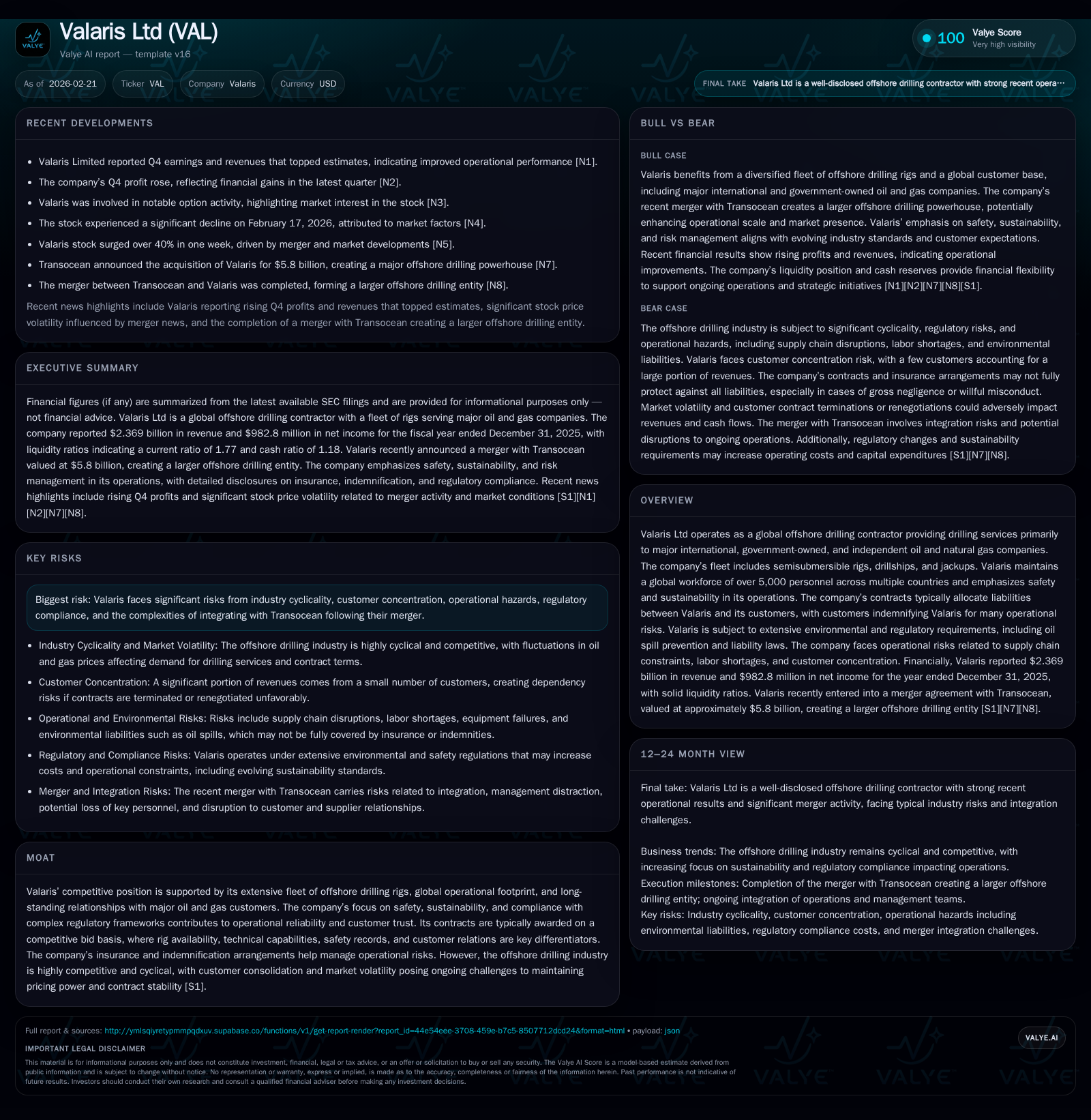

Valaris Ltd: Surging Earnings and Merger Dynamics Redefine Offshore Drilling

Valaris reports strong 2025 earnings amid its transformative merger with Transocean, navigating complex industry risks.

Valaris Ltd demonstrated remarkable financial performance in 2025, delivering steady revenue with significant rises in operating and net income. The company's merger with Transocean is set to reshape its competitive positioning, offering scale benefits but also integration challenges. Regulatory pressures and customer concentration remain critical risks that could influence future contract negotiations and operational costs. Capital allocation favors share buybacks supported by solid cash flows, while ongoing monitoring of day rate trends and contract renewals will be key for sustaining growth.

Financial Trajectory: Revenue Stability Coupled with Profit Surge

Valaris Ltd's full-year 2025 results revealed a nuanced financial trajectory characterized by stable top-line growth and robust bottom-line expansion [F1], [N1]. Revenue climbed slightly by 0.3% to $2.369 billion versus $2.362 billion in 2024, underscoring steady market demand despite the volatile offshore drilling cycle [F1]. More striking was the leap in operating income by 35.4%, reaching $477 million from the prior year's $352 million. This strength cascaded to net income which more than doubled (+163.2%) reaching $982.8 million, reflecting enhanced operational leverage and likely margin expansion [F1]. The operating margin progression suggests that Valaris has effectively optimized rig utilization or contracted more lucrative day rates.

Operating cash flow surged by 53.7% to $546 million, driven by higher profitability and possibly disciplined working capital management [F1]. Meanwhile, capital expenditures fell sharply (-24.5%) to approximately $343.5 million, contributing to a healthy free cash flow estimate of about $203 million (operating cash flow minus Capex) [F1]. These trends collectively demonstrate improved cash conversion efficiency amid prudent investment spending.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2.4 | 983 | 546 | 477 | +0.3% | +163.2% |

| 2024 | 2.4 | 373 | 355 | 352 | +32.4% | -56.9% |

| 2023 | 1.8 | 865 | 268 | 54 | +11.3% | +390.3% |

| 2022 | 1.6 | 177 | 128 | 37 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 100 | 203 | 31.0 |

| 2024 | 126 | -100 | 16.7 |

| 2023 | 199 | -429 | 43.5 |

| 2022 | -79 | 13.7 |

Source: SEC companyfacts cache [F1].

Note: Operating Income = OpInc; Net Income = Net Inc; Operating Cash Flow = CFO; Capital Expenditures = Capex; YoY % = Year-over-Year Percent Change.

Sector-native detail: The pronounced jump in net income relative to operating income often reflects non-operational gains or improved financing terms common in offshore drilling during cyclical upswings.

Drivers Behind Earnings Growth: Operational Efficiency and Market Demand

Underlying the earnings acceleration are amplified rig utilizations and fleet modernization efforts that improve competitive positioning in bidding scenarios [S1], [N1]. Valaris operates a diverse fleet comprising semisubmersible rigs, drillships, and jackups, crucial for matching customer project demands worldwide to maintain high utilization rates—key for day rate optimization.

Contracts are customarily negotiated on a competitive bid basis where factors such as rig availability, safety records, technical capabilities, and term length dictate pricing dynamics per bid cycle [S1]. Valaris' contracts include indemnification provisions wherein customers assume liabilities arising from well-control events—like blowouts—mitigating operator risk exposure significantly [S1]. Such contractual risk-sharing improves risk-adjusted returns amidst an inherently hazardous offshore environment.

Market demand improvements stem from increased exploration activity by major international oil companies following commodity price stabilization [N1]. However, aggressive cost controls and capital discipline among customers temper potential day rate uplifts despite tightened rig supply-demand balances—a typical market tension point impacting offshore drilling returns.

Sector-native mention: The capacity to negotiate favorable day rates while balancing operational uptime is critical given elevated technical maintenance needs and regulatory compliance costs, particularly for deepwater rigs.

Navigating Merger Implications: The Transocean-Valaris Integration

The recent merger creating a combined offshore drilling giant consolidates resources across fleets, enhancing geographic coverage and technical depth [N4], [N9]. Synergies target cost reduction through fleet rationalization and enhanced bidding leverage for large-scale projects due to increased capacity.

Integration complexity centers around unifying operational cultures, aligning contractual obligations amid overlapping customer bases, and managing regulatory approvals pertinent to consolidation antitrust concerns [S1], [N9]. Customer concentration effects are magnified post-merger as some clients now command greater buyer power potentially pressuring contract renegotiations or adjustments [S5].

The merged entity aims to bolster technical capabilities including advanced well-control event management systems—an important competitive differentiator influencing contract award decisions post-merger.

Regulatory and Environmental Risks Shaping Operational Realities

Valaris operates under stringent regulatory frameworks encompassing international conventions like MARPOL and national laws such as the U.S. Oil Pollution Act of 1990 (OPA90), mandating rigorous oil spill contingency planning and financial liability exposures [S8], [S9], [S10].

Insurance programs typically cover third-party liabilities up to approximately $855 million but do not entirely absolve operators from gross negligence liabilities or uncovered events under named windstorms specific policies for Gulf of Mexico floaters [S1], [S8].

Contractual indemnifications largely shift pollution-related losses back onto customers when sourced from wells or reservoirs yet leave residual liabilities tied to operator negligence unprotected or capped under specific limits affecting potential loss severity exposure [S20].

Risk vocabulary: Hull & machinery insurance plays a critical role protecting against rig damage excluding specific perils; however well control event indemnities are central because even small incidents generate disproportionate regulatory fines and remediation costs.

Environmental compliance costs are rising globally alongside tightening emissions standards resulting from sustainability initiatives that could necessitate additional investments in emissions-reduction technologies increasing operating expenses over time [S13], [S17].

Customer Concentration and Contract Structures: Risk and Opportunity

During fiscal year 2025, Valaris' top five customers accounted for nearly half of consolidated revenues (49%), highlighting significant counterparty concentration risk alongside dependency on major oil firms’ capital expenditure strategies [S5], [S23]. The largest single customer contributed about 13% of total revenues.

Contracts incorporate standard clauses allocating most well-control event liabilities to customers via indemnity agreements helping manage operational hazard risks effectively though these can vary by negotiated terms reflective of market conditions at signing times [S1], [S20].

The cyclical industry environment subjects day rates to renegotiation pressures especially post-merger where larger customers may leverage size for concessions adversely impacting revenue visibility and margins going forward.

Counterparty credit risk is nontrivial given industry consolidation; failure by key operators to fulfill commitments or early contract terminations could materially impact Valaris’ cash flows.

Day rate risk nuances dictate close monitoring of contract terms expiration dates alongside spot market volatility impacting pricing between firm commitments.

Capital Allocation Trends: Focus on Share Buybacks over Dividends

Valaris has abstained from dividend payments since at least FY2019 but actively pursued share repurchases totaling approximately $100 million in FY2025 supported by strong free cash generation (~$203 million) despite reduced capital spending compared to prior years [F1]. This signals management preference for enhancing shareholder value via capital return through buybacks over direct dividends.

Return on equity rose significantly owing to surging net incomes against shareholders’ equity base of roughly $3.17 billion in FY2025 translating into an approximate ROE of about 31%, indicative of efficient profit generation relative to capital employed [F1].

Liquidity remains ample with a current ratio near 1.77 supporting ongoing operational requirements and enabling continued shareholder-friendly capital deployment amidst restrictive covenant frameworks attached to existing indebtedness per credit agreements limiting dividend distributions and share repurchases contingent on covenant compliance [S7], [F1].

Free cash flow expansion stems mainly from disciplined capex reductions (-24.5% YoY), offsetting increases in operational costs associated with regulatory compliance and workforce expenses.

Future Outlook: Monitoring Contract Renewal and Dayrate Trends (Analytical)

Looking forward, key catalysts encompass successful renewal of existing long-term contracts at competitive day rates amid heightened pricing competition due to excess rig supply following industry downturns and uncertain customer project schedules exacerbated by geopolitical tensions impacting exploration budgets [N1], [N4], [S1].

Fleet modernization initiatives post-merger will also determine competitiveness in technical capability critical for securing high-value deepwater contracts involving complex well-control event risk mitigation standards.

Given rising regulatory overheads forecasted globally alongside potential shifts in customer priorities towards sustainability-linked contracting requirements, maintaining margin integrity will require adaptive cost controls coupled with agile bid strategy focusing on demonstrating exceptional safety metrics—a primary determinant in award decisions within this segment.

Sector-native observation: Bid competitiveness increasingly depends on demonstrated compliance with evolving environmental safeguards alongside proven uptime reliability metrics related directly to fleet maintenance regimes.

Balance Sheet Strength and Liquidity Amid Industry Cyclicality (Analytical)

As of December-end FY2025, Valaris’ balance sheet reflects robust liquidity evidenced by cash & equivalents of approximately $599 million against current liabilities near $692 million yielding a comfortable current ratio around 1.77 supporting near-term liquidity needs without stress under normal operations [F1], [S7].

Debt covenants embedded within the Indenture and Credit Agreements impose restrictions on incremental borrowings, capex outlays, share repurchases, and dividend payouts functioning as safeguards amidst cyclical downturns but may constrain maneuverability during unexpected shocks or integration-related investments post-merger [S7], [S24].

Interest coverage ratios required under financial covenants necessitate sustained EBITDA levels committing management focus toward operational efficiency gains concurrently with deleveraging efforts where feasible.

Potential refinancing risk exists if adverse market conditions coincide with debt maturities but current industry tailwinds together with merged scale should underpin continued access to capital markets if necessary.

Disclaimer: This analysis is prepared solely for informational purposes reflecting available data as of February 21, 2026, without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments