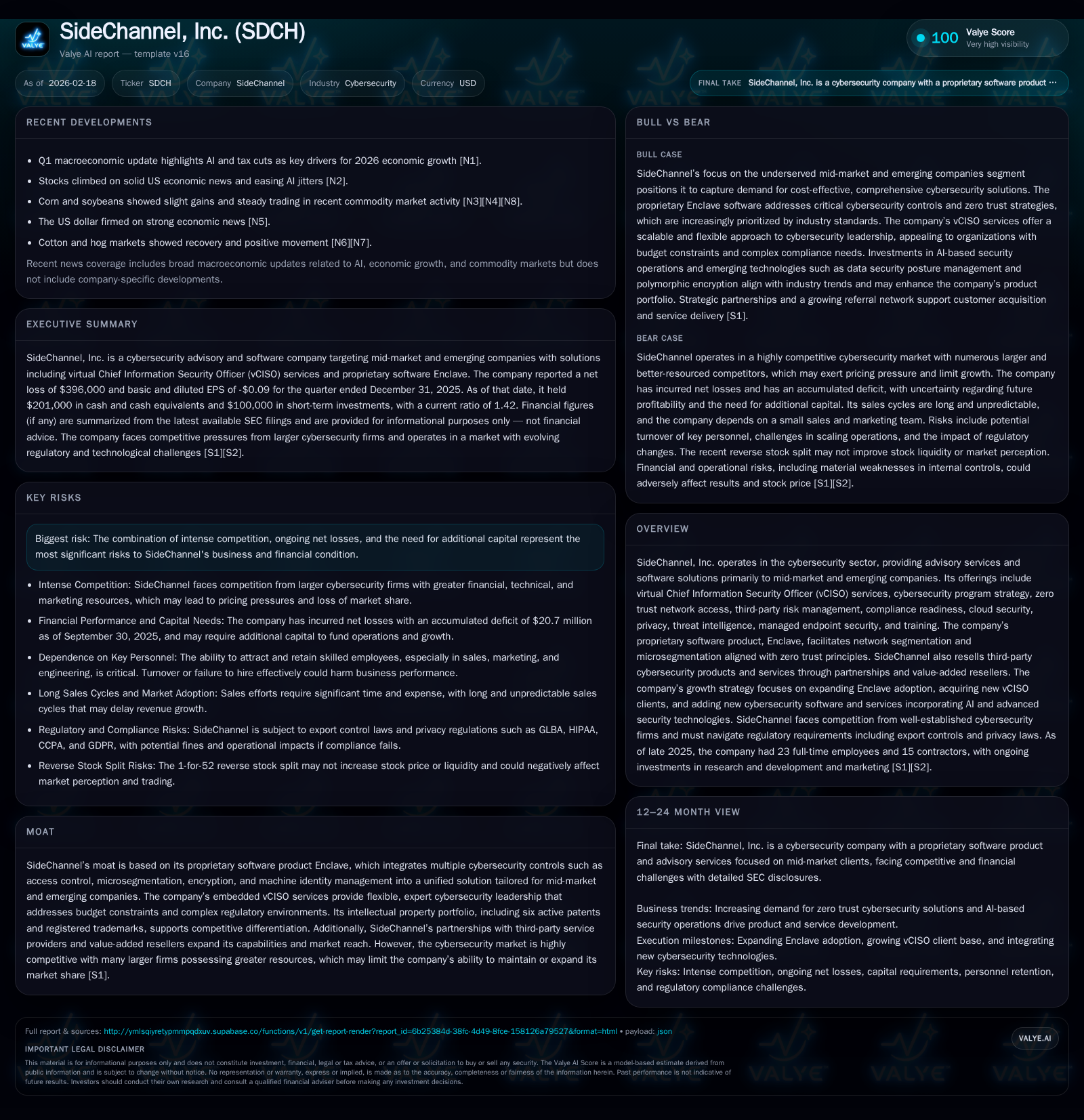

SideChannel’s Growth Balancing Proprietary Software Adoption with Persistent Operating Losses

The cybersecurity firm targets mid-market clients through its Enclave platform and vCISO services amid competitive pressures and liquidity challenges.

SideChannel, Inc. focuses on delivering integrated cybersecurity solutions tailored to mid-market and emerging companies, leveraging its Enclave software and virtual Chief Information Security Officer (vCISO) services to address growing zero trust and compliance needs. Historically, revenue has stagnated around $316K annually, with sizeable operating losses persisting above $900K in the latest fiscal year and negative operating cash flows. The company’s strategic growth relies on boosting adoption of Enclave and securing new vCISO clients, alongside integrating AI-driven enhancements. However, intense competition from well-established cybersecurity firms, combined with ongoing financial losses and dependence on additional capital raises, constrains near-term profitability prospects. Careful execution in scaling sales efforts and managing operational costs will be critical to improving financial health going forward.

Company Overview and Market Position

SideChannel, Inc. operates within the cybersecurity space focused on mid-market and emerging companies—a segment it identifies as underserved by larger competitors [S1][S10]. The company offers a blend of advisory services including virtual Chief Information Security Officer (vCISO), risk management consulting, compliance readiness support, cloud security advisory, threat intelligence, managed endpoint protection, and security awareness training. Central to its product suite is Enclave—a proprietary network segmentation software designed around zero trust network access principles to combat modern threats like ransomware [S1][S10].

The firm's strategy emphasizes integrated solutions that simplify complex cybersecurity requirements for smaller enterprises confronting budget constraints and expanding regulatory demands. By embedding fractional-vCISOs into client leadership teams and providing technology-enabled risk mitigation bolstered by AI-powered post-detection automation, SideChannel aims to deliver tailored value in a crowded market landscape [S1][S10].

Historical Financial Performance

SideChannel's revenue has essentially plateaued around $316K over recent fiscal periods ([F1]), indicating challenges in scaling sales or market penetration:

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | -130000 | -1 | 15000 | +1.3% |

| 2024 | -1 | 307000 | -1 | 15000 | +87.1% |

| 2023 | -7 | -1945000 | -7 | 32000 | +40.5% |

| 2022 | -12 | -396000 | -12 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -145000 | -41.6 |

| 2024 | 292000 | -33.4 |

| 2023 | -1977000 | -231.2 |

| 2022 | -125.3 |

Source: SEC companyfacts cache [F1].

*FY2025 figures represent the year ended September 30, 2025 except where otherwise noted ([F1]).

Operating losses remain substantial but showed slight improvement year-over-year: operating income improved by approximately 2.3%, while net losses decreased by about 1.3% from FY2024 to FY2025 [F1]. However, operating cash flow turned negative again in FY2025 following positive cash flow in FY2024, underscoring ongoing liquidity pressures [F1]. Capital expenditures have remained minimal and steady at roughly $15K annually.

Shareholders’ equity declined from $2.7 million in FY2024 to $2.14 million by FY2025 end due to cumulative operating deficits impacting net asset value [F1]. Calculated return on equity stands near -42%, highlighting persistent unprofitability.

Growth Drivers and Strategy

SideChannel's growth strategy centers on:

Scaling Enclave adoption: The proprietary Enclave platform integrates zero trust elements such as microsegmentation, encryption, access control, and machine identity management aimed at cost-conscious mid-market customers seeking enhanced network security [S1][S10]. Demand for zero trust architectures is rising amid increased remote work vulnerabilities [N1].

Expanding virtual CISO engagements: Fractional vCISOs provide flexible expert cybersecurity leadership suited for smaller firms facing complex regulatory environments and budget constraints—positioning SideChannel competitively against traditional service providers [S1][S10].

Enhancing AI-driven capabilities: Incorporation of AI-based threat detection/hunting and automated incident response playbooks aims to keep pace with industry leaders investing heavily in AI security operations [S5][S16][S10].

The company also leverages partnerships with third-party vendors and value-added resellers to extend market reach beyond its limited direct sales force of three marketing personnel as of the latest filings [S11]. Digital marketing efforts, events participation, direct outreach, and referral partner programs form key components of customer acquisition.

Risks and Challenges

Key risks include:

Intense competition: Larger incumbents with greater resources offer broader product suites often bundled competitively against standalone solutions like Enclave; cloud-native security providers add pressure on traditional delivery models [S5][S8][S16].

Ongoing financial losses: Continued operating deficits have eroded equity requiring additional capital raises which may dilute shareholders or impose restrictive terms; availability of financing remains uncertain given market conditions [S7][S13][F1].

Limited sales capacity: Small sales/marketing team restricts ability to rapidly expand pipeline or accelerate customer acquisition; long sales cycles typical of cybersecurity products add complexity [S25].

Regulatory & litigation exposures: Escalating global data privacy laws increase compliance burdens; intellectual property risks related to AI technologies add expense uncertainties [S4][S6][S12][S21].

Reverse stock split impact: The recent 1-for-52 reverse stock split reduces share count significantly but may negatively affect liquidity or market perception without guaranteeing price gains [S2][S20].

Capital Allocation and Returns Analysis

SideChannel has never paid dividends nor currently plans to do so given its financial condition [S14]. Capital expenditures are low relative to revenues consistent with a software-centric business model. Share repurchases are nominal historically (approximately $40K in FY2021), with none disclosed recently [F1][S14].

Free cash flow remains negative—estimated near -$145K for FY2025—reflecting continued cash burn at the operating level after minimal capex investments [F1]. The approximate return on equity of about -42% underscores the absence of profitability.

Outlook Considerations

Management guidance is not available in the provided documents /, but key factors for monitoring include:

- Pace of Enclave deployments and new client conversions.

- Growth trajectory of vCISO engagements alongside retention rates.

- Margin trends influenced by hiring skilled personnel without inflating costs excessively.

- Success integrating AI-driven innovations that differentiate offerings.

- Ability to raise capital timely under favorable terms mitigating dilution risk.

Industry tailwinds favor zero trust adoption amid rising cyber threats and regulatory complexity; however, execution risks remain significant given current financial constraints.

Conclusion

SideChannel occupies a challenging niche targeting cost-sensitive mid-market firms with integrated zero trust software and fractional advisory services. While its proprietary Enclave platform combined with vCISO offerings presents a differentiated value proposition aligned with evolving security paradigms, historical flat revenues coupled with sustained operating losses highlight hurdles scaling amid a competitive landscape dominated by well-funded incumbents.

Near-term priorities include managing liquidity prudently while expanding sales capacity. Modest R&D investment focused on AI augmentation signals strategic intent but translating this into profitable growth remains uncertain given resource limitations.

Investors should monitor quarterly cash flow trends, technology advancements including third-party integrations, partnership expansions, and any disclosures regarding backlog or guidance that may indicate inflection points toward sustainable profitability.

This report is based solely on publicly available information including SEC filings as of February 18, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments