Triumph Financial: Driving Niche Leadership in Trucking-Focused Financial Services

Triumph Financial carves a distinctive place in US trucking finance through integrated banking, factoring, payments, and data intelligence solutions.

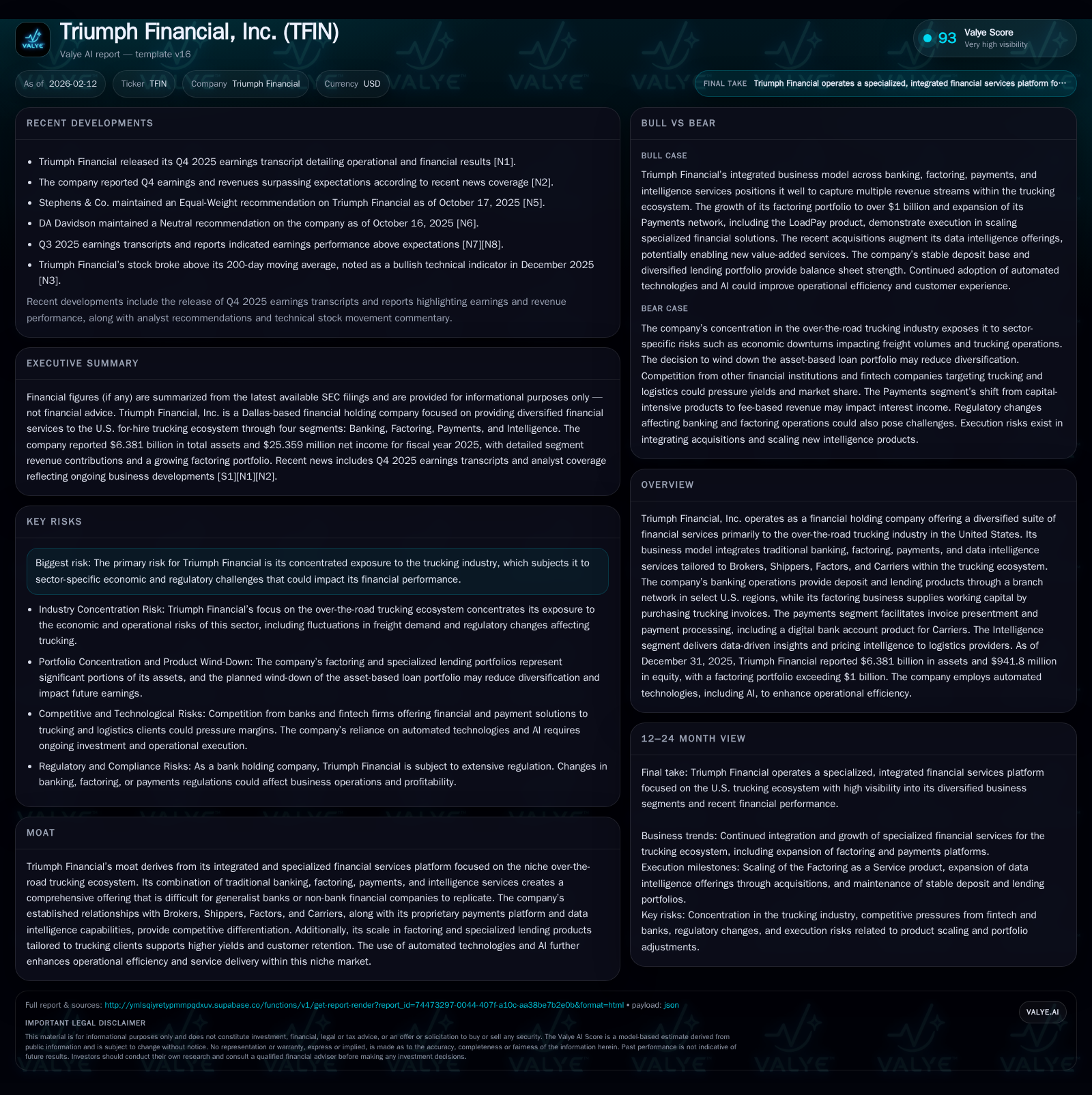

Operating primarily within the over-the-road trucking ecosystem, Triumph Financial leverages a diversified financial services platform tailored to carriers, brokers, shippers, and factors. Its blend of traditional banking, invoice factoring, digital payments, and data intelligence delivers synergistic value difficult for generic competitors to replicate. Powered by AI-enabled automation and specialized lending products, Triumph reported strong 2025 results with $6.38 billion in assets and $25 million net income. However, its concentrated exposure to the trucking sector and regulatory risks remain material considerations.

Navigating the Road: Triumph Financial’s Niche in Trucking Finance

Triumph Financial, Inc., headquartered in Dallas, Texas, has established itself as a financial holding company focused singularly on servicing the complex over-the-road (OTR) trucking ecosystem in the United States. Unlike broad-based financial institutions that spread across varied industries or geographic regions, Triumph specializes in meeting the nuanced financial needs of Brokers, Shippers, Factors, and Carriers operating within freight logistics[ S1 ]. This specialization is evident across their four interconnected segments—banking, factoring, payments, and data intelligence—all designed around trucking's unique cash flow dynamics and operational challenges.

At its core, Triumph operates not just as a bank but as an integrated financial platform addressing multiple points along the trucking value chain. For example, trucking carriers often face delayed receivables due to long payment cycles inherent in freight logistics. Similarly, brokers require streamlined invoice audits and payment reconciliation across various counterparties. Triumph’s business model converges these demands into a single ecosystem powered by modern technology enabling faster capital flow and improved visibility.

By tailoring products specifically for this market niche—notably small to mid-size fleets that represent a substantial portion of the trucking landscape—Triumph differentiates itself from generic banks ill-equipped to comprehend industry-specific risk profiles or cash conversion mechanics. Their approach fosters deep client relationships grounded in expertise rather than transactional banking alone[ valye_report_excerpt ]. This tightly focused positioning underpins Triumph’s competitive advantages detailed further below.

Four Engines of Growth: Banking, Factoring, Payments, and Intelligence

Triumph segments its operations into four principal business lines that together compose its comprehensive trucking-focused financial offering.

Banking (57% of total revenue) Triumph’s wholly owned TBK Bank delivers traditional yet specialized banking services via branches concentrated mainly in Colorado’s front range, Iowa-Illinois Quad Cities region, and Dallas[ S1 ]. The bank offers deposit products generating low-cost funding complemented by commercial lending portfolios tailored to trucking-related enterprises. Notably included are equipment financing programs critical to carriers needing capital-intensive trucks as well as mortgage warehouse lending extending geographically nationwide to diversify asset composition.

These banking services produce a stable deposit base (~$4.95 billion) while mitigating balance sheet volatility through diversification beyond factoring alone. The lending portfolio ($4.99 billion) contributes complementary interest income streams aligned with client needs spanning local markets and national deployments[ F1 ][ S1 ].

Factoring (31% of total revenue) Operating as a pivotal working capital provider within the OTR sector’s cash cycle challenges, Triumph purchases trucking invoices generated by smaller fleets at a discounted rate[ valye_report_excerpt ]. This immediate purchase model alleviates carriers’ liquidity constraints where payment terms can extend 30-60 days or longer from customers.

This factoring business is highly complementary to lending since it responds to short-term operational funding timing gaps unique to freight transporters struggling against slow pay cycles. By integrating automated underwriting powered by AI technology (discussed below), Triumph expedites funding decisions while managing credit risk effectively[ valye_report_excerpt ].

Payments (11% of total revenue) The Payments segment acts as both an efficiency enabler and revenue generator by facilitating transportation invoice presentment and payment processing among Brokers, Shippers, Factors, and Carriers. It incorporates digital bank account offerings for carriers designed for ease-of-use in managing funds received from completed freight deliveries.

This platform optimizes administrative workflows that historically involved manual reconciliation prone to error or delay—further differentiating Triumph via process innovation fostering stickiness within its customer base.

Intelligence (1% of total revenue) Though smaller in scale today relative to other segments, the Intelligence business taps into proprietary datasets amassed through ongoing transactions across Triumph’s platforms. It provides data-driven insights such as pricing intelligence algorithms enabling logistics providers to benchmark rates or anticipate capacity shifts.[ valye_report_excerpt ]

While nascent compared with core banking/factoring units revenue-wise, this segment represents strategic potential leveraging big data analytics applications increasingly sought after by transportation stakeholders aiming at margin optimization.

Together these four engines form an interlocking service architecture delivering differentiated value which generalist lenders or standalone fintech players currently cannot replicate effectively.

Technology in Overdrive: AI and Automation Driving Efficiency and Scale

A critical driver underpinning Triumph's competitive position is its deployment of automated technologies bolstered by artificial intelligence throughout key processes.[ valye_report_excerpt ] In particular:

Factoring Operations: Triumph employs an instant purchase model utilizing AI-enabled credit assessment tools allowing rapid invoice buying decisions for carrier customers. This streamlines funding turnaround times substantially compared with traditional underwriting cycles customized for trucking-specific risk parameters.

Payments Platform: Scalable digital infrastructure automates invoice auditing workflows between brokers/shippers/carriers reducing frictional costs historically associated with fragmented settlement processes.

Operational Efficiency: Automation reduces manual labor intensity driving improved cost structures enabling competitive pricing flexibility while maintaining credit discipline.

By embedding AI into multiple facets—from risk models assessing fleet reliability or broker payment history to optimizing loan syndication—Triumph reduces human review bottlenecks without sacrificing underwriting quality or compliance adherence.[ valye_report_excerpt ][ S1 ] This technological backbone empowers scale economies absent among smaller players limiting their growth runway.

Consequently technology adoption not only elevates client experience through accelerated service delivery but also fortifies defensive moats surrounding relationship longevity given integrated operational dependencies shaped over time.

Financial Performance on the Dashboard: Latest Results and Metrics

Triumph has demonstrated solid operational execution reflected in financial results for calendar year 2025. Key highlights include:

Asset Base Expansion: Total consolidated assets reached approximately $6.38 billion at December 31, 2025 reflecting growth across banking loans ($4.99 billion) balanced with stable deposit inflows nearing $4.95 billion capturing client liquidity surpluses aligned with operating expansions.[ F1 ]

Profitability: Net income stood at roughly $25 million for the full year evidencing profitable scaling amid ongoing investments supporting payments and intelligence growth initiatives.[ F1 ]

Revenue Mix: Banking remains dominant accounting for 57% of segment revenues spotlighting consistent income stability; factoring contributed nearly one-third (31%) underscoring importance as a working capital engine; Payments at 11% confirm traction gains; Intelligence remains a small but growing contributor (1%).[ S1 ]

Earnings Beats: Notably Q4 2025 earnings surpassed analyst estimates reporting both top-line revenue beats alongside improved net interest margins attributed partly to higher yields on specialized loans as well as expense control efficiencies amid automated operations.[ N2 ][ N1 ]

This financial dashboard aligns cohesively with management commentary emphasizing disciplined credit risk management supporting asset quality while selectively expanding footprint via branches primarily servicing key regional markets[ N1 ].

The stable deposit base combined with diversified loan portfolio including equipment financing insulates against single-product volatility prevalent among pure factoring companies.[ S1 ][ F1 ] Together these metrics paint a robust picture underpinning affirmation of strategic direction leveraging integrated product mix.

Moat Mechanics: What Defends Triumph’s Turf?

Triumph’s competitive edge derives from holistic integration—the company is not simply a bank nor merely a factoring provider but combines multiple specialized services addressing trucking ecosystem intricacies under one roof.[ valye_report_excerpt ] This integration creates several moat drivers:

Industry Specialization: Deep domain expertise across Brokers, Shippers, Factors, and Carriers allows tailoring of underwriting criteria aligned with unique cash cycle risks not well understood outside niche specialists.

Comprehensive Product Suite: Offering deposits/lending plus factoring embedded with payments processing plus intelligence affords one-stop-shop convenience increasing switching costs for clients seeking seamless finance workflow support.

Proprietary Technology: Custom-developed AI-driven automation streamlines decision-making enhancing speed rare among banks/fintechs limited individually in scope or scale.

Scale & Client Base: Substantial assets ($6+ billion) enable offer competitive yields while spreading fixed costs across large volumes especially within factoring where scale improves loss mitigation capabilities.

Together these factors strengthen barriers preventing new entrants or generalist competitors from encroaching easily without replicating entire integrated platform—a challenging feat both technologically and relationship-wise fostering durable customer loyalty.[ valye_report_excerpt ]

The Risks Lurking Down the Highway

Concentration risk looms largest—Triumph’s fortunes correlate closely with cyclical performance of the US trucking industry exposed to macroeconomic shifts impacting freight volumes such as fuel price volatility or trade policy fluctuations.[ S1 ][ valye_report_excerpt ]

Additional systemic risks include:

Credit Risk: Exposure primarily concentrated in small/mid-tier carriers who may be vulnerable during downturns leading to elevated charge-offs affecting earnings stability.[ S1 ]

Regulatory Environment: Banking regulations evolving around capital adequacy plus emerging frameworks targeting fintech-related payments or AI usage may impose compliance costs or restrict operational flexibility.[ S1 ]

Technology & Cybersecurity Threats: Increasing reliance on digital platforms introduces heightened cyber risk requiring continual investment to prevent breaches potentially disrupting payment flows or compromising sensitive data.[ S1 ]

Integration Risks: Growth through acquisitions entails execution challenges merging systems/cultures potentially diluting focus.[ S1 ]

Management openly acknowledges these perils noting necessity for vigilant risk management frameworks adapting dynamically given uncertainties inherent in transportation sector funding markets.[ S1 ][ N1 ] Such transparency tempers overly optimistic narratives reinforcing need for balanced assessment weighing both strengths and vulnerabilities.

Growth Pit Stops: Acquisitions and Market Expansion Strategies

Since inception of its banking operations in 2010,[ S1 ] Triumph has tactically expanded its branch network via both organic growth initiatives supplemented by targeted acquisitions particularly within strategic regional hubs like Colorado’s front range area plus Quad Cities region embracing Iowa/Illinois markets.

These expansions enable deeper local market penetration fostering incremental deposit gathering feeding loan growth including newer product lines such as mortgage warehouse lending providing asset diversification nationwide.[ S1 ] Meanwhile efforts expanding non-lending segments including Payments aim at cross-selling opportunities attaching higher-margin fee businesses anchored on existing transactional volumes from primary customers.[ S1 ]

Collectively these approaches demonstrate measured scaling balancing geographic diversity benefits without diluting core specialization philosophy intact centered on OTR trucking ecosystem participants.

Looking Ahead: Industry Tailwinds and Potential Roadblocks

Macroeconomic trends steering US freight demand influence Triumph’s trajectory significantly – robust ecommerce growth coupled with supply chain resilience investments bode well for sustained volume requiring financing support thereby underpinning runway expansion potential[ N1 ]. Moreover digitization trends among logistics operators accelerate adoption of fintech-enabled payments/intelligence solutions increasing addressable market size.

Conversely evolving regulatory landscapes encompassing banking oversight modernization alongside emerging AI governance frameworks could inject compliance hurdles rationing capital deployment agility,[ S1 ] while intensifying competition from larger fintech conglomerates or diversified lenders might pressure pricing power necessitating continual innovation investments.

Furthermore anticipated fluctuations in fuel costs or economic slowdowns present risks of demand shocks directly impacting carrier balance sheet health thus constraining factoring/loan repayment profiles requiring vigilance over credit portfolio concentrations amidst tightening monetary conditions common post-pandemic era.[ N1 ][ S1 ]

Ultimately Triumph’s integrated business model equipped with proprietary technology paired against sound risk management sets foundational strengths facing forward albeit conditioned upon navigating external headwinds carefully balanced against opportunity-rich industry tailwinds.[ valye_report_excerpt ][ N1 ][ S1 ]

This analysis synthesizes publicly available registrations filed up through February 2026 alongside recent earnings disclosures to provide an empirically grounded perspective on Triumph Financial’s positioning within the US trucking finance niche. It reflects neither investment advice nor price forecasts but aims to elucidate strategic dynamics shaping this specialized financial services company’s current state and near-term outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments