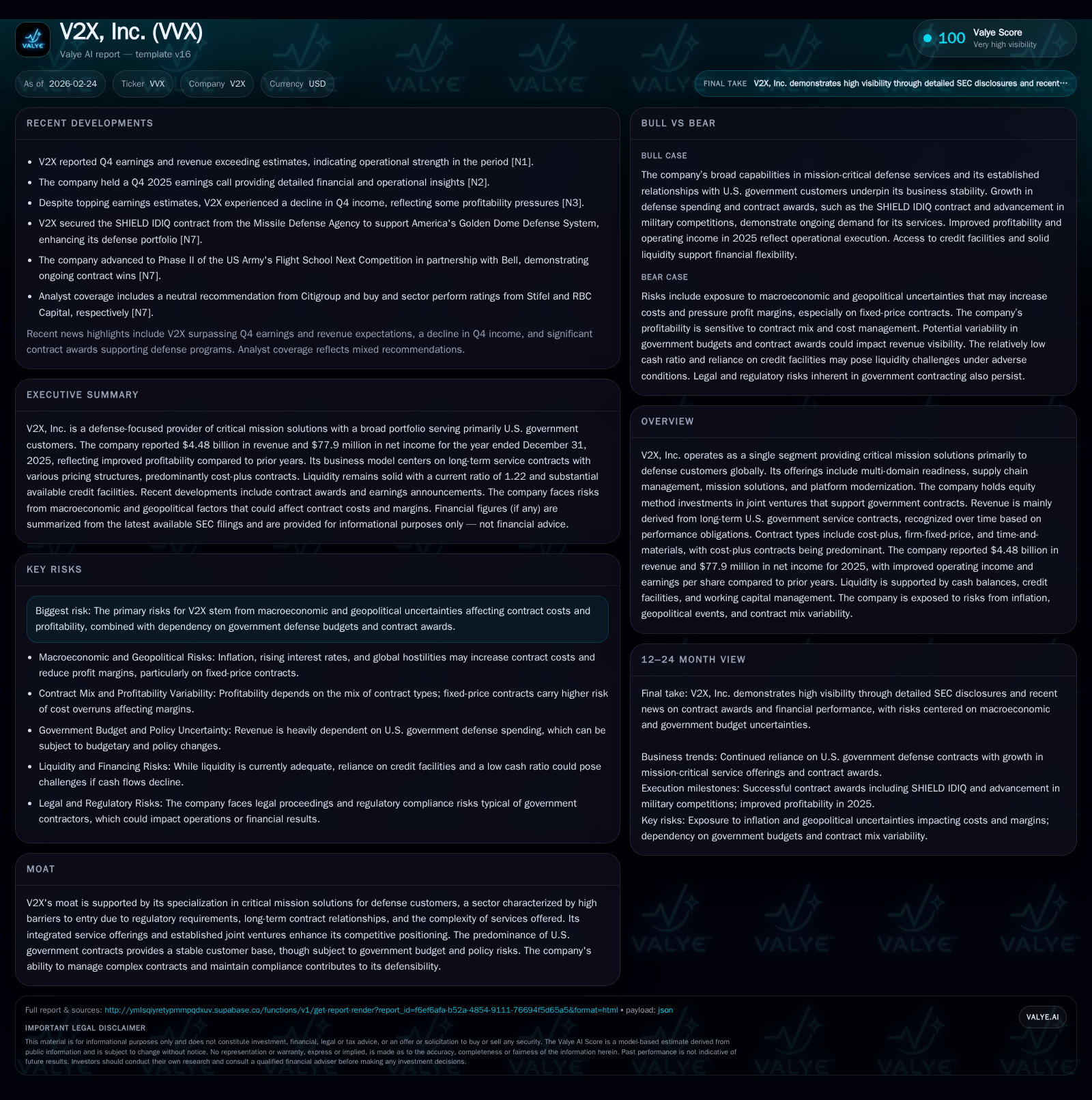

V2X Drives Defense Sector Growth Through Contract Excellence and Capital Efficiency

V2X leverages long-term government contracts and disciplined capital management to build resilient growth and profitability despite evolving defense budget dynamics.

V2X, Inc. reported robust financial improvements in 2025, driven by its performance on key defense contracts such as LOGCAP V Kuwait Task Order. The company’s revenue recognition closely tracks long-term, predominantly cost-plus contracts, providing stable but timing-sensitive topline trends amid a $1.4 billion backlog decline. Growth is supported by multi-domain readiness and supply chain solutions aligned with shifting U.S. defense priorities, while recent contract awards and legal successes bolster near-term funded backlog replenishment. Capital allocation reflects a focus on free cash flow deployment to share repurchases and debt management, underpinning a solid liquidity position and controlled leverage. Investors should monitor funded backlog dynamics, option exercises on core contracts, and government budget execution as critical indicators for fiscal 2026.

Strong Historical Performance Anchored by Major Government Contracts

V2X, Inc.’s 2025 financial results underscore effective execution of its long-duration U.S. government service contracts, particularly cost-plus agreements which dominate its portfolio. Operating income climbed to $194 million in fiscal 2025, marking a 22% year-over-year increase from $159 million in 2024 [F1]. This improvement stems primarily from enhanced operational efficiencies and favorable contract modifications within major programs like the Logistics Civil Augmentation Program (LOGCAP) V Kuwait Task Order, which contributed nearly 10% of total revenue in both years with over $440 million recognized in 2025 alone [S1].

Despite sector-wide challenges related to government budget fluctuations and procurement complexities, V2X’s ability to recognize revenues in alignment with performance obligations under these contracts has enabled steady growth momentum. Net income’s rebound from losses in prior years — reaching $77.9 million in 2025 (a 124.5% increase) — further illustrates improved profitability powered by scale-leveraging on core contracts and cost discipline [F1]. Cost-plus contracts mitigate margin pressure stemming from inflationary inputs through contractual cost recovery mechanisms, reinforcing revenue reliability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 78 | 182 | 194 | 12 | +124.5% |

| 2024 | 35 | 254 | 159 | 12 | +253.7% |

| 2023 | -23 | 188 | 124 | 25 | -57.5% |

| 2022 | -14 | 93 | 56 | 12 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 170 | 7.2 |

| 2024 | 242 | 3.4 |

| 2023 | 163 | -2.3 |

| 2022 | 81 | -1.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue data unavailable from tags; YoY values calculated where possible [F1]

The Impact of Backlog Shifts and Contract Timings on Revenue Recognition

V2X disclosed a substantial $1.4 billion reduction in total backlog from $12.5 billion at the end of FY2024 to $11.1 billion at end FY2025 [S1]. This decline largely reflects the timing of contract awards vis-à-vis revenue recognition schedules rather than loss of business.

Of particular note is the breakdown between funded backlog ($2.3 billion in FY2025 vs $2.25 billion prior year) and unfunded backlog ($8.8 billion down from $10.3 billion). Funded backlog aligns with contractually authorized appropriations from the U.S government and forms the base for near-term revenues recognized over time per meeting performance obligations under complex IDIQ (Indefinite Delivery Indefinite Quantity) arrangements.

The variable nature of option periods embedded in multi-year contracts leads to cyclical backlog fluctuation since exercise rights reside solely with government customers or prime contractors when V2X is a subcontractor [S1]. Moreover, several awards are subject to competitive protests that impose stop-work orders delaying order flow and potentially elongating revenue recognition timelines.

As such, analyzing backlog changes requires careful differentiation between net decreases attributable to sustained burn-down versus delays or shifts induced by acquisition reform cycles or protest adjudications common within defense contracting frameworks.

Growth Drivers in Multi-Domain Readiness and Supply Chain Solutions

Beyond headline contract volumes, V2X’s differentiated growth rests on delivering integrated multi-domain readiness capabilities across air, land, sea, space, cyber, and electronic warfare environments per emerging national security mandates . Its platform modernization expertise aligns well with Department of Defense initiatives emphasizing agile infrastructure renewal alongside legacy system sustainment.

Supply chain management offerings are gaining importance as DoD prioritizes resilience against global disruptions amid geopolitical tensions – e.g., diversified vendor integration and inventory optimization methods embedded into mission support functions enhance V2X's value proposition.

Joint ventures using equity method accounting extend V2X’s reach into niche areas supporting government contract fulfillment that require specialized technical or region-specific competencies—critical for maintaining comprehensive service portfolios under stringent compliance requirements.

This breadth allows V2X to act as a force multiplier helping clients meet evolving threat environments through mission-essential capabilities tailored to client-specific performance obligations.

Navigating Defense Budget Priorities and Geopolitical Risk Factors

The U.S Department of Defense's FY2026 base budget request totals approximately $848 billion excluding mandatory appropriations added via the One Big Beautiful Bill Act (OBBBA), which contributes an estimated extra $113 billion aligned with DoD priorities—funding frameworks heavily influence V2X's addressable market size and contract availability [S1],[S18].

However, lingering political uncertainties around federal appropriations processes combined with defensive acquisition reform intensify pressure around contract renewals' timing & margin compression due to competitive bids seeking efficient solutions at affordable costs.

Geopolitical risks such as rising great power competition necessitate more agile multi-domain readiness programs that V2X services cater towards but may force demand fluctuations linked explicitly to episodic events or policy shifts impacting DoD spending phasing or program priorities.

Hence managing exposure amid these factors demands agile contract execution strategies—careful monitoring of appropriations progress post-October start date alongside alternative contingency planning remain vital operational considerations for sustained growth.

Insights from Recent Contract Awards and Legal Wins

Strategic contract wins reinforce V2X’s competitive foothold: In January 2026 securing the SHIELD IDIQ contract from the Missile Defense Agency positions V2X on next-generation missile defense support streams critical for layered continental defense systems [N13].

Advancing into Phase II of the US Army's Flight School Next competition alongside Bell Helicopter signals confidence in V2X’s capability envelope within advanced aviation training ecosystems [N11]. Meanwhile a recent favorable court ruling sustaining the T-6 Comprehensive Operational-Based Maintenance Services (COMBS) award following competitor protest illustrates judicial reinforcement of its existing contract portfolio stability [N8].

These outcomes suggest healthy funded backlog replenishment prospects through successful option period exercises plus newly awarded task orders—all reinforcing medium-term visibility essential given backlog-related timing nuances described above.

Capital Allocation Discipline: Evaluating Returns, Buybacks, and Cash Flow

V2X exhibits conservative capital allocation favoring shareholder returns alongside balance sheet stewardship—ROE approximates a moderate but improving ~7.2%, consistent with sector norms for large defense services firms balancing growth reinvestment imperatives versus return expectations grounded by stable government relationships [F1].

Free cash flow generation remains solid at approximately $170 million after deducting modest capital expenditures (~$12 million); this cash supports share repurchases totaling ~$30 million during FY2025 aimed at enhancing per-share metrics amid no declared dividend payouts currently [F1].

Capex levels have stayed relatively flat year-over-year (+1.2%), focused primarily on software/hardware upgrades supporting existing operations rather than materially expanding asset bases—an alignment typical among service-oriented defense primes prioritizing human capital & systems integration vs heavy infrastructure investment.

The buyback approach underscores management discipline toward flexible capital deployment calibrated against evolving marketplace conditions without compromising liquidity buffers.

Analyzing Liquidity, Debt Profile, and Future Funding Flexibility

Liquidity stands robust: cash plus equivalents totaled approximately $369 million as of December 31, 2025 backed by an undrawn revolver facility availability near $479 million—a prudent cushion against working capital volatility inherent in federal contracting workflows requiring rapid invoice collections and payments management [S4][F1].

The company carries amortizing term loans aggregating just below $890 million bearing floating rates tied to SOFR plus margins averaging close to ~6–6.5% effective interest expenses—consistent capitalization metrics supporting good interest coverage ratios above covenant minimums stipulated under its credit agreements [S7][S15][S17].

No borrowings against revolving credits at year-end indicate conservative liquidity utilization supporting operational agility plus optionality for opportunistic acquisitions or other strategic investments if desired without pressing refinancing needs.[S10]

Analysts should observe quarterly debt amortization schedules since principal repayments accelerate modestly through late decade maturity horizons enabling gradual deleveraging absent major leverage triggers reducing financing risks further.

Forward-Looking Considerations: What to Watch in Fiscal 2026

Going forward into fiscal year 2026—with explicit numerical guidance notably absent from disclosures—it is critical to monitor key metrics indicative of ongoing execution quality:

- Fluctuations in funded backlog levels driven by new awards or option exercises post-June particularly related to LOGCAP extensions through potentially mid-2030s timeframe provide directional insight into near-term revenue resilience.[S1]

- Resolution pace regarding ongoing protests affecting certain IDIQ-related awards may alter order intake unpredictably impacting timing of recognized revenue.[S1]

- Government annual budget approvals incorporating OBBBA appropriations will influence incremental funding availability essential for current program sustenance.[S18]

- Geopolitical developments impacting DoD spending patterns could catalyze shifts across multi-domain readiness demand profiles where V2X focuses service investments.[N2]

- Lastly watch for any changes in capital allocation signaling strategic shifts beyond steady buybacks including potential M&A activity leveraging existing liquidity frameworks.

Taken together these factors will shape how effectively V2X balances backlogs declines against profit margins anchored by disciplined contract performance driving sustainable growth trajectories.

Disclaimer: This analysis summarizes publicly available information about V2X, Inc., including SEC filings and news reports up to February 24, 2026; it is intended solely for informational purposes without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments