses while diverting management bandwidth away from operational objectives [S6]. Cybersecurity risk is acknowledged given data privacy regulations governing information handled via connected devices; breach repercussions could heighten financial liabilities or reputational damage [S21].

Competition from advancing sensor technologies threatens erosion of Lifeloc’s federated fuel cell advantage requiring sustained R&D investments which are inherently risky and capital-intensive without guaranteed commercial success [S20][S29].

Key Milestones Ahead: Product Launch Timelines and Funding Needs

Attention centers on SpinDetect’s development progress correlated with usage of recently secured funds under Kornelsen’s promissory note financing [S2][S3]. Monitoring key R&D milestones such as prototype validation completion benchmarks or regulatory approvals will be critical gauges for commercial launch feasibility.

Additional capital raises might become necessary should delays or cost overruns materialize.

Federal/state grant renewal cycles represent another milestone sensitive area impacting order visibility beyond the near term. Competitive activity particularly innovations by rival firms deploying alternative sensors will require vigilant tracking given potential market share shifts.

Financial Position: Liquidity Strength Underpinning Growth Ambitions

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $4.37mm | |

| 2026-03-31 | ||

| Current liabilities | $1.06mm | |

| 2026-03-31 | ||

| Current ratio | 4.11x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Despite ongoing net losses (-$2.47 million for year ending December 31, 2025), Lifeloc exhibits liquidity strength manifested in its current assets totaling roughly $4.37 million against liabilities near $1.06 million resulting in a robust current ratio of approximately 4.11 at March 31, 2026 [F1]. Such balance sheet positioning provides operational runway facilitating continued R&D investment including the internally financed SpinDetect program without immediate external capital dependency.

Total debt stands at about $1.24 million (best effort estimate), partially offset by sizeable cash balances yielding a net debt negative position enhancing flexibility [F1]. However, subordinated debentures bearing fixed interest expense are ongoing cost commitments that constrain free cash flow conversion absent substantial revenue improvements.

The recent related-party loan arrangement reflects pragmatic response to capital access challenges but introduces repayment obligations extending into late 2031 demanding disciplined cash management aligned with product commercialization success metrics [S3].

This analysis synthesizes verified filings through mid-2026 to provide a forward-looking yet grounded assessment based on Lifeloc Technologies’ operational updates, business model structure, competitive environment, growth initiatives focused on SpinDetect™, associated risks—including funding concentration—and consolidated financial health indicators supporting ongoing strategic execution.

Disclaimer: This report is informational only according to policy constraints provided; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments