Corebridge Financial’s 2025: Navigating towering revenues amid persistent losses

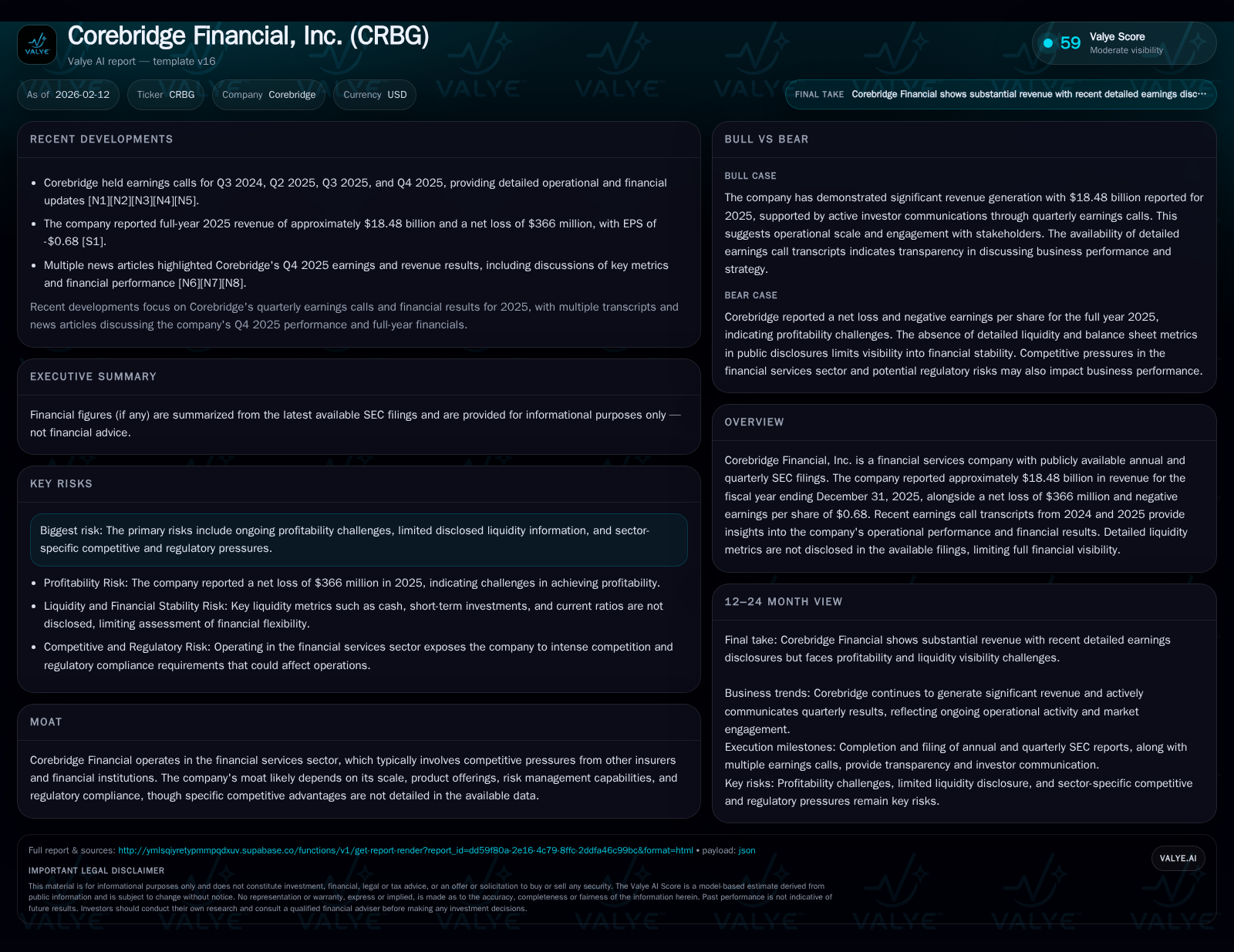

Corebridge Financial posted robust $18.48 billion revenue in 2025 yet wrestled with a near-$366 million net loss, raising strategic questions.

Corebridge Financial’s fiscal year 2025 reflected the tension between strong top-line performance and ongoing profitability challenges. Despite generating sizable revenue, the company reported a net loss of $366 million and negative EPS of $0.68, suggesting structural or operational headwinds. Management commentary from Q4 earnings calls sheds light on cost controls and risk management amid sector pressures, while limited liquidity disclosures cast shadows over full financial clarity. The firm faces intense regulatory and competitive dynamics requiring agile navigation to restore sustainable profits.

Corebridge’s 2025 Revenue Strength vs. Profitability Challenge

In the sprawling landscape of financial services, Corebridge Financial mounted an impressive topline of $18.48 billion in revenues for fiscal 2025. This figure alone paints a picture of a company commanding significant market footprint and business activity [F1]. However, the sheen dims when juxtaposed against a net loss tallying $366 million and an EPS in the red at -$0.68 — stark reminders that scale is no antidote to profitability woes. This juxtaposition sketches an immediate narrative tension: why does such revenue heft fail to translate into bottom-line gains?

Delving into SEC filings outlines likely culprits tucked beneath headline numbers — operational inefficiencies, elevated costs, or adverse investment outcomes within insurance reserves could be factors dampening income streams [S1]. The sizable revenue base suggests healthy sales or premium intake, but equally signals substantial outflows or expense accruals offsetting gains.

This duality underscores a balancing act: preserving growth engines while tightening leaky profitability seams remains a pressing challenge for Corebridge.

Dissecting the Q4 2025 Earnings Calls: Management’s Perspective on Performance

Management’s voices from Q4 2025 earnings calls frame this tension with revealing candor [N1][N2][N6][N7]. They emphasize revenue drivers rooted in diversified financial products yet concede subdued profit margins owing to cost pressures and macroeconomic volatility. Notably, executives highlighted initiatives targeting expense control without sacrificing customer acquisition momentum.

A key theme threading these discussions was risk management vigilance — a critical hedge given fluctuating market conditions impacting investment portfolios integral to insurer economics. Statements like "we remain focused on disciplined underwriting and recalibrating our portfolio strategies" convey a proactive mindset countering uncertainty.

Yet the tone also hinted at ongoing structural adjustments required for sustainable turnaround, signaling that the road ahead involves more than short-term fixes.

Moat Under the Microscope: Scale and Risk Management Capabilities

While explicit competitive moats are not enumerated in public disclosures, analysis infers Corebridge’s positioning rests on its sizable scale, diverse product catalog, and embedded risk management framework [S1][valye_report_excerpt.moat]. In an industry saturated with insurers jockeying for favorable contract terms and capital efficiency, these traits matter.

Scale can afford economies of scope and pricing power; however, without unique product innovation or technological edge disclosed, differentiation appears modest relative to peers. Moreover, rigorous risk controls are vital in managing underwriting losses or investment volatility — qualities underscored repeatedly by leadership but challenging to quantify externally.

This suggests Corebridge’s moat is evolutionary rather than entrenched— dependent on continuous enhancement of internal capabilities amidst fierce competition.

Liquidity Shadows: Implications of Limited Disclosure

One thorny facet emerging from filings is the scarcity of comprehensive liquidity metrics [S1][S2][valye_report_excerpt.risks]. This opacity injects uncertainty into evaluating Corebridge's maneuvering room during adverse market swings or investment shocks.

Liquidity represents the lifeblood enabling an insurer-financial firm to meet obligations promptly while pursuing growth investments. Partial transparency restricts analysts’ ability to build robust risk profiles or stress test scenarios — especially crucial given recent earnings showed losses despite sizeable revenues.

In this foggy terrain, investors may apply wider risk premiums or discount valuations pending clearer disclosures that affirm capital adequacy and funding stability under varied cycles.

Sector Pressures: Regulatory and Competitive Landscape Impact

Operating within financial services subjects Corebridge to labyrinthine regulatory webs governing capital reserves, underwriting practices, consumer protections, and transparency mandates [valye_report_excerpt.risks]. Such frameworks continuously evolve post-financial crises worldwide to bolster systemic resilience but often constrain profit levers through compliance costs.

Simultaneously, competition fixes razor-thin margins as traditional insurers contend with newcomers leveraging technology-driven efficiencies or alternative capital sources. For Corebridge, these external forces manifest as persistent profitability headwinds requiring nimble responses — not only preserving regulatory good standing but innovating to capture emerging niches faster than rivals.

Consequently, these dual pressures compound challenges already evident from internal performance metrics.

Risks and Opportunities Embedded in Recent Financial Trends

The intersection of declining earnings despite strong revenues spotlights core risks: structural cost burdens, exposure to market volatilities affecting invested assets backing policies, and possibly slower-than-expected integration or scaling of new business lines [S1][N10][N12]. These risks have tangible implications for stock trajectory as analysts temper estimates accordingly.

Yet embedded alongside risks are latent opportunities. Management’s commentary on recalibrating portfolios, enhancing underwriting rigor, and cost rationalization programs indicate deliberate corrective paths unfolding. Should these take hold effectively, Corebridge could pivot toward healthier margin profiles without sacrificing growth vectors.

Thus recent financial trends depict a battleground where prudent strategy execution could unlock value suppressed by legacy inefficiencies.

Investor Sentiment and Analyst Expectations Ahead of Q1 2026

Market sentiment percolates cautiously around Corebridge heading into Q1 2026 earnings announcements [N10][N12][N14]. Analysts highlight expectations for continued pressure on profit figures but watch closely for inflection signs driven by operational improvements or macroeconomic tailwinds.

Options market activity corroborates a guarded stance — reflecting uncertainty yet positioning for potential volatility swings depending on forthcoming disclosures or guidance adjustment.

This environment demands that Corebridge sustain transparent communication channels accentuating progress milestones to rebuild investor confidence progressively rather than abruptly.

Strategic Outlook: Pathways to Restoring Profitability

Synthesizing these threads frames several strategic imperatives Corebridge appears embracing or might consider accelerating [N1][S1]. Foremost is amplifying operational efficiency — streamlining redundant processes while deploying technology for claim adjudication and customer engagement improvements offers margin expansion potential.

Product innovation aligned with shifting demographic needs or emerging retirement planning trends could fortify revenue resilience alongside tighter risk quantification enhancing underwriting precision. Furthermore, judicious capital management— balancing debt leverage with liquidity cushions—remains essential given opaque liquidity markers observed.

Ultimately, profitability restoration emerges as a multifaceted navigation demanding calibrated balance between growth aspiration and disciplined expense governance underpinned by transparent stakeholder engagement.

This report assembles publicly available data as of February 12, 2026. It embodies analytical insight without providing investment recommendations or forecasts. Readers should consider supplementary sources when forming judgments regarding Corebridge Financial's future prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments