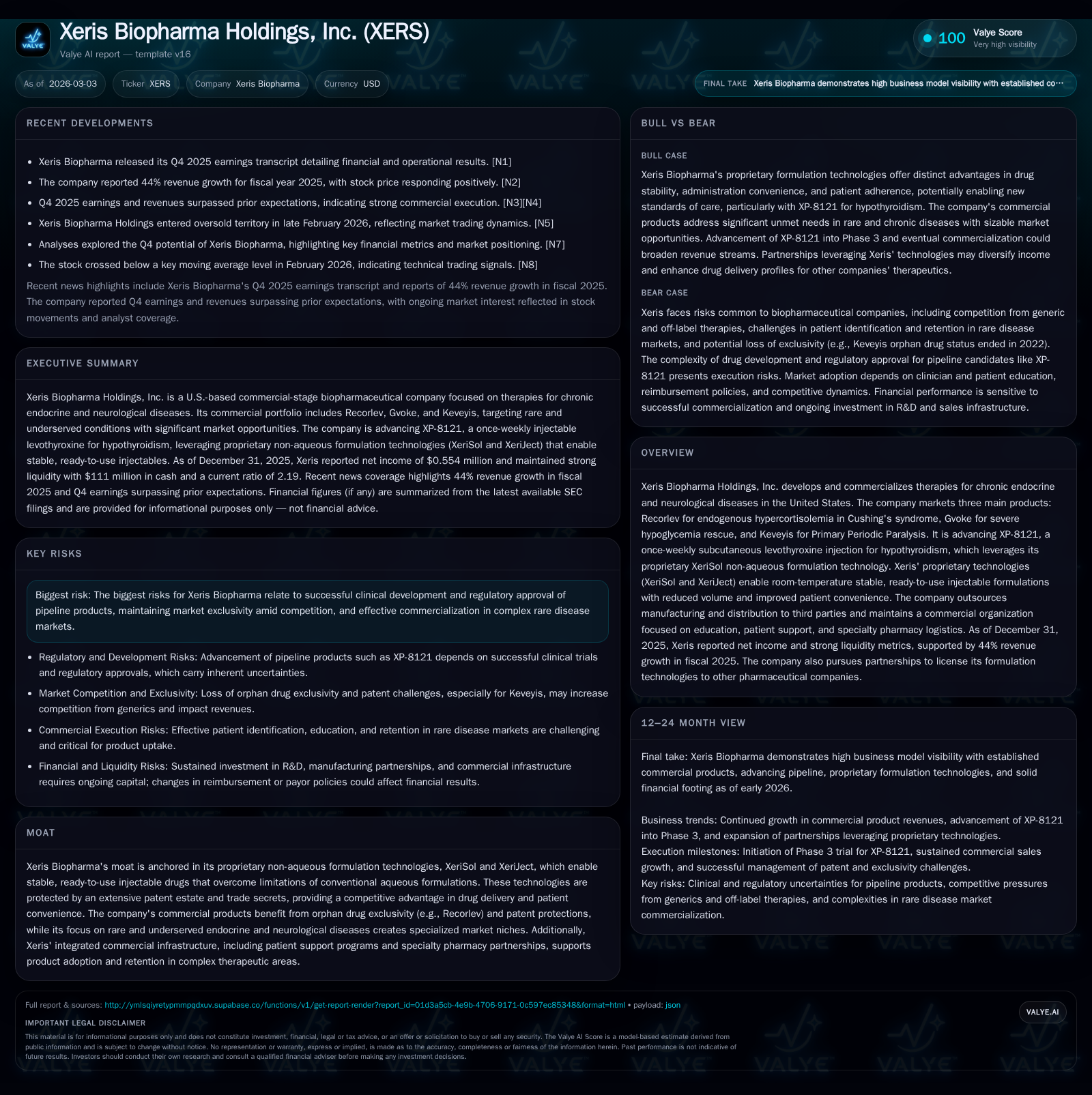

Xeris Biopharma Achieves First Profitability Amid Expanding Rare Disease Franchise

Xeris Biopharma reported positive net income for 2025 driven by ramping sales of orphan and specialty products alongside controlled expenses.

Xeris Biopharma transitioned to operating profitability in 2025 after years of substantial losses, supported by strong growth in its endocrine and neurological disease portfolio. Key commercial products Recorlev, Gvoke, and Keveyis contributed to a 44% revenue increase year-over-year. The company’s proprietary non-aqueous injection technologies underpin product differentiation and stability. While net income is modest and capital structure includes significant debt, cash flows have improved markedly, supporting ongoing R&D investments and commercial expansion. Challenges remain in defending patent exclusivity and advancing pipeline therapies, notably XP-8121 for hypothyroidism.

Historical Performance

Xeris Biopharma reached an inflection point in its financial results for the fiscal year ended December 31, 2025. The company posted operating income of approximately $24.9 million after several years of substantial operating losses (negative $33.6 million in 2024 and larger losses in prior years). Net income swung from a loss of $54.8 million in 2024 to a modest positive net income of roughly $0.6 million in 2025 — the first profitable year since inception [F1][S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 1 | 29 | 25 | +101.0% |

| 2024 | -55 | -37 | -34 | +11.9% |

| 2023 | -62 | -47 | -44 | +34.2% |

| 2022 | -95 | -103 | -82 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 4.0 |

| 2024 | 185.2 |

| 2023 | 917.9 |

| 2022 | -209.5 |

Source: SEC companyfacts cache [F1].

The improvement was primarily driven by commercialization progress of three core products: Recorlev (for endogenous hypercortisolemia/Cushing's syndrome), Gvoke (ready-to-use glucagon for severe hypoglycemia), and Keveyis (treatment for Primary Periodic Paralysis). These therapies address rare but serious chronic endocrine and neurological diseases with relatively limited competition [S1].

Revenue growth outpaced increases in research & development expenses (+22%) and selling/general administrative expenses (+11.6%), indicating improving operating leverage as the commercial infrastructure scales [S16][S18]. Research & development spending remains significant given ongoing pipeline priorities.

Business Model and Competitive Advantages

Xeris’ competitive edge centers on its proprietary non-aqueous formulation platforms — XeriSol and XeriJect — which enable ready-to-use injectable drugs stable at room temperature without complex reconstitution or refrigeration requirements [S1]. This advantage enhances patient convenience, critical for rare disease therapies often administered outside hospital settings.

These platforms provide durable intellectual property protection alongside orphan drug exclusivities enjoyed by flagship products such as Recorlev, whose patents extend through March 2040 barring successful legal challenges [S4].

Future Growth Prospects

Commercial Product Expansion

- Recorlev addresses endogenous Cushing's syndrome patients unsuitable for surgery or inadequately treated surgically — a rare condition with significant unmet need [S1]. Management estimates peak U.S. revenues could approach $1 billion annually based on market penetration assumptions.

- Gvoke targets severe hypoglycemia rescue with an estimated addressable U.S. diabetic population over 14 million at high risk — implying a sizable market opportunity potentially exceeding $5 billion under optimal uptake scenarios [S1].

- Keveyis treats Primary Periodic Paralysis, a rare genetic disorder affecting muscle function with addressable markets estimated above $500 million domestically [S1].

Momentum behind these franchises is expected to continue given ongoing market education initiatives, specialty pharmacy partnerships, and potential label expansions within rare disease segments.

Pipeline Development

The lead investigational program is XP-8121, a once-weekly subcutaneous levothyroxine injection formulated via XeriSol technology targeting hypothyroidism — traditionally managed with daily oral therapy [S1]. This candidate offers potential differentiation through improved adherence and steadier thyroid hormone levels.

Entering pivotal Phase 3 status implies upcoming milestones including trial initiation/readouts, regulatory filings, and potential approvals that could contribute significantly to medium-term growth.

Financial Position and Capital Allocation

Operating cash flow turned positive at $28.6 million in FY25 from negative $37.0 million the prior year; capital expenditures remain modest (~$0.7 million), yielding free cash flow near $27.5 million — supporting sustainability without immediate external financing needs [F1][S19].

Cash and equivalents totaled approximately $111 million at year-end providing liquidity runway amid an accumulated deficit exceeding $671 million due to prior investment cycles [F1][S4][S16].

The company carries over $220 million in debt net of issuance costs including convertible notes maturing between 2028–2029; interest expense decreased slightly (~4.6%) year-over-year reflecting reduced principal balances [F1][S10][S18]. The credit agreement contains covenants limiting dividend payments or stock repurchases ensuring capital preservation for operations and growth investments.

Legal & Regulatory Risks

Xeris faces Paragraph IV patent challenges from generic competitors targeting Recorlev patents expiring in March 2040; the company has initiated Hatch-Waxman litigation defending its intellectual property rights essential for revenue protection .

Additionally, compliance with healthcare laws including anti-kickback statutes, false claims acts, environmental regulations, pricing disclosures, and reimbursement policies imposes ongoing operational risks that can impact costs or market access . Pricing pressures from payors focused on specialty drug cost containment remain an industry-wide challenge.

Summary Analysis

Xeris Biopharma is transitioning into early profitability fueled by robust sales momentum across multiple orphan/rare disease therapies supported by differentiated injection technology platforms protected through patents and trade secrets. Its non-aqueous formulations provide tangible advantages addressing patient convenience barriers inherent in chronic endocrine/neuro conditions.

While reported revenue growth accelerated sharply (44% YoY), profitability gains have been moderate but encouraging given historical losses typical of clinical-stage biopharmaceutical companies moving into commercialization phases [F1][N2][S1]. Positive operating cash flow conversion signals improving operational discipline despite narrow net income margins so far ($0.6M).

The capital structure includes meaningful indebtedness requiring monitoring but is currently manageable given cash reserves. Future upside depends critically on advancing XP-8121 through Phase 3 trials toward market entry alongside scaling core product sales amid competitive and regulatory risks intrinsic to rare disease pharma sectors.

Disclaimer: This analysis provides an informational summary based strictly on publicly available financial disclosures, official SEC filings, company statements, and recognized news sources as of early March 2026 without offering investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments