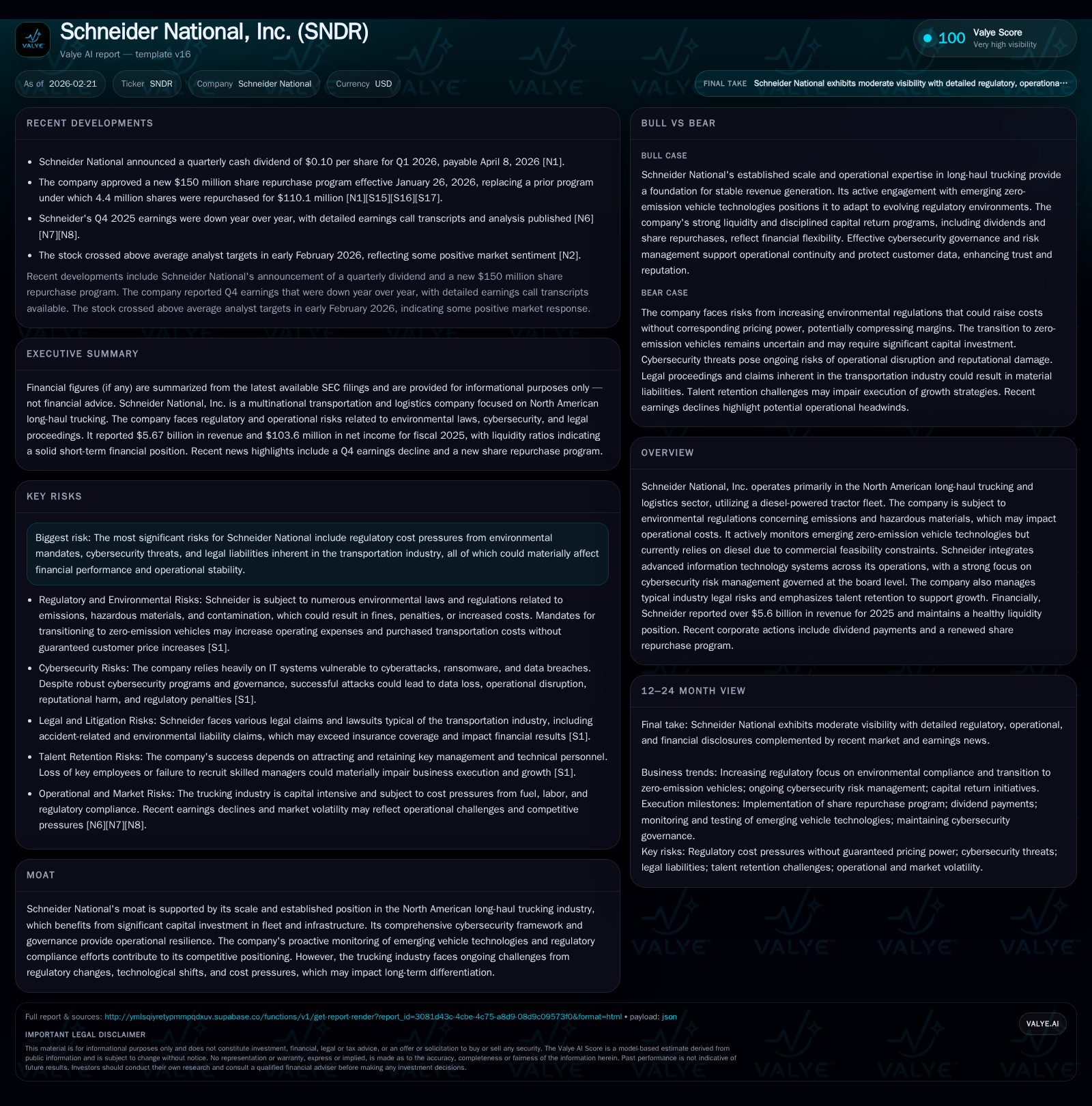

Schneider National’s Growth Pause and Capital Strategy Reflect Industry Shifts

Schneider National’s recent revenue growth slowdown and earnings compression underscore challenges from environmental regulation and diesel dependency, prompting a cautious capital allocation approach.

Schneider National experienced a deceleration in revenue growth through 2025 alongside notably shrinking operating margins driven by rising cost pressures, particularly from environmental regulations and reliance on diesel-powered Class 8 tractors. Despite these operational headwinds, the company maintains a stable free cash flow profile and recently increased dividends while renewing its modest share repurchase program. Schneider’s measured capital allocation reflects strategic caution amid evolving regulatory risks and technological uncertainty surrounding zero-emission vehicle adoption. Additionally, the company’s strong cybersecurity governance remains a key defensive capability as it navigates industry transitions.

Trajectory of Growth: Revenue, Profit, and Operating Trends Through 2025

Schneider National posted $5.67 billion in revenue for fiscal 2025, representing a modest 7.3% increase over $5.29 billion in 2024 after earlier fluctuations—$5.50 billion in 2023 and a sharp decline from $6.60 billion in 2022 [F1]. However, the growth masks significant margin pressure: operating income has been effectively cut by more than two-thirds since its peak at $600 million in 2022, falling steeply to $169 million in 2025 (a -71.9% four-year contraction). Net income followed a similar pattern, plunging from $458 million in 2022 to just $104 million last year (-77.4%), indicating pronounced earnings compression amid rising costs [F1].

This disproportionate decline reflects expanding expenses against relatively stable revenues. Operating costs linked to fuel prices, labor, maintenance for Class 8 tractor fleets predominantly fueled by diesel—the industry’s standard—have tightened margins severely [S1]. Despite steady demand supporting top-line stability, decreased profitability signals increasing headwinds within the long-haul trucking sector.

The company generated $637 million cash from operations in 2025, down from $686 million the prior year (-7.1%), sustaining positive free cash flow after accounting for capital expenditures of $352 million (a -15% reduction) [F1]. This capex pullback coincides with cautious investment amid industry shifts.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5.7 | 104 | 637 | 169 | +7.3% | -11.5% |

| 2024 | 5.3 | 117 | 686 | 165 | -3.8% | -50.9% |

| 2023 | 5.5 | 239 | 680 | 296 | -16.7% | -47.9% |

| 2022 | 6.6 | 458 | 856 | 600 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 67 | 15 | 285 |

| 2024 | 67 | 30 | 272 |

| 2023 | 64 | 67 | 20 |

| 2022 | 56 | 321 |

Source: SEC companyfacts cache [F1].

Note: Buybacks data sparse for some years; not all metrics have consistent YoY figures due to volatility.

Operational Pressures from Environmental Regulations and Diesel Reliance

Schneider National operates under intensive environmental scrutiny impacting long-haul trucking fleets reliant on diesel Class8 tractors [S1]. The company is subject to stringent laws regarding greenhouse gas emissions, hazardous materials handling, underground fuel storage compliance, storm water retention, and contamination liability at industrial facilities [S4][S22].

Despite active monitoring of emerging technologies such as hydrogen or electric powertrains for heavy trucks, Schneider acknowledges these alternatives are not currently commercially feasible at scale across North America due to powertrain performance limitations and lack of supporting fueling infrastructure [S1][S25]. Regulatory bodies including the California Air Resources Board (CARB) have paused enforcing certain stringent clean truck mandates but analogous state laws persist with uncertain enforcement trajectories [S1].

Such regulations implicitly raise operational costs by driving capital expenditures for cleaner equipment or escalating purchased transportation fees when third-party carriers must comply with costlier mandates [S1][S25]. The inability to pass these incremental costs fully onto customers could compress margins further.

Forward-Looking Stance: Technology Adoption and Regulatory Uncertainties

As zero-emission vehicle (ZEV) technology matures unevenly—with regional pilot projects possibly appearing before broad-scale rollouts—Schneider’s strategy hinges on continuous assessment of feasibility rather than imminent fleet overhaul [N3][S1][S4]. This measured stance seeks to balance early innovation risks against cost escalation tied to premature technology adoption.

Regulatory uncertainty complicates planning since federal/state mandates might emerge unpredictably affecting timing of compliant tractor deliveries from OEMs and potential need for infrastructure investments [S25]. Given these variables, capital deployment remains conservative—favoring maintain-and-monitor instead of aggressive upgrades.

Capital Allocation: Dividends, Share Buybacks, and Investment in Fleet Assets

Notwithstanding margin pressures, Schneider continues disciplined capital returns. The quarterly dividend was increased from $0.095 in Q4’25 [S11] to $0.10 starting Q1’26 payable April with shareholder record date March14 [S8][N8]. Concurrently, the company renewed its stock repurchase program authorizing up to $150 million over three years—essentially unchanged from the expiring authorization during which it repurchased approx. $110 million worth of shares [S8][S11].

Capital expenditures reduced organically reflecting careful fleet replacement aligned with technology uncertainty; capex dropped by about one-sixth compared with peak investment years [F1]. Free cash flow remains positive (~$285 million in FY25 calculated as CFO less capex), supporting stable liquidity demonstrated through a current ratio above two at year-end [F1][S16].

Return on equity remains subdued near an estimated ~3.4%, indicative of constricted profitability relative to equity base [F1]. This suggests limited financial leverage expansion opportunities absent operational turnaround.

Cybersecurity Governance as a Strategic Defensive Pillar

Given reliance on sophisticated information systems spanning freight booking to internal reporting—and heightened vulnerability as critical infrastructure participant—Schneider prioritizes cybersecurity under comprehensive governance frameworks detailed in annual disclosures [S1][S10][S18][S24].

Oversight responsibilities reside primarily with the Audit Committee which receives semiannual detailed risk updates including third-party assessments and cybersecurity control effectiveness audits [S1][S10]. Executive leaders such as Chief Information Technology Officer (CITO) and Senior Director Information Security (SDIS) bring decades of practitioner experience guiding architecture of cyber risk management programs integrated within enterprise risk management (ERM) processes.

Robust programs include threat detection partnerships with managed security service providers (MSSPs), continuous monitoring for anomalous activity, layered defense strategies against phishing/ransomware attacks common in logistics IT environments, and resilience planning covering potential operational disruptions or data breaches [S23][S24].

Key Quarterly Milestones and What Investors Should Watch Next

Recent Q4 results evidenced an earnings miss alongside top-line softness attributed partly to persistent operational challenges including regulatory compliance burdens and competitive pricing constraints on purchased transportation costs [N13]. The earnings call transcript underscores management’s commitment to balance growth aspirations with risk mitigation amidst tightening market conditions [N3].

Upcoming catalysts will include:

- Clarity on state/federal emission regulation enforcement timelines particularly regarding ZEV mandates impacting fleet renewal capex strategy,

- Progress reports on pilot deployments or investments in alternative propulsion technologies,

- Execution pace against the newly approved stock repurchase plan,

- Quarterly dividend declarations maintaining or adjusting payout trajectory,

- Evolving cybersecurity threat landscape updates as flagged by senior tech executives.

Given absence of explicit forward guidance beyond these disclosures, external observers should focus on whether Schneider can stabilize operating margins while navigating the dual imperative of environmental compliance and technological adaptation.

Disclaimer: This analysis is for informational purposes only based on publicly available information as of February 21, 2026. It is not investment advice or recommendations regarding purchase or sale of securities related to Schneider National or any other entity.

Comments