Perfect Moment Ltd.: Balancing a 51% Sales Surge with Lingering Financial Fragility

Despite an impressive quarterly sales growth, Perfect Moment Ltd. faces substantial risks from tight liquidity and concentrated manufacturing.

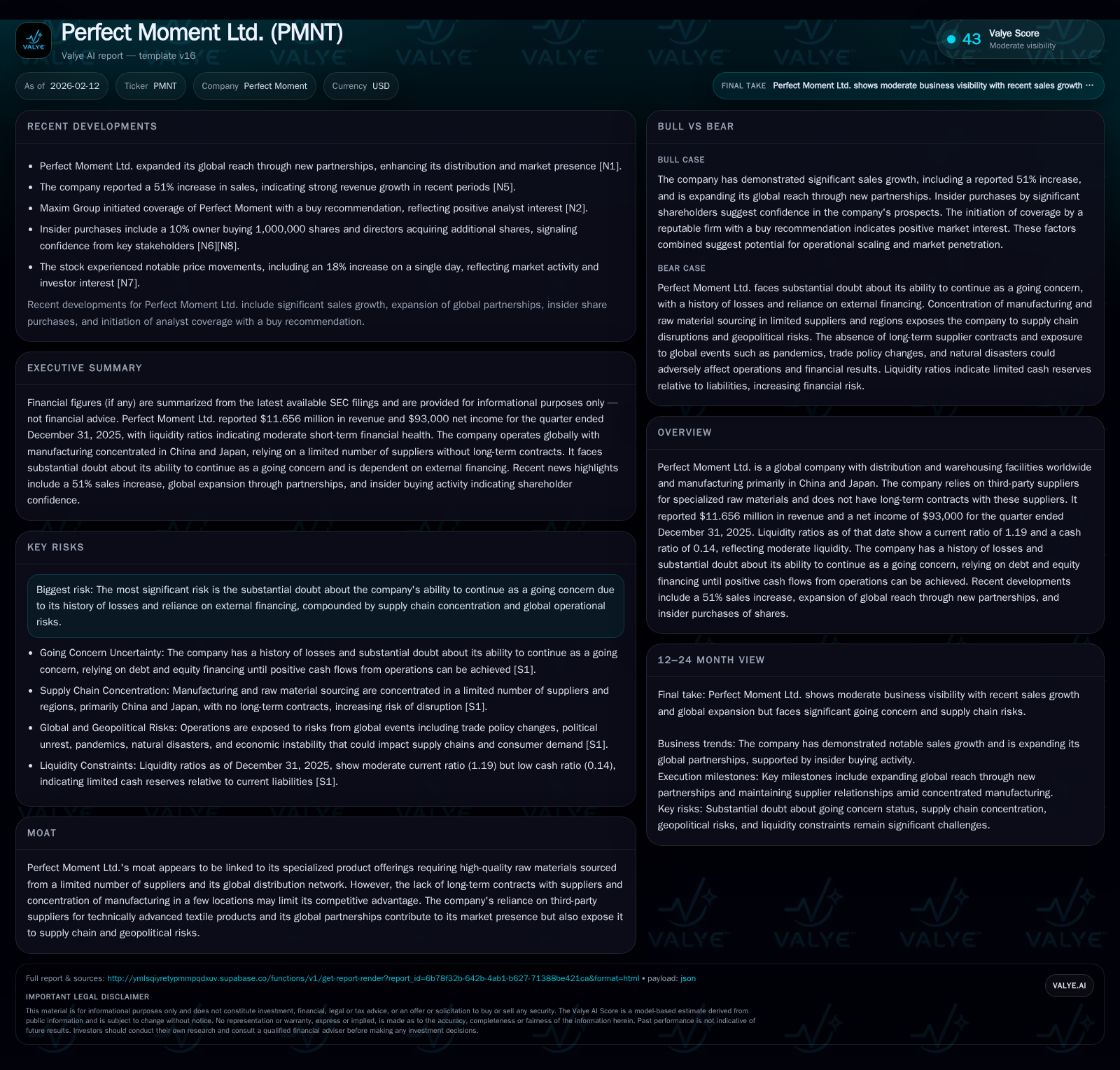

Perfect Moment Ltd. reported a remarkable 51% increase in sales for the quarter ended December 31, 2025, reaching $11.7 million in revenue, but net income gains remain modest at $93,000, underscoring persistent profitability challenges. The company’s liquidity profile reflects moderate cushion with a current ratio of 1.19 and a low cash ratio of 0.14 amid ongoing reliance on external financing. Its expanding global partnerships offer new market reach; however, they also intensify exposure to geopolitical and operational complexities. Concentration of manufacturing in China and Japan combined with dependence on third-party suppliers without long-term contracts further heighten supply chain vulnerabilities. Finally, the auditor’s ‘substantial doubt’ regarding going concern status accentuates existential risk despite insider purchases signaling some internal confidence.

Surging Sales amid Lingering Doubts: The Latest Quarter in Focus

Perfect Moment Ltd.’s latest quarter starkly illustrates the tension pulsing through its business trajectory. A headline-grabbing 51% surge in sales thrust revenues up to $11.656 million for the period ending December 31, 2025 — a meaningful jump after years marked largely by losses [N1][F1]. However, this growth story softens upon scrutiny of profitability: net income barely nudged to $93,000, reflecting thin margins or elevated costs that continue to compress earnings power [F1]. This paradox—of top-line momentum barely translating into bottom-line strength—sets the stage for a nuanced evaluation of operational efficacy versus underlying vulnerabilities.

While the sales jump signals market acceptance or improved execution possibly tied to recent global partnerships [N1], it also poses questions on scalability and sustainable profit conversion under existing cost structures.

The Tightrope of Liquidity: Unpacking PMNT’s Financial Health

A snapshot of Perfect Moment’s liquidity reveals precarious footing framed by mixed signals. The company carries $13.25 million in current assets against $11.13 million in current liabilities, generating a current ratio of 1.19, suggesting just enough short-term asset coverage for obligations [F1]. Yet this surface adequacy masks a strikingly low cash ratio of approximately 0.14, with only around $1.57 million in cash equivalents available [F1].

Such constrained immediate liquidity heightens existential risk amid fixed near-term commitments and operating cash flow uncertainty. It dovetails with disclosures cautioning that while current financing arrangements support operations over the coming year at present assumptions, unforeseen shifts or accelerated capital needs could force early fundraising — whose timing and terms remain uncertain [S2].

This delicate balancing act positions liquidity as both buffer and bottleneck, shaping Perfect Moment’s strategic flexibility and operational resilience.

Global Partnerships as a Double-Edged Sword

Expansion into new international markets via recently announced global partnerships has undeniably enhanced Perfect Moment’s distribution footprint and potential customer base [N1]. These alliances reflect strategic ambition to leverage localized expertise and scale beyond core existing geographies.

However, each step into foreign markets embeds additional complexity: navigating divergent regulatory environments, currency volatility, customs logistics, and political instability risks [S2]. Furthermore, integrating partners’ operational standards and safeguarding supply chain coherence introduces friction points that could adversely affect service consistency or cost structures.

Thus, while these relationships open promising avenues for revenue augmentation, they simultaneously elevate the company's exposure to global economic shocks and geopolitical upheavals.

Supply Chain Dependencies: Strength or Achilles’ Heel?

Perfect Moment’s reliance on third-party suppliers for highly specialized raw materials without binding long-term contracts emerges as a critical vulnerability [valye_report_excerpt][S2]. This supplier dependency concentrates risk on external providers whose availability can fluctuate due to their own capacity constraints or external events.

The lack of contractual safeguards exposes the company to sudden supply shortages or price inflation — scenarios that become particularly perilous given Perfect Moment’s niche product requirements demanding high technical quality input materials.

In an environment where supply chains are under constant strain from geopolitical tensions or logistic bottlenecks, such non-committed arrangements resemble an Achilles’ heel capable of disrupting production schedules or forcing costly last-minute sourcing alternatives.

Decoding the ‘Going Concern’ Warning: What It Means for Investors

One of the starkest cautions comes in the form of an auditor-issued ‘going concern’ explanatory paragraph, explicitly stating “substantial doubt about our ability to continue as a going concern” due to ongoing losses and dependence on external financing [S2][valye_report_excerpt].

For investors unfamiliar with accounting parlance, this term signals that auditors question whether the company can meet its obligations over the next year without significant changes in capital structure or operational strategy—essentially flagging existential financial risk.

While Perfect Moment believes current cash flows combined with financing will suffice near term, this outlook hinges on optimistic assumptions vulnerable to rapid deterioration should market conditions shift unfavorably or operational hurdles emerge.

Recognizing this qualification is crucial; failure to surmount these risks could lead to severe consequences including insolvency or equity value impairment.

Insider Moves: Insider Share Purchases as a Signal?

Amidst cautionary tales lies an intriguing counterpoint: insiders have engaged in recent share purchases [valye_report_excerpt]. Such activity often signals management’s confidence—or at least willingness—to demonstrate commitment during volatile times.

While insider buying cannot dispel structural challenges outright, it adds color about internal sentiment that might portend either belief in near-term turnaround prospects or alignment with shareholder interests under pressure.

These transactions warrant monitoring as a nuanced barometer of how those closest to Perfect Moment perceive its trajectory against documented risks.

Manufacturing Footprint Risks: China and Japan Concentration

Perfect Moment's manufacturing predominantly situated in China and Japan offers advantages linked to established industrial ecosystems and cost controls but simultaneously encumbers operations with geopolitical susceptibility [valye_report_excerpt][S2].

Tensions affecting trade policies, tariffs, or regional conflicts could rapidly escalate costs or disrupt production timelines for facilities concentrated within these areas.

Moreover, any outbreak of events such as labor unrest, natural disasters, or regulatory crackdowns would disproportionately impair Perfect Moment compared to firms diversified across wider geographies.

This dual-edged nature necessitates careful mitigation plans yet remains an intrinsic source of operational hazard difficult to overlook.

Future Financing Imperatives: Navigating Capital Needs and Market Realities

Given persistent undercapitalization relative to growth ambitions, Perfect Moment openly acknowledges probable future needs for additional financing, whether via debt issuance, equity raises, or alternate funding sources [S2].

Such fundraising cycles could impose dilution pressures on shareholders while diverting executive bandwidth toward capital markets rather than core business development—a classic bind for companies straddling early-stage growth amid fragile financial footing.

Moreover, external market conditions will critically influence terms availability; difficult credit environments or investor wariness stemming from going concern warnings may exacerbate funding challenges further.

This dynamic underscores how securing sufficient capital at reasonable terms constitutes a linchpin determinant for Perfect Moment's viability beyond the short term.

PMNT’s Moat: Specialized Products in a Fragile Ecosystem

In examining competitive edges, Perfect Moment’s asserted moat derives from its specialized product portfolio requiring high-quality technical inputs sourced from limited suppliers combined with an extensive global distribution network [valye_report_excerpt].

On one hand, this specialization fosters brand differentiation difficult for generic competitors to replicate quickly—potentially affording pricing power within niche segments.

On the other hand, absence of supplier contracts plus manufacturing concentration weakens defensibility by exposing product pipelines to external shocks. The global network bolsters customer access yet simultaneously demands robust coordination across regions subject to variable operational climates.

Hence, while intangible assets exist within its ecosystem positioning, they possess inherent fragility threatening sustained advantage if underlying risks materialize without mitigation.

Wrapping Up: Growth Potential Vs. Structural Risk

Perfect Moment Ltd.’s narrative brims with contradictions emblematic of ambitious small-cap enterprises seeking breakthrough trajectories through bold expansion amid multifaceted headwinds. The 51% surge in sales marks undeniable progress, reflecting effective commercial initiatives particularly via new global partnerships.

Yet beneath this surface triumph lies enduring fragility: tight liquidity constraints paired with modest profitability gains; critical manufacturing concentration imperiling supply continuity; absence of supplier contract security amplifying disruption risk; all compounded by an auditor-issued going concern warning that colors future uncertainties of survival itself.

Insider buying gestures hint at pockets of internal faith but cannot fully offset these systemic pressures requiring astute capital management and strategic flexibility ahead. Stakeholders therefore face a complex interplay between encouraging signals of growth momentum contrasted sharply against structural vulnerabilities demanding vigilant oversight moving forward.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available data as of February 12, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments