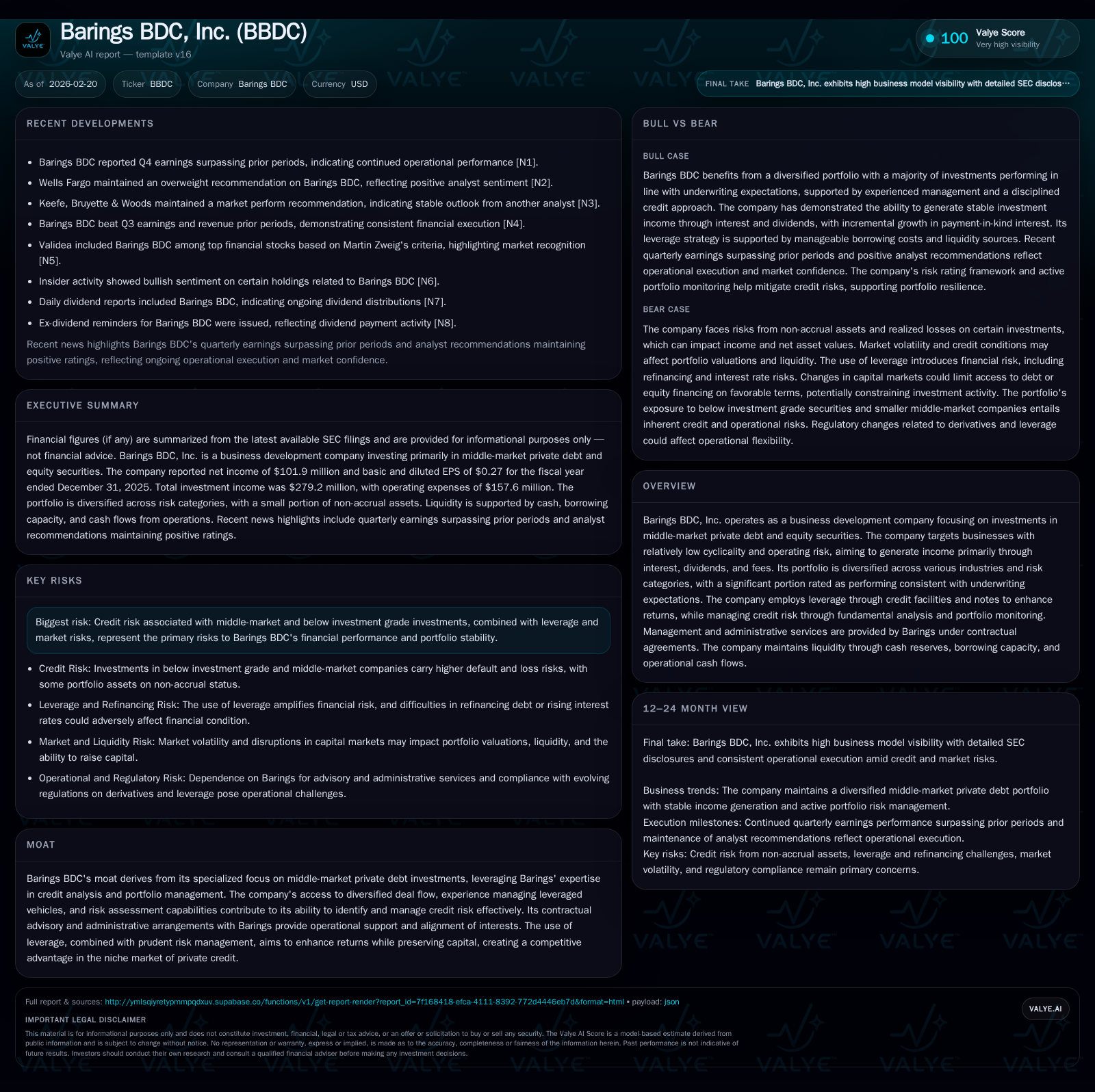

Barings BDC Expands Its Private Debt Stronghold While Managing Credit Risks

Barings BDC leverages disciplined credit analysis and calibrated leverage to sustain income in middle-market private debt.

Barings BDC, Inc. focuses on middle-market private debt and equity investments targeting lower-cyclicality businesses. Although net income declined modestly in 2025 after peaking in 2023, operating cash flow increased substantially, underscoring resilient income collection amid evolving credit risks. The company maintains a conservative portfolio risk profile with majority assets performing in line with underwriting expectations and low non-accrual exposure. Its capital structure features an amended revolving credit facility providing flexibility to deploy leverage prudently, complemented by a steady dividend policy and opportunistic share repurchases. Looking ahead, Barings BDC’s growth will hinge on its ability to source resilient credits amid macroeconomic uncertainties while managing credit risk through robust monitoring.

Historical Performance and Key Drivers of Growth

Barings BDC’s net income trajectory reflects a firm balancing growth ambitions with prudent risk management in the volatile middle-market private debt space. Net income climbed notably from just $4.7 million in 2022 to a peak of approximately $128 million in 2023, driven by increased investment yields and expanding portfolio scale [F1]. However, the subsequent year saw a moderation with net income retracting nearly 7.6% to about $102 million as credit conditions tightened across portions of the portfolio [F1][N1]. Despite this, the company reported robust operating cash flow growth—up over 31% year-over-year—indicating effective collection of interest and fees amid portfolio shifts [F1]. Stockholders’ equity remained stable near $1.16 billion through these years, underpinning balance sheet steadiness against earnings volatility.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 102 | 161 | -7.6% |

| 2024 | 110 | 122 | -13.8% |

| 2023 | 128 | 77 | +2634.4% |

| 2022 | 5 | 86 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 125 | 6 | 8.8 |

| 2024 | 27 | 6 | 9.3 |

| 2023 | 109 | 15 | 10.7 |

| 2022 | 94 | 32 | 0.4 |

Source: SEC companyfacts cache [F1].

*Substantial increase from low base in transition year.

*Note: Revenue and Operating Income figures are not available in provided tags; ROE calculated as net income divided by stockholders’ equity.

Investment Portfolio Risk Profile and Credit Quality Evolution

The core strength of Barings BDC lies in its disciplined focus on less cyclically sensitive middle-market firms characterized by manageable operating risks [S1]. The Adviser employs an internally developed five-tier risk rating system ranging from Category 1 (materially above underwriting expectations) to Category 5 (substantially below expectations) to assess issuer performance and risk migration continuously [S1]. As of December-end 2025, the largest share of portfolio fair value—about 72%—fell into Category 2, confirming most investments are performing as expected relative to their original terms [S1][N1].

Adverse ratings representing elevated credit risk decreased notably from approximately 26% (categories 3–5 combined) in late 2024 down to about 19% a year later [S1]. Non-accrual assets remained tightly controlled at roughly $17 million or just around 0.7% of total portfolio fair value—a figure that signals strict loss containment despite market headwinds [S1]. Sector exposures were diversified across various industries, which helps mitigate concentration risk.

This stable yet vigilant credit quality stance reflects successful portfolio monitoring and selective reinvestment strategies amid ongoing macroeconomic pressures.

Capital Structure and Leverage Framework

Leverage optimization forms a linchpin of Barings BDC’s strategy to enhance returns while preserving capital integrity [S5][S6]. The company’s principal debt facility—the February 2019 Credit Facility—is a senior secured revolving credit line originally sized at $800 million but incrementally expanded via its accordion feature up to current commitments of $825 million following amendments extending revolving periods through November 2030 [S5][S14]. Such accommodations ensure ample borrowing capacity aligned with prevailing financial covenants.

Interest rates are set based upon term SOFR plus spread or alternate base rate options depending on currency denomination, with foreign currency borrowings offering natural hedges via spot rate translation exposure managed within Treasury policies [S6][S9]. Notably, fixes like the September 2028 Notes issuance paired with interest rate swaps serve as complementary tools to mitigate rate volatility impact on financing costs [S7].

As of year-end, borrowings denominated in Euros accounted for approximately €193 million ($227 million USD), illustrating Barings BDC’s geographic asset diversification within its leveraged structure [S9]. The company remains compliant with all covenants across its indebtedness spectrum including notes maturing through late decade [S23][S25], reflecting prudent financial stewardship crucial for sustaining access to cheaper funding sources.

Dividend Policy and Share Repurchase Activities

Consistent with its business development company designation prioritizing income stability, Barings BDC maintained strong dividend discipline coupled with shareholder-friendly buyback initiatives [S4][S7]. Dividend payments surged from about $27 million in FY24 to over $125 million in FY25—a nearly fivefold increase highlighting enhanced distributable earning capability during the period dominated by cash collections from debt instruments [F1][S19].

Simultaneously, the Board authorized a $30 million share repurchase program starting March 2025 aimed at opportunistic buybacks below NAV thresholds [S4][S11]. During calendar year ’25, approximately $6.3 million was deployed to repurchase roughly seven hundred thousand shares at an average cost near $9 per unit [F1][S11], demonstrating measured capital allocation balancing immediate returns versus reserve liquidity.

Management explicitly notes no guaranteed level or timing for repurchases within stated plans given market dynamics but emphasizes preserving flexibility to support stock price undervaluation scenarios without jeopardizing operational funding or growth objectives [S11].

Future Prospects: Economic Conditions and Investment Pipeline

Barings BDC projects forward growth anchored primarily on sustaining access to middle-market private debt originations characterized by lower volatility sectors such as healthcare, industrials, and essential services [N1][S1]. Inflationary trends and monetary tightening pose risks due to potential margin compression or borrower stress but diversified industry allocations temper concentrated downside impacts [N1]. Management commentary underscores active sourcing from credits exhibiting stable cash flows rather than highly cyclical or speculative enterprises.

Further capital deployment opportunities reflect an investment pipeline enriched by Barings’ proprietary origination network combined with fund-specific mandates emphasizing capital preservation alongside yield enhancement strategies [N1]. Macroeconomic uncertainties could cap upside; however, flexible leverage capacity paired with ongoing credit surveillance positions Barings favorably to selectively augment positioning as conditions allow.

Credit Risk Management and Portfolio Monitoring Practices

A hallmark of Barings BDC’s investment process is its customized multi-category credit rating apparatus coupled with continuous fundamental analysis driving real-time portfolio adjustments when required [S1][S2]. Loans identified as potentially impaired or underperforming transition through categories ascending toward non-accrual designation where interest recognition ceases until remedial actions restore collectability or final settlements conclude.

This systematic rating mobility mechanism equips management with early warning signals enabling tactical reallocations and loss mitigation before material adverse effects manifest financially [S2]. Such rigor manifests in historically low default experience relative to peers alongside prudent write-downs reflecting conservative asset valuation practices enhancing investor confidence.

Market Positioning within Middle-Market Private Debt

Barings BDC’s competitive edge stems from its embedded relationship within the broader Barings platform—a global asset manager with deep credit underwriting expertise and established middle-market deal access unmatched by standalone vehicles [N1]. This structural alignment affords preferential pipeline flow plus centralized back-office efficiencies fostering scalable governance frameworks.

The compact focus on businesses exhibiting lower cyclicality shields the fund somewhat from typical mid-cap economic swings encountered elsewhere in leveraged lending or broadly syndicated loans spheres—a subtle moat differentiator critical during unstable cycles where default contagion can emerge rapidly.

Their contractual advisory arrangement ensures tightly aligned incentives between asset managers’ performance assessments and operational execution facilitating disciplined portfolio construction responsive to evolving market signals.

Key Metrics to Watch: NAV, Earnings, and Capital Deployment Trends

Though explicit guidance remains absent from filings beyond recent earnings announcements, stakeholders should vigilantly monitor quarterly updates especially concerning NAV variability relative to share price movements reflective of underlying asset mark-to-market shifts [N1]. Net income volatility vis-à-vis operating cash flow outcomes may also potentially presage emerging credit stress scenarios warranting scrutiny around forward-looking impairments or reserve adjustments.

Capital allocation evolution capturing leverage utilization trends alongside distribution stability will reveal management’s balancing acts between yield pursuits versus capital preservation imperatives under increasingly complex macro-financial conditions.

Consistent transparency into incremental portfolio composition changes by sector and risk category provides frontline insight into potential pivot points affecting medium-term return trajectories.

Disclaimer: This analysis synthesizes data exclusively drawn from Barings BDC public SEC filings and publicly available news as of February 20, 2026 without projecting specific investment outcomes or recommendations for shareholders or potential investors. Readers should independently verify details before forming financial opinions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments