Sanara MedTech Inc: Navigating Innovation and Competitive Pressures in Surgical Medical Devices

Sanara MedTech develops specialized soft tissue repair and bone fusion medical products, leveraging R&D and strategic partnerships to compete within a challenging healthcare market.

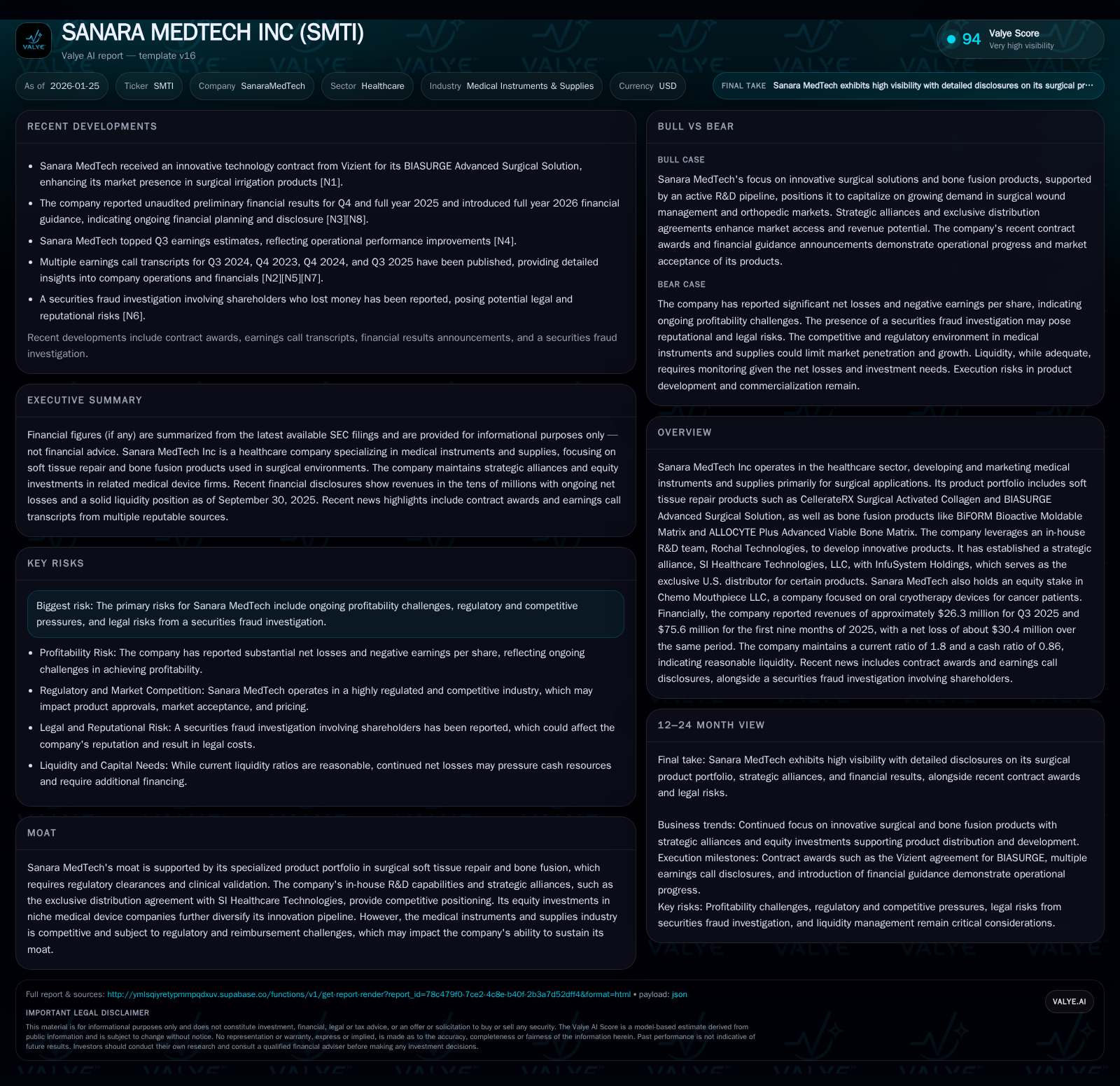

Sanara MedTech operates primarily in surgical soft tissue repair and bone fusion medical instruments, with a product portfolio centered on collagen-based and bioactive implant solutions. Recent financial reports show revenue growth but ongoing net losses amid regulatory and competitive headwinds. The company’s business model integrates in-house R&D and strategic alliances, including exclusive U.S. distribution agreements, to expand market access. However, profitability challenges and an active securities fraud investigation highlight risks in sustaining competitive advantage.

What Changed Recently

Sanara MedTech reported Q3 2025 revenues of approximately $26.3 million, surpassing earnings expectations and signaling positive top-line momentum [N3][N6]. The company also announced preliminary unaudited financial results for Q4 2025 and introduced full-year 2026 financial guidance, reflecting management’s growing confidence in execution [N2][N7]. A notable commercial development was the receipt of an innovative technology contract from Vizient for its BIASURGE Advanced Surgical Solution, a key product in the wound irrigation segment, potentially expanding hospital procurement channels [N8]. However, offsetting these operational highlights, Sanara faces ongoing legal challenges related to a securities fraud investigation with shareholder litigation underway [N9]. This legal backdrop introduces uncertainty regarding capital markets access and management focus.

Business Model as a System

Sanara MedTech operates primarily in the healthcare sector, developing and marketing specialized medical instruments and supplies for surgical applications. Its product portfolio comprises two core categories: soft tissue repair and bone fusion products. Soft tissue repair includes flagship products such as CellerateRX Surgical Activated Collagen—a hydrolyzed collagen designed to promote surgical wound healing—and BIASURGE Advanced Surgical Solution, a sterile, no-rinse wound irrigation product optimized for operating room use. Bone fusion offerings include BiFORM Bioactive Moldable Matrix, a porous implant facilitating osteoconduction and bony ingrowth, and ALLOCYTE Plus Advanced Viable Bone Matrix, a human allograft containing progenitor cells to enhance bone regeneration [S2].

The company leverages an internal research and development unit, Rochal Technologies, to develop and sustain an innovation pipeline critical for product differentiation and regulatory approvals. This R&D-driven model supports continuous product improvements and potential new launches, essential in a medical device industry where clinical validation and regulatory clearances are significant barriers to entry.

To drive commercialization, Sanara entered a 50/50 strategic alliance with InfuSystem Holdings, forming SI Healthcare Technologies, LLC, which acts as the exclusive U.S. distributor for certain product lines, including standard chemo regimen kits under an exclusive distribution agreement. This partnership is designed to capitalize on InfuSystem’s established sales infrastructure and hospital relationships, mitigating Sanara’s need to scale a standalone commercial sales force [S1].

Sanara also holds approximately a 6.6% equity stake in Chemo Mouthpiece LLC, a developer of oral cryotherapy devices aimed at reducing chemotherapy-induced oral mucositis severity. This minority investment aligns with Sanara’s strategic interest in adjacent therapeutic device markets and innovation diversification [S5].

Financially, management assesses performance mainly through Adjusted EBITDA, excluding non-cash share-based compensation, legal expenses, and other unusual costs, highlighting ongoing challenges in achieving profitability despite revenue growth [S3]. Liquidity metrics as of September 2025 show a current ratio near 1.8 with $14.9 million in cash and equivalents, suggesting reasonable short-term financial flexibility, though net losses reported at approximately $30.4 million indicate continued operational strain [S10][S13].

Industry Map & Competitive Battlefield

Sanara MedTech operates within the broader medical instruments and supplies industry, specifically targeting surgical soft tissue repair and bone fusion markets. These segments are characterized by high regulatory scrutiny (FDA clearances and ongoing compliance), reliance on clinical evidence, and dependency on hospital purchasing decisions, often influenced by group purchasing organizations (GPOs) and integrated health systems.

Competition includes large established medical device firms with broad portfolios and robust sales channels, as well as specialized niche companies innovating in collagen-based wound care and bioactive bone graft substitutes. Differentiation in this market derives from product efficacy, ease of use in sterile environments, clinical outcomes, and reimbursement favorability.

Sanara’s strategic alliance with InfuSystem via SI Healthcare Technologies is a critical tactical move to enhance distribution breadth in the U.S., where hospital relationships and GPO contracts dictate product adoption. The recent Vizient contract for BIASURGE indicates momentum in securing key procurement pathways, which can be a substantial competitive advantage given Vizient’s scale in healthcare supply chain management [N8].

However, the competitive landscape is intense with frequent product innovation, pricing pressures, and the need for clinical validation to convince surgeons and hospital committees. Additionally, reimbursement policies can vary by region and insurer, posing risks to revenue predictability.

The company’s minority investment in Chemo Mouthpiece LLC signals an attempt to expand into supportive oncology care devices, a potentially adjacent growth avenue, but one with its own competitive and regulatory challenges.

Where the Economics Become Real

Sanara’s unit economics hinge on several interrelated factors: manufacturing costs of specialized collagen and allograft materials, R&D investment for regulatory approvals, and sales and marketing expenses primarily driven by distribution partnerships.

The use of a strategic alliance for distribution reduces fixed commercial overhead but introduces dependency on third-party execution and potentially margin sharing. Securing exclusive distribution rights, as with SI Healthcare Technologies, allows for focused commercial efforts but also concentrates risk if sales targets are not met.

Pricing power depends on clinical differentiation and reimbursement status. Products like CellerateRX Surgical and BiFORM are positioned as premium solutions requiring strong clinical evidence to justify pricing amidst competitive alternatives.

The path to profitability is challenged by ongoing net losses driven by R&D spend, legal costs, and scaling efforts. The company reports significant operating expenses and non-cash charges, such as share-based compensation and impairment charges, which cloud operating margin clarity [S10]. Capital allocation decisions and expense control will be critical to transition from revenue growth to sustained profitability.

Additionally, regulatory clearance timelines and reimbursement approvals represent bottlenecks, as delays or unfavorable decisions can stall product launches or compress pricing power. The Vizient contract may help unlock volume sales and improve margin leverage if it leads to broader institutional adoption.

Diligence Questions / Disconfirming Signals

- How materially does the ongoing securities fraud investigation and associated shareholder litigation impact management bandwidth, capital access, and overall corporate governance?

- What is the current status of regulatory approvals for newer products in the pipeline developed by Rochal Technologies, and what is the timeline and probability for their market commercialization?

- How effective has the SI Healthcare Technologies alliance been in driving U.S. sales growth, and what are the terms governing revenue sharing and operational control?

- Are there any emerging reimbursement challenges or pricing pressures from hospital systems or GPOs that could erode Sanara’s product margins?

- How scalable is the company’s manufacturing capacity for collagen and bone matrix products, and what are the key supply chain risks?

- What clinical data supports the differentiation of CellerateRX Surgical and BiFORM relative to competitors, and how is this data being leveraged in sales and marketing efforts?

- Given persistent net losses, what is management’s path and timeline to achieving profitability or positive cash flow?

- How significant is the investment in Chemo Mouthpiece LLC to future revenue streams, and what strategic synergies exist?

- Are there any pending or potential regulatory or legal risks beyond the disclosed securities investigation that could impact operations?

This analysis synthesizes publicly available information and recent disclosures about Sanara MedTech Inc. It does not constitute investment advice or recommendations. The company operates within a complex, highly regulated industry where product innovation, regulatory approvals, and commercial execution critically impact financial outcomes and competitive positioning. Potential investors and stakeholders should consider these factors alongside evolving market and legal developments. The information here reflects data as of early 2026 and is subject to change with new disclosures and market conditions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments