Planet Image International's Revenue Growth Masks Profitability Pressure

Robust sales expansion contrasts sharply with escalating costs and share-based compensation, compressing earnings in 2025.

Planet Image International Ltd (Nasdaq: YIBO) sustained top-line growth in 2025, driven by a diversified global footprint and an integrated manufacturing-sales model underpinned by proprietary technology. However, profitability deteriorated markedly as gross margins shrank due to pricing pressures, increased material costs, and higher selling expenses compounded by significant share-based compensation charges. The company’s capital allocation reflects caution amid negative operating cash flow and limited capital returns, while risks persist from geopolitical trade policies and regulatory issues in China. Future growth hinges on innovation via an extensive patent portfolio and management’s strategic responses to margin headwinds and market diversification.

Steady Revenue Growth Through an Integrated Global Model

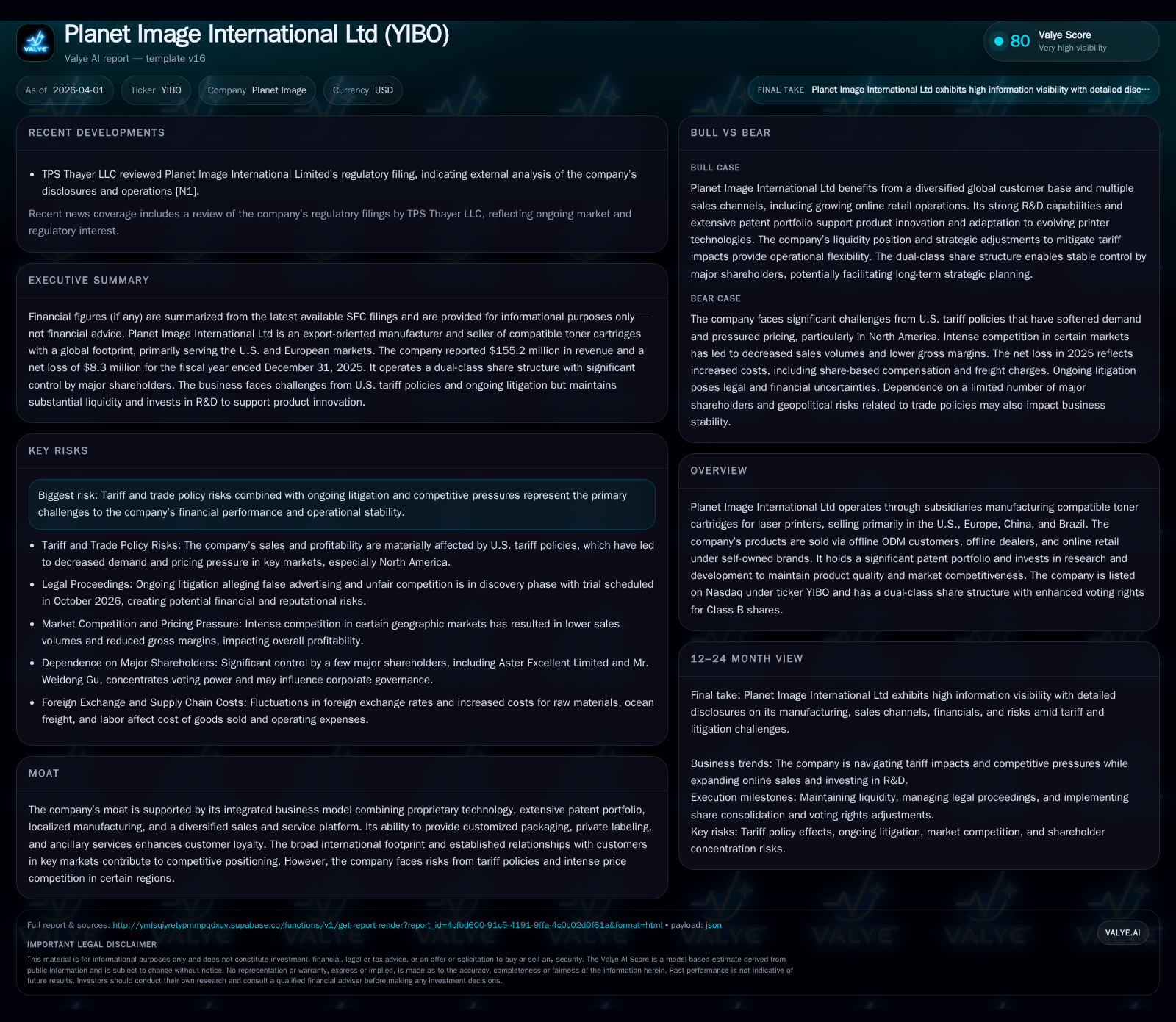

Planet Image International Ltd recorded revenues of $155.2 million for fiscal year 2025, representing a 3.6% increase over the previous year’s $149.8 million [F1][S1][S4]. This incremental growth underscores the effectiveness of its integrated export-oriented model combining proprietary R&D-driven manufacturing with diversified sales channels: offline ODM customers who private-label products, offline dealers reselling white-label and self-branded cartridges, plus a growing online retail presence under its own brands [S1][S4][S20]. The broad international footprint spans key established markets—primarily North America and Europe—with recent expansion into Asia-Pacific markets such as China and Brazil contributing substantially to revenue gains [S8]. This cross-channel approach enhances market responsiveness by coupling product innovation with localized logistics and customer service.

Despite largely consistent product capabilities between ODM and white-label offerings, differentiation occurs through customized packaging options and flexible pricing strategies tailored per channel [S15]. The company's ability to control the entire value chain bolsters its time-to-market advantage across new printer models whose technology evolves rapidly—a critical factor given sector dynamics favoring compatibility [S22].

Margin Pressure and Profitability Setbacks in 2025

Underlying this topline resilience is a sharp deterioration in profitability metrics that starkly reverses the positive trajectory observed through 2023–24. Operating income declined precipitously from a $6.9 million profit in 2024 to an $11.3 million loss in 2025 [F1], amounting to a -264% year-on-year swing [F1]. Net income mirrored this pattern, dropping from $7.1 million profit to an $8.3 million loss (-216% YoY) [F1]. The magnitude of this loss was driven chiefly by several factors:

- A substantial increase of $8.6 million in share-based compensation expense linked to equity grants under the company’s new 2025 Equity Incentive Plan [S1][S3][S7].

- Gross profit contraction totaling approximately $6.6 million stemming from lower average selling prices (ASPs) on core products facing intensified price competition, paired with rising input costs for raw materials including OPC drums, toner powders, chips, plus elevated freight charges especially via overseas warehouses connected to online sales platforms [S3][S7][S8]. The gross margin slid from a solid 34.9% in 2024 down to just 29.4% in 2025—a notable compression for a manufacturing business heavily reliant on scale economies [F1][S7].

- Increased selling expenses by about $4.2 million due largely to expansion-related payroll increments, facility lease costs for new office/warehouse spaces mainly in China and the U.S., as well as elevated freight expenses accompanying larger online order volumes [S7].

- A rise in income tax expenses attributable to reduced tax loss carryforwards following prior profitable years [S1].

- Foreign exchange volatility that swung $2.6 million from gains into losses due to currency fluctuations across USD, EUR, RMB, GBP [S1][S7].

The unit economics reflect adverse tariff impacts as well; U.S. import duties applied on certain compatible toner cartridges pressured ASPs within the dominant North American channel by increasing landed costs for customers—though management proactively adjusted resource allocation toward Asia sales as partial mitigation [S17]. This cascade of price competition allied with cost-push effects illustrates the precarious margin environment facing Planet Image’s business.

Historical Financial Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 155 | -8 | -2 | -11 | +3.6% | -216.0% |

| 2024 | 150 | 7 | -2 | 7 | -0.3% | -8.5% |

| 2023 | 150 | 8 | 18 | 13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | -14.3 |

| 2024 | -3 | 12.5 |

| 2023 | 17 | 23.5 |

Source: SEC companyfacts cache [F1].

International Footprint and Market Concentration Dynamics

North America remains Planet Image's largest single region accounting for close to half its revenues (~47% in 2025), followed by Europe—where German operations lead—but witnessed revenue declines circa -8.7% in 2024 due primarily to competitive intensity in Eastern Europe markets like Russia amid geopolitical instability [S4][S6][S14]. In contrast, Asia showed exponential growth (+89.5%) initiated by successful penetration of China’s growing compatible cartridge market aided by favorable customer satisfaction outcomes domestically [S8]. Brazil likewise contributed robustly with over +67% revenue increase emphasizing strategy diversification beyond historically high-dependence Western markets.

Customer profiles encompass wholesale dealers and offline ODM brand owners requiring private labeling or customized packaging while supporting direct-to-retail e-commerce channels [S4][S14]. ODM sales exhibited strong volume growth yet borne mixed margin impacts given competitive pricing pressures—the offline dealer segment faced margin erosion largely related to tariffs levied on shipments into the U.S., resulting in tactical withdrawal or scale reduction within certain contested areas like Mexico and parts of Eastern Europe where pricing aggressiveness intensified dramatically [S6][S7][S14][S17].

Tariff-related trade policies remain a significant risk vector restricting pricing flexibility with opaque regulatory outcomes combined with intensifying rivalry from low-cost producers influences revenue concentration strategically requiring broader global exposure.

Innovation and Patent Portfolio as Competitive Differentiators

Central to Planet Image’s strategic moat is its extensive intellectual property foundation comprising over 400 registered patents along with additional pending applications spanning key jurisdictions including U.S., Europe, Mainland China, and Hong Kong—reflecting sustained R&D commitment vital for technological compatibility amid printer OEM evolutions [S14]. Its R&D spend increased from approximately $6.2M (2024) to $9.8M (2025), reflecting not only regular capex infusion but also escalating stock-based compensation costs embedded within this line item aligned with incentivizing technical talent retention under competitive industry conditions [F1][S5][S16][S22].

This patent-backed portfolio enables differentiated cartridge designs optimized for reliability while permitting ancillary services such as bespoke packaging solutions, drop-shipping logistics supports for offline clientele plus private labeling—collectively fostering higher customer loyalty even amidst commoditized market segments where product parities are otherwise thin [S21][S22]. The capacity to deliver timely upgrades keeps inventories relevant strategically minimizing technological obsolescence risk prevalent given fast printer innovation cycles posing inventory markdown dangers otherwise.

Operating leverage comes into play through disciplined but selective capital expenditure focusing mainly on mould acquisition for production tooling upgrades alongside investments into logistic infrastructure particularly warehousing solutions facilitating multi-channel fulfillment enhancements [F1][S16][S22].

Capital Allocation Under Strain: Negative Operating Cash Flow and Limited Buybacks

Despite nominally stable top-line metrics, Planet Image’s financials depict mounting strains on internal liquidity fueled by operational losses manifesting as negative operating cash flows—the latest disclosed CFO fell further into negative territory at approximately -$2.44 million for FY2025 against -$2.15 million in FY2024 denoting slight deterioration alongside compressed free cash flow available post-capex which stood near -$3.27 million given modest capital expenditures capped at $825K—marking a near 27% decline versus prior year investments aimed at prudent spending amid uncertainty [F1][S18].

Return metrics confirm this pressure; estimated return on equity slipped decisively into negative territory near -14%, mapping net income losses despite equity base expansion primarily driven by retained earnings depletion reversal post-loss recognition [F1]. No dividends were issued during these years nor were any share repurchase programs active—indicating conservative capital return policy oriented towards balance sheet preservation rather than shareholder distributions or aggressive buyback deployment currently [F1][S18].

Borrowings remain moderate though guarantees extended personally by major shareholders underpin short-term financing facilities supporting working capital needs primarily linked to inventory build-up timing matching fluctuating demand episodes encountered regionally especially around peak seasons or tariff uncertainty periods [F1][S10][S19][S21]. This cautious stance reflects management’s awareness of prevailing margin squeezes demanding careful liquidity stewardship.

China Operations Risks and Regulatory Uncertainties

Operating through subsidiaries domiciled predominantly within mainland China infuses Planet Image with systemic regulatory exposure unique among global peers—facing multifaceted risks spanning economic shifts under PRC government policies through legal system modifications that may materially impact operational latitude or compliance burdens unexpectedly [S24][N1]. Notably relevant are restrictions surrounding dividends repatriation constraints where limitations imposed under PRC foreign exchange regimes or tax classifications could hamper transferring profits offshore attenuating consolidated cash flexibility vital for servicing global operations headquartered outside China jurisdictional spheres [N1][S24]. Additionally, offshore financing arrangements encounter procedural complexity potentially delaying capital inputs critical for scaling manufacturing capacities or funding R&D pipelines dynamically responsive to evolving market demands.

Further compounding these threats is governmental influence capacity potentially altering operational modalities spontaneously thus introducing an overlay of political risk challenging predictability for minority investors reliant purely on international capital market mechanisms without direct participation control privileges despite dual-class share structures conferring some voting rights enhancement to controlling shareholders [N1]. These geopolitical dimensions underline prudence required when weighing Planet Image’s intrinsic innovation strengths against external uncertainties particularly when navigating channel-specific tariff evolutions predominantly affecting U.S./Europe sales more than domestic ones but nonetheless cascading through global logistical networks.

Outlook: Key Operational Metrics and Market Drivers to Watch

Looking ahead beyond documented full-year data points is inherently speculative; however analysis-guided views identify pivotal variables shaping Planet Image's near-term trajectory:

- Board-approved share consolidation plans originally resolved at ratios between one-for-twenty-six up to one-for-eight-thousand shares underscore efforts at optimizing share structure possibly aiding liquidity or indexing attractiveness upon final ratio determination before the formally scheduled 2027 annual general meeting injection point [N1][S2].

- Product mix evolution remains critical as shifts toward newer compatible cartridges exhibiting material cost inflation necessitate agile pricing tactics balancing volume retention against margin volume trade-offs frequently revisited amidst volatile tariff landscapes especially in U.S.

- Continued monitoring of litigation outcomes pertinent to intellectual property disputes remains relevant given industry history rife with infringement risks though none presently detailed specifically affecting YIBO materially per filings.

- Tariff policy adjustments alongside freight cost fluctuations bear immediate influence over unit economics requiring reactive supply chain reengineering or geographic rerouting optimizing landed cost efficiency.

- Execution on innovation investments safeguarding quality differentials backed by patented technology represents ongoing synthetic moat maintenance tethered directly to customer retention vigor especially within fiercely fragmented aftermarket channels.

Investors should thus track updates from quarterly filings for changes in selling expense compositions, share-based payment trends impacting bottom line volatility, plus commentary on regional sales performance nuances providing advance warning signals regarding evolving competitive dynamics.

This report consolidates publicly filed financial statements from Planet Image International Ltd (Nasdaq: YIBO) up through fiscal year ended December 31, 2025 along with recent regulatory disclosures supplemented by domain-specific analysis contextualized within compatible toner cartridge aftermarket industry characteristics without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments