Vistra’s Integrated Model Balances Growth Amid Rising Capital Complexity and Market Volatility

Vistra Corp. leverages a multi-segment, diversified generation fleet and retail platform while navigating uneven earnings and elevated capital expenditures.

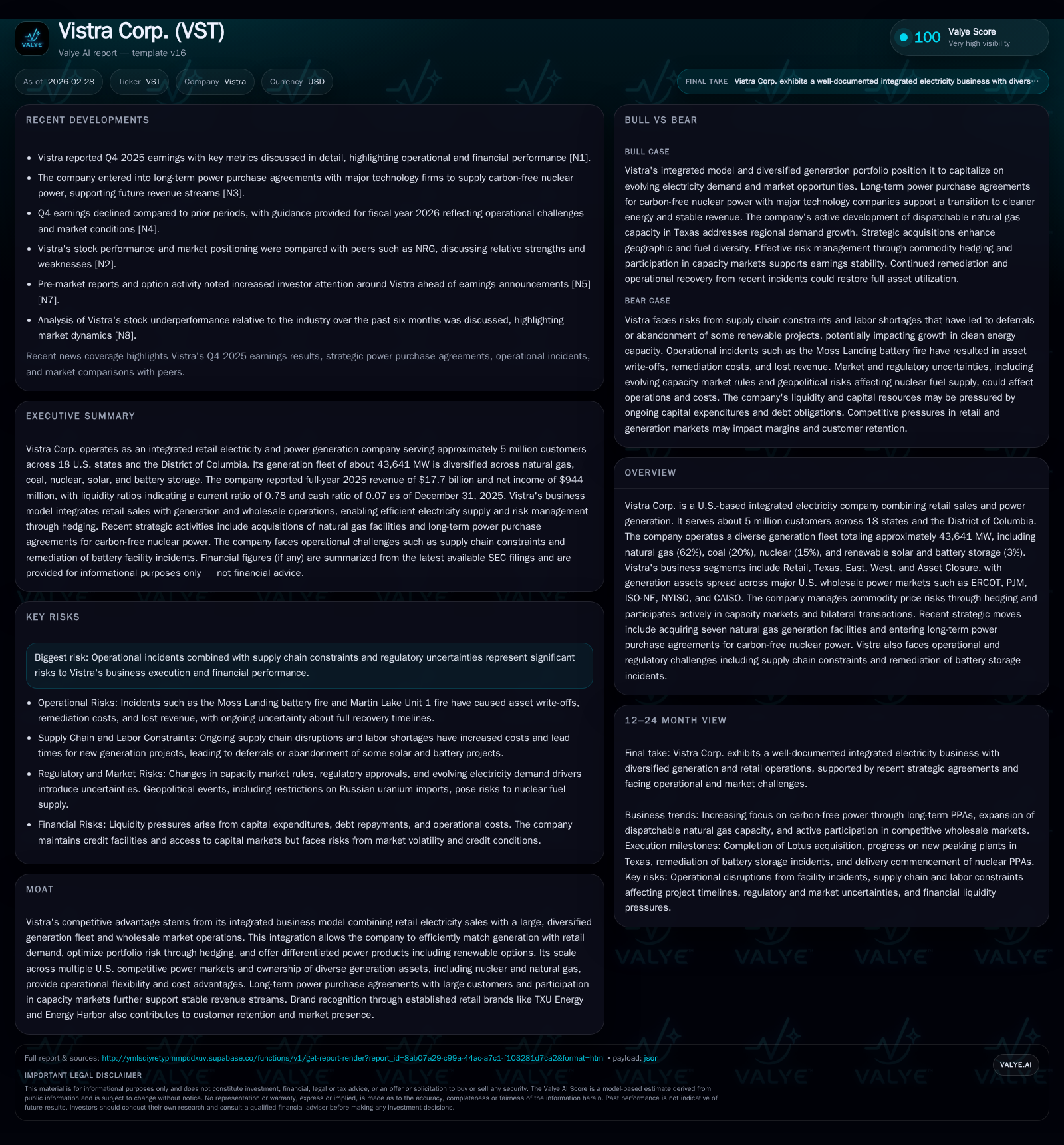

Vistra Corp. operates as a major U.S. integrated electricity company combining retail electricity sales with diverse generation assets including natural gas, coal, nuclear, solar, and storage across multiple wholesale markets. From 2022 to 2025, Vistra expanded revenues steadily but experienced a sharp decline in operating income and net income due to transient factors such as operational incidents and increased expenses. The company is actively executing long-term power purchase agreements with major tech firms for carbon-free power, expanding natural gas capacity through acquisitions, and planning nuclear uprates. Capital allocation reflects aggressive investments balanced by disciplined buybacks and dividends. Key risks include supply chain constraints and regulatory uncertainties that could impact execution.

Company Overview

Vistra Corp. is a significant player in the U.S. energy sector functioning as an integrated electricity provider with a broad reach spanning retail sales and power generation across key competitive wholesale markets including ERCOT (Texas), PJM (Mid-Atlantic), ISO-NE (New England), NYISO (New York), and CAISO (California) [S1][S7]. Serving approximately five million residential, commercial, and industrial customers primarily via its TXU Energy and Energy Harbor retail brands across 18 states and the District of Columbia, Vistra combines customer-centric electricity sales with an extensive generation portfolio totaling roughly 44 GW capacity [S1][S7].

The company’s diversified generation mix includes approximately 62% natural gas, 20% coal, 15% nuclear power, complemented by renewable solar and battery storage making up about 3% of capacity [S1]. This breadth provides Vistra operational flexibility to dynamically respond to energy demand fluctuations through optimized hedging strategies while catering to evolving customer requirements with a variety of products including renewable power options [S1][S7].

Historical Financial Performance

Over the trailing four-year period ending FY2025, Vistra’s top-line revenue showed consistent growth driven largely by acquisitions (notably Energy Harbor merger completed early 2024) alongside organic expansion:

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 17.7 | 0.9 | 4.1 | 1.9 | +3.0% | -64.5% |

| 2024 | 17.2 | 2.7 | 4.6 | 4.1 | +16.5% | +78.1% |

| 2023 | 14.8 | 1.5 | 5.5 | 2.7 | +7.7% | +221.7% |

| 2022 | 13.7 | -1.2 | 0.5 | -1.2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 1028 | 1.3 | 18.5 |

| 2024 | 1266 | 2.5 | 47.7 |

| 2023 | 1245 | 3.8 | 28.1 |

| 2022 | 1949 | -0.8 | -25.0 |

Source: SEC companyfacts cache [F1].

(Source: [F1])

Revenue climbed steadily from $13.7 billion in 2022 to $17.7 billion in 2025 primarily fueled by the addition of Energy Harbor's assets along with material investments into generation capacity expansions [S1][F1]. However, operating income peaked in FY2024 at just over $4 billion before sharply declining more than half (-53%) in FY2025 to roughly $1.9 billion primarily due to operational incidents such as the Moss Landing outages, increased depreciation expense following asset additions, higher interest expense stemming from incremental borrowings linked to acquisitions like Lotus purchase (~$1.9 billion cash base price plus assumption of ~$800 million debt) completed in October 2025, plus lower mark-to-market gains on derivative contracts [S1][S10][S22][F1].

Net income exhibited a similar pattern dropping from $2.66 billion in FY2024 to $944 million in FY2025 (-64%), yet still delivering an approximate return on equity near 18.5%, supported by equity rising modestly due to retained earnings offsetting share repurchases [F1]. Operating cash flow displayed resilience despite partial pressures from increased margin deposits for hedging activities related to commodity price volatility [S17][F1]. Capital expenditures accelerated significantly (+32%) in FY2025 reflecting the company's growth agenda emphasizing natural gas plant developments, nuclear fuel procurement (planned nuclear uprates adding incremental carbon-free capacity beginning circa early next decade), and renewables including solar projects at retired fossil sites [S25][F1].

Share repurchases maintained high levels with about $1 billion spent during FY2025 under renewed board authorization from October 2025; alongside dividends totaling approximately $306 million demonstrating balanced capital return discipline amid expansion efforts [S1][F1].

Future Growth Prospects

Portfolio Expansion & Contract Wins

Vistra is actively pursuing growth through both organic investments and strategic acquisitions focused on natural gas assets for flexible generation capacity alongside carbon-free nuclear energy under long-term contracts [S1][S2]. Recent announcements include:

- A definitive agreement to acquire Cogentrix Energy’s portfolio comprising ten natural gas plants totaling about 5,500 MW expected mid-to-late 2026 closing,

- Development of an additional ~860 MW natural gas facility in West Texas,

- Several long-term PPAs with major tech firms: a landmark 20-year agreement with Amazon Web Services for supplying ~1,200 MW carbon-free power from Comanche Peak Nuclear Plant starting late 2027 ramping into full delivery by mid-2030s,

- Similarly sizable PPA commitments exceeding ~2,600 MW of carbon-free PJM nuclear capacity with Meta Platforms including both existing operating units and uprate projects set for phased delivery expansion through early-2030s [S1][S2][N6].

These contracts anchor future base profitability enhancing earnings predictability by locking in stable revenue streams outside volatile merchant markets.

Renewable Integration & Transition

Vistra continues solar development at former coal plants like Oak Hill (~200 MW commercial operation commenced) while planning substantial retirements or repowering initiatives for aging coal plants transitioning them towards cleaner fuels [S1]. Nuclear uprates pending NRC approvals will increase carbon-free output within PJM increasing output by about 433 MW incrementally ahead of exiting older thermal units [S1]. These efforts align with broader U.S.-wide decarbonization trends stimulating demand growth linked particularly to electrification use-cases such as data centers expansion and electric vehicle charging infrastructure growth.

Regulatory & Market Risks

Capacity market design changes especially within PJM remain an evolving risk factor with FERC engagements underway regarding reliability backstop auctions and co-location transmission fee reforms which could affect unit economics or investment returns [S24]. Additionally current supply chain constraints pose execution challenges on capital projects required for continued fleet modernization.

Operating Segments & Risk Profile

Vistra’s five reportable segments include Retail (comprising energy sales under multiple brand names), Texas (generation + retail focus), East (generation-heavy including PJM assets), West (includes CAISO assets), plus Asset Closure responsible for decommissioning activities related to retired plants ensuring compliance with environmental mandates [S7][S24]. Retail segment contributes scale advantages while generation segments provide operational flexibility across market cycles bridging volatile merchant prices.

Risk factors center on operational incidents impacting availability/productivity—as witnessed with Moss Landing outages—as well as regulatory ambiguity around evolving capacity markets impacting margins; persistent supply chain limitations delaying project timelines add uncertainties [S11][S12]. Cybersecurity is also acknowledged formally at board level given critical infrastructure exposure.

Capital Allocation & Financial Health

Across recent years Vistra displayed disciplined capital deployment focusing on balancing growth investments with shareholder returns:

- Net cash flow from operations remained robust above $4 billion annually,

- Capital expenditures rose markedly reflecting growth agendas targeting diversified fuel sources,

- Share repurchases consistently exceeded $1 billion per year subject to ample liquidity buffers,

- Dividends have been steadily maintained near ~$300 million annually.

Refinancing efforts included senior secured note issuances totaling around $3 billion late-2025 enhancing maturity profiles while reducing interest costs; domestic credit rating upgrades by S&P affirm enhanced credit quality moving into investment grade territory as of December ’25 bolster borrowing capacity at favorable terms [S1][S10][F1].

Liquidity management involved prudent posting of collateral relative to hedging exposures within ISOs/RTOs credit frameworks mitigating financial counterparty risks inherent in commodity markets [S6][S8][S17]. Current ratio stands below unity at approximately .78 reflecting the working capital-intensive nature typical within utilities engaged in trading activities [F1].

What To Watch Next – Analysis Perspective

Absent explicit forward guidance beyond recent PPA milestones and acquisition expectations stated for mid-to-late ’26 closing on Cogentrix deal monitoring several indicators may be insightful:

- Execution progress on aging coal retirements/re-powering projects,

- Further contract wins or expansions securing stable revenue streams,

- Regulatory developments notably around PJM market reforms influencing capacity revenues,

- Operating performance recovering from prior year incidents sustaining margin recovery trends,

- Capital expenditure pacing versus cash flow generation sustaining financial flexibility. Monitoring earnings releases for trajectory shifts on operating income margins along with updates on liquidity positions will clarify financial resilience amid ongoing integration activity.

Conclusion

Vistra exemplifies an integrated utility model navigating the complex intersection of traditional fossil-fueled generation alongside ambitious clean energy transitions anchored by scale retail operations across fragmented wholesale power markets spanning the U.S.A.. While near-term earnings endure pressure from legacy asset performance issues coupled with considerable capital commitments toward asset transformation projects, the structural positioning backed by multi-decade contractual commitments for nuclear power provide robust medium-to-long term earnings stability. The balance sheet improvements via refinancing actions combined with sizeable share repurchase programs demonstrate active capital stewardship amidst substantial business evolution demands. Nonetheless industry dynamics including regulatory shifts affecting capacity pricing frameworks alongside execution risks embedded within large-scale transition projects pose ongoing challenges requiring vigilant oversight.

This report is prepared solely for informational purposes based on publicly filed SEC documents ([F1],[S#]) and verified news sources ([N#]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments