Tyra Biosciences Faces Intensifying Losses Despite Strong Liquidity Position

Tyra Biosciences shows widening net losses alongside a robust liquidity posture and new leadership, underpinning cautious market optimism.

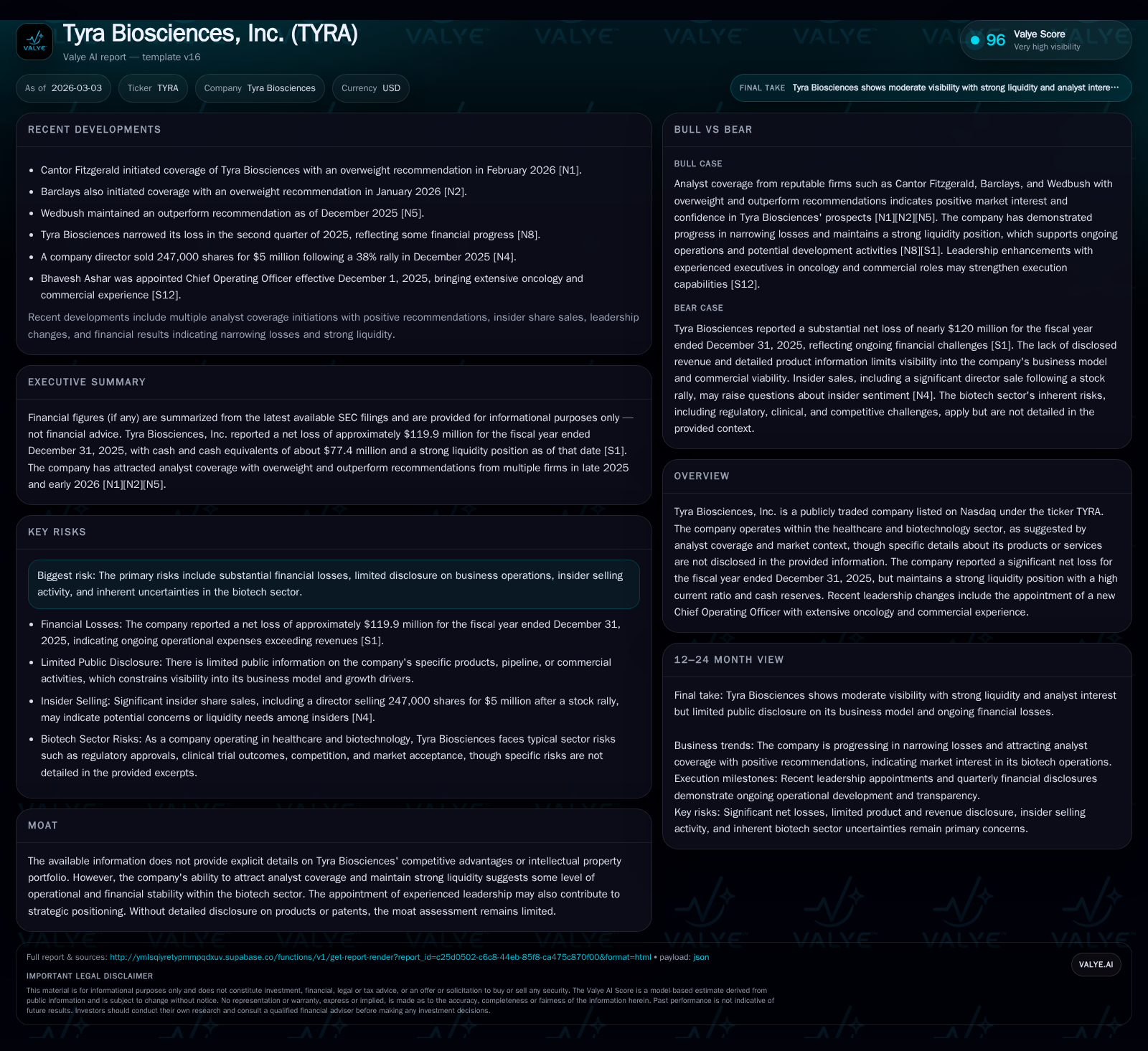

Tyra Biosciences has recorded sharply increasing net losses over recent years, culminating in a net loss of $119.9 million in 2025, reflecting an intensification of operating expenses largely linked to clinical development expansion. Despite these financial pressures, the company retains a strong liquidity position with a current ratio around 14.7 and cash reserves exceeding $77 million, cushioning operational flexibility. Recent management changes, including the appointment of an oncology-experienced COO, signal an emphasis on optimizing execution and commercial readiness. Analyst coverage beginning in early 2026 with overweight ratings indicates growing investor interest keyed to pipeline developments, especially the progressing Phase 2 clinical trial for dabogratinib in pediatric achondroplasia.

Escalating Losses Against a Strong Liquidity Backdrop

Tyra Biosciences has exhibited a pronounced increase in operating and net losses over the past four years. Operating income worsened from -$58.9 million in FY2022 to -$132.8 million in FY2025, marking a compound deterioration with a -27.4% year-over-year change from FY2024 to FY2025 [F1]. Correspondingly, net income declined by nearly 39% over the same interval, reaching -$119.9 million at the end of 2025 [F1]. This trend reflects an aggressive scaling of operational activities without offsetting revenue generation.

Despite these escalating losses, Tyra’s liquidity position remains robust. The company reported cash and equivalents totaling approximately $77.4 million and current assets of $265.5 million against current liabilities of just $18.1 million as of December 31, 2025 [F1], resulting in an exceptional current ratio of about 14.7 [F1]. This ample cushion provides a significant buffer against funding risks typically faced by pre-commercial biotech firms executing costly clinical programs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -120 | -95 | -133 | 141000 | -38.7% |

| 2024 | -86 | -70 | -104 | 664000 | -25.1% |

| 2023 | -69 | -50 | -80 | 770000 | -25.0% |

| 2022 | -55 | -50 | -59 | 559000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -95 | -46.3 |

| 2024 | -70 | -25.2 |

| 2023 | -51 | -33.8 |

| 2022 | -51 | -21.5 |

Source: SEC companyfacts cache [F1].

Operational Drivers Behind Recent Financial Trends

The rapid increase in operating expenses correlates strongly with expanding research and development activities centered around clinical programs such as the BEACH301 study investigating dabogratinib for pediatric achondroplasia [S15]. The initiation of dosing for the first child participant marked a key milestone that corresponded with elevated trial-related costs including patient monitoring and third-party services.

Moreover, Tyra relies extensively on contract manufacturing organizations (CMOs) for drug production and various preclinical research functions [S11]. This reliance on external providers introduces cost variability and supply chain risks but is common among emerging biotechs focusing limited internal resources on discovery while outsourcing later-stage development functions.

Impact of Leadership Enhancements on Strategic Direction

In December 2025, Tyra appointed Bhavesh Ashar as Chief Operating Officer bringing two decades of oncology-focused commercial expertise from senior roles at SpringWorks Therapeutics, Bayer Oncology and Sanofi Genzyme [S22]. Ashar's background positions him well to refine commercial strategies and enhance operational alignment ahead of potential product launches.

His joining signifies an intent by Tyra’s board to strengthen execution capabilities bridging scientific progress with market readiness—an important pivot commonly observed when biotech firms transition from discovery toward commercialization phases.

Development Pipeline Focus: Dabogratinib Clinical Progress

Tyra’s leading pipeline candidate dabogratinib (formerly TYRA-300) entered its Phase 2 BEACH301 study targeting children with achondroplasia in mid-2025 [S15]. This trial's dosing initiation was publicly announced with the first pediatric patient treated emphasizing progress beyond adult-focused indications.

Crucially, Tyra expects safety data from the sentinel cohort by the second half of 2026 [S15; N1], which will be an important inflection point providing initial human tolerability metrics essential for regulatory engagement and further dose escalation decisions.

Analyst Coverage Initiations and Market Sentiment Signals

Early 2026 saw Barclays and Cantor Fitzgerald commence coverage on Tyra Biosciences issuing overweight recommendations [N1; N2]. These ratings reflect analyst confidence anchored on pipeline momentum coupled with fresh leadership strengthening execution prospects despite ongoing losses.

Market responses are consistent with biopharma investing norms where developmental catalysts frequently overshadow short-term financial headwinds until pivotal data readouts either validate or reset expectations.

Capital Structure and Cash Flow Dynamics

Reviewing capital deployment confirms Tyra's profile as an early-stage biotech prioritizing innovation investment over capital expenditures or shareholder returns. Operating cash flows remained deeply negative at approximately -$95.1 million for FY2025 representing a -36.4% year-over-year decline versus FY2024 [F1]. Meanwhile capital expenditures were immaterial at just $141 thousand consistent with minimal investment in fixed assets [F1].

No dividends or share repurchases were reported during this period [S9; S19; S20], aligning with typical sector behavior where scarce capital is directed toward R&D rather than distributions.

Equity stood at $259 million at year-end reflecting prior financing rounds that maintain sufficient runway though equity dilution remains a future consideration [F1]. The approximate return on equity was negative ~46% due to ongoing losses [F1].

Forward-Looking Considerations and Milestones to Track

Critical forthcoming events include anticipated initial safety data from the BEACH301 sentinel cohort expected H2 2026 [S15]. This dataset will provide early insight into dabogratinib’s therapeutic window in children—a key regulatory prerequisite given pediatric patient sensitivities.

While explicit FDA guidance timelines remain undisclosed subsequent regulatory engagements post-sentinel data will guide trial progression or necessary protocol adaptations [S15]. Investors should also observe how new leadership delivers against operational milestones influencing market sentiment.

Any future clinical advancements or partnerships emerging from these developments could materially alter Tyra's valuation dynamics—though caution is warranted due to inherent biotech volatility.

Navigating Biotech Industry Risks Unique to Tyra

Operational risks encompass dependency on single-asset pipeline concentration—dabogratinib being critical—and third-party suppliers whose performance affects timelines [S11]. Regulatory uncertainties prevalent across biotech add layers of unpredictability around trial outcomes and approval pathways [S4; S5; S6; S7; S15]. Insider selling activity noted raises potential governance or confidence questions that warrant monitoring.

These factors compound typical 'black swan' risks intrinsic to innovative therapeutics development where scientific promise coexists uneasily alongside technical execution challenges.

This analysis is based solely on publicly filed SEC documents and recent news reports through March 3, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments