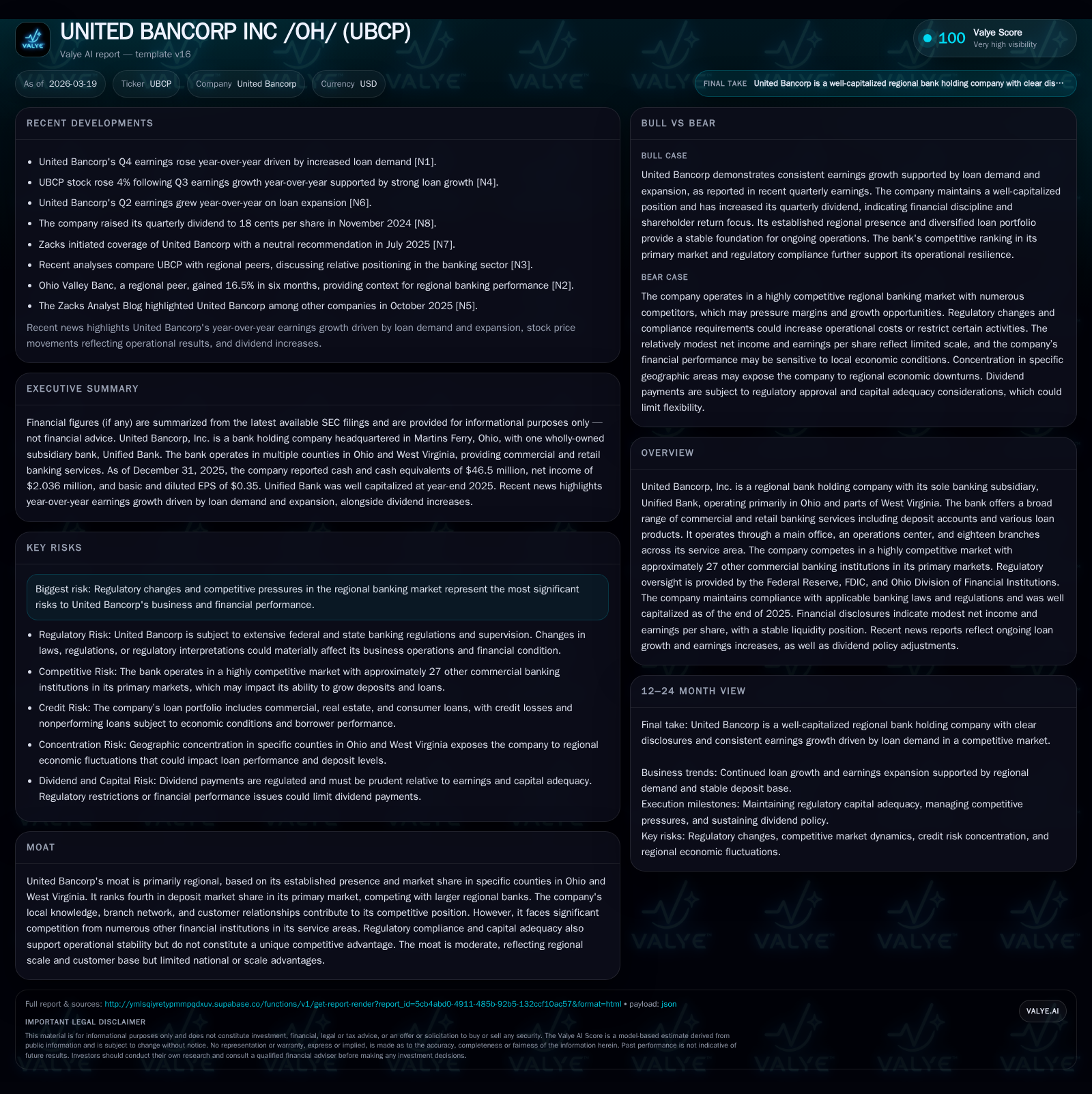

United Bancorp’s Steady Regional Positioning and Capital Management Shape Modest Growth Outlook

United Bancorp leverages a solid regional deposit base and prudent capital strategies to sustain earnings amid intense competition.

UNITED BANCORP INC /OH/ (UBCP) operates primarily in Ohio and parts of West Virginia through its sole banking subsidiary, Unified Bank. Despite operating in competitive markets with over two dozen banks, United Bancorp maintains a respectable fourth-place deposit market share in Belmont County, supported by its branch network and strong local customer ties. Its financial performance over recent years has shown modest net income growth driven by steady commercial loan demand but tempered by competitive pressures and regulatory constraints. Capital adequacy remains sound, supporting dividend payouts and limited share repurchases, though free cash flow is currently negative due to elevated capex. Looking ahead, growth is likely capped by market competition and regulatory limits, with close attention warranted on loan portfolio quality and liquidity conditions.

Company Overview and Market Position

United Bancorp, Inc., headquartered in Martins Ferry, Ohio, operates solely through its banking subsidiary Unified Bank. The bank serves customers across northeastern to southeastern Ohio counties such as Belmont, Harrison, Jefferson, Tuscarawas, Carroll, Athens, Hocking, Fairfield, as well as northern panhandle areas of West Virginia [S1][S7]. Its operational footprint includes a main office and eighteen branches distributed strategically within these regions. The bank offers typical commercial and retail banking services including demand deposits, savings accounts, time deposits, commercial lending, real estate financing, and consumer loans.

Competition is notably intense; the primary market of Belmont County alone includes approximately 27 other commercial banks [S1][S15]. United Bancorp holds the fourth-largest deposit market share there after dominant players like Huntington National Bank and PNC Bank. This ranking underscores its established regional presence but also delineates constraints from larger institutions’ scale advantages.

Historical Financial Performance

Financially, United Bancorp has demonstrated stable yet modest profitability over the past several years. Net income for fiscal year (FY) 2025 stood at approximately $2.04 million representing about a 10% increase from FY2024's $1.85 million [F1]. This jump was primarily supported by increased demand for loans reported in Q4 earnings press coverage [N1], alongside stable net interest margins sustained around the low-to-mid single digits based on SEC disclosures [S17][S26].

Operating cash flows (CFO) showed an even stronger rise — moving from $8.45 million in FY2024 to over $10.45 million in FY2025 (+23.8%) [F1]. However, capital expenditures also surged significantly from under $10 million to almost $11.8 million over the same period (+21.5%), mostly reflecting investments into branch infrastructure upgrades and IT systems modernization as noted indirectly via management discussion sections [S1][S4]. The net effect was a negative free cash flow (CFO minus CapEx) position near -$1.32 million for FY2025 — signaling reinvestment prioritization over cash generation currently.

Equity expanded steadily from approximately $63.5 million at end-FY2023 to $70.5 million at end-FY2025 [F1]. This growth alongside modest profit levels yields a roughly calculated ROE near 2.9%, indicating relatively conservative profitability metrics given regional mid-sized banking peers often target mid-to-high single digit returns on equity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 2 | 10 | 12 | +10.1% |

| 2024 | 2 | 8 | 10 | -22.6% |

| 2023 | 2 | 9 | 1 | +3.6% |

| 2022 | 2 | 8 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 5 | 317000 | -1 |

| 2024 | 5 | 687000 | -1 |

| 2023 | 5 | 733000 | 8 |

| 2022 | 5 | 767000 | 8 |

Source: SEC companyfacts cache [F1].

Table: Key Financial Metrics for United Bancorp FY2023–FY2025 [F1]

Loan Portfolio Composition and Credit Quality

The bank’s loan portfolio is concentrated moderately across several key segments with roughly equal exposure to first lien residential mortgages (18%), owner-occupied non-farm/non-residential real estate (19%), commercial & industrial loans (19%), plus other non-farm real estate (19%) [S11][S27]. This diversified loan mix mitigates sector-specific risk while aligning with typical community banking models.

Allowance for credit losses remained adequate relative to total loans both in absolute terms (0.87% of loans) and when compared to nonperforming loans; nonaccrual loans constituted less than half a percent of total loans [S18]. Net charge-offs historically have been minimal across all categories though consumer installment loans experience slightly higher loss rates (1-2%) typical for unsecured segments.

Regulatory Environment & Compliance

United Bancorp operates under stringent regulatory scrutiny from multiple agencies—the Federal Reserve Board supervises the holding company while the FDIC and Ohio Division of Financial Institutions oversee the banking subsidiary [S1][S15]. The bank complies with Basel III capital adequacy standards since their implementation in prior years with clear evidence that it remains well-capitalized as of year-end FY2025 [S9].

Ohio state laws additionally constrain dividend payouts relative to profits retained or accumulated earnings requiring board prudence in distribution decisions [S13]. The bank adheres closely to Federal Reserve supervisory guidance on dividends and share repurchases balancing shareholder returns against capital preservation [S4].

Capital Allocation and Returns

United Bancorp has returned capital steadily through quarterly dividends along with occasional special dividends confirmed by recent announcements early in Q1 of calendar year 2026 [N1][S3]. Dividend payments rose modestly year-over-year reaching about $5.48 million total disbursed during FY2025 [F1]. Share repurchases have taken place but remain subdued below $400k annually recently.

Though net income increased slightly this past year supporting payout stability, the measured return on equity implies room for improved operational efficiency or higher risk-adjusted yields before delivering sizable shareholder value uplift [F1]. Elevated capex investment reduces free cash available for distributions temporarily but aims at fortifying operational platforms long term.

Future Growth Prospects and Constraints

Looking forward into fiscal years beyond FY2025:

- Continued loan growth momentum driven primarily by local business demand could support improved net interest income though competitive pressures may cap achievable margins given multiple similar-sized players competing locally including nationally known banks like Huntington or PNC [N1][S15].

- Deposit base retention appears solid given fourth-place market rank but expanding share would require notable product differentiation or expansion into underserved adjacent geographies within Ohio-West Virginia corridor.

- Regulatory capital requirements remain binding constraints limiting aggressive expansions without proportional equity raises or retained earnings accumulation [S9][S13].

- Further investments into technology or branch modernization might be needed but will pressure free cash flows short term.

- Loan portfolio quality should be monitored closely especially consumer installment segments which exhibit relatively higher charge-offs amid evolving economic conditions locally.

No explicit future financial guidance has been provided publicly beyond dividend declarations issued early in calendar year 2026 [N1][S3], therefore financial milestones must be observed through forthcoming quarterly filings ([S2], periodic Form10-Q).

Conclusion

United Bancorp occupies a solid regional niche within northeastern Ohio’s banking landscape backed by an entrenched branch network and moderate deposit market share rankings despite fierce local competition. Its historical financials reflect steady yet unspectacular profit generation constrained by cautious capital allocation priorities amidst considerable reinvestment spending.

Capital adequacy remains sound supporting dividends yet free cash flow dynamics suggest continued reinvestment focus potentially limiting rapid external growth or distribution hikes ahead until efficiency improvements or broader scale are attained.

In this context United Bancorp typifies a traditional community bank balancing prudent risk measures with maintaining competitive positioning amid escalating compliance demands—a balancing act common within mid-tier regional U.S. banks today.

This analysis is based exclusively on available public disclosures without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments