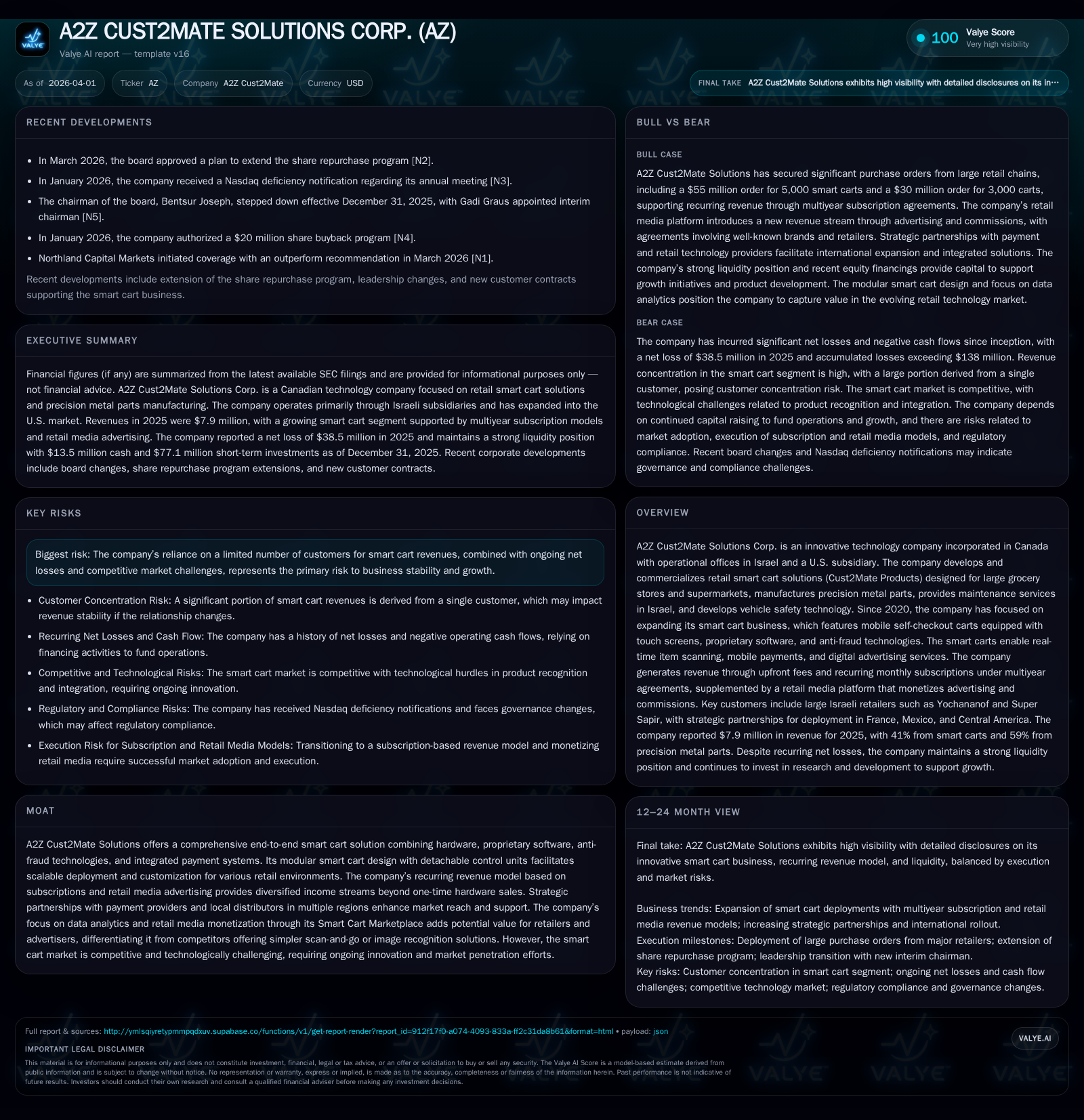

A2Z Cust2Mate’s Modular Smart Cart Journey: From Rapid Growth to Scaling Challenges

A2Z Cust2Mate Solutions Corp. has evolved its smart cart technology into a modular, subscription-based platform amid rising costs and competitive pressures.

A2Z Cust2Mate Solutions Corp. has built a distinctive retail technology business centered on its modular smart carts that integrate hardware, proprietary software, anti-fraud measures, and payment systems. Revenues increased to $7.9 million in 2025, driven by expanded deployments, but operating costs surged sharply due to intensified R&D and administration expenses, driving net losses of $38.5 million and challenging profitability. The company’s shift to recurring subscription revenues and retail media monetization diversifies income but depends heavily on a limited customer base and market adoption pace. Adequate liquidity and a continued share repurchase program underscore management’s focus on capital discipline as it balances scaling potential with operational constraints.

From Startup to Market Entrant: Trajectory of Historical Growth

A2Z Cust2Mate Solutions Corp.’s financial journey over recent years illustrates the transition from early breakthrough revenue growth toward operational challenges linked to scaling its innovative smart cart technology. Revenues for fiscal year (FY) 2025 reached approximately $7.9 million, representing a roughly 10% increase compared to about $7.17 million in FY2024 [F1]. This growth was propelled mainly by increased deliveries within their smart cart segment following completion of a significant purchase order for Yochananof in 2023 [S6][S18]. However, this top-line momentum masks underlying margin pressures—gross profit declined from roughly $1.89 million to $1.09 million due to higher material costs and scale-related factors.

Costs expanded aggressively during this period: Research and Development (R&D) expenses soared from approximately $3.85 million in FY2024 to nearly $9.94 million in FY2025, driven largely by replacing external subcontractors with internal staff for better quality control [S6]. Sales and marketing outlays also climbed from about $1.22 million to nearly $3.86 million as the company targeted wider market penetration [F1][S6]. Most notably, general and administrative (G&A) expenses ballooned from around $7.95 million to an outsized $23.75 million, straining the cost structure amidst rapid corporate expansion [F1][S6]. These dynamics culminated in an operating loss of approximately $36.46 million for FY2025—nearly triple the prior year—and a net loss of about $38.48 million [F1], underscoring the significant investment phase A2Z undertook.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 8 | -38 | +10.3% | -99.8% |

| 2024 | 7 | -19 | -37.0% | -6.7% |

| 2023 | 11 | -18 | +21.6% | +1.6% |

| 2022 | 9 | -18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -50.4 |

| 2024 | -281.5 |

| 2023 | 782.0 |

| 2022 | -635.1 |

Source: SEC companyfacts cache [F1].

Table: A2Z Cust2Mate Annual Financial Performance (USD millions)[F1]

Understanding Revenue Composition and Technological Edge

The company's innovation centers on its fully integrated 'smart cart' system deployed primarily in large grocery chains and supermarkets [S5]. Unique among competitors, A2Z combines modular hardware featuring detachable control units with proprietary software supporting real-time item scanning on the cart’s large touchscreen interface, embedded anti-fraud measures, plus integrated mobile payment capabilities [S15]. This contrasts with more common 'scan-and-go' handheld app models or emerging image recognition solutions that face practical SKU recognition challenges at scale.

Revenues arise from multiple streams: outright sales of smart carts coupled with monthly maintenance fees; an evolving subscription model retaining ownership while providing customers multi-year access against upfront fees plus ongoing payments for updates and service; and a digital services layer—the Smart Cart Marketplace—enabling retailers to offer targeted promotions, digital advertising, e-coupons, and data analytics monetized via commissions [S5]. This approach extends value creation beyond physical hardware sales into recurring SaaS-type revenues bolstered by retail media platforms.

Modularity permits retrofitting existing store fleets without high replacement costs—a strategic driver for scalability internationally—including partnerships facilitating installation and support across the U.S., Mexico, France, Australia, Israel, Canada, and Chile [S4][S18]. Recent collaborations include Nayax Ltd., integrating automated mobile payments into the platform launched first in France [S18].

Cost Structure Evolution and Impact on Profitability

A striking feature is the steep escalation in expenses accompanying growth [F1][S6]. R&D costs more than doubled year-over-year from approximately $3.85 million to nearly $10 million reflecting internalization of software engineering talent previously outsourced—aiming at deeper integration with customers’ POS systems—and advancing product iterations focused on lighter cart designs with detachable control units [S6].

Sales and marketing expenditures tripled as the company invested heavily in expanding geographic footprints through partner channels alongside direct marketing efforts targeting major retailers [F1][S6]. Administrative overhead similarly expanded disproportionately—driven by infrastructure build-out for global operations including compliance complexities across jurisdictions [F1][S6]. This cost inflation overwhelmed gross profits which remained thin amid stiff competition.

Consequently, operating leverage proved elusive: substantial revenue gains were offset by sharp expense increases leading to deeper annual operating losses approaching $36 million—the worst performance since inception—and magnified net losses nearing negative $39 million [F1]. This exemplifies typical ‘scale-up spikes’ where early commercial success carries steep organizational build costs before efficiency gains emerge.

Recurring Revenue Model and Retail Media Monetization Strategy

A competitive differentiator is shifting away from reliance solely on upfront cart purchases toward a subscription-based model offering multiyear contracts covering hardware leasing alongside software maintenance, upgrades, service support plus optional digital add-ons like navigation maps or personalized shopping lists [S5]. This enables smoother revenue recognition via monthly payments aligning incentives for continuous platform enhancement.

Further diversification comes from the Smart Cart Marketplace functioning as an embedded advertising ecosystem inside the carts’ touchscreens [S5]. Retailers monetize shopper engagement through targeted ads delivered at decision points—a valuable channel given physical retail’s increasing need for data-driven promotional insights absent at checkout-only alternatives.

Retailers benefit from improved consumer behavior analytics generated via integrated AI capable of mapping shopper routes, dwell times, purchase decisions prior to payment completion—insights previously unavailable without expensive infrastructure elsewhere [S10]. The platform also facilitates revenue sharing among retailers, brand manufacturers, third-party advertisers potentially lowering net cart costs reducing adoption barriers.

Competitive Positioning and Industry Partnerships

Several competitors offer partial solutions such as handheld scanners ('scan-and-go') or attempt unproven AI image recognition claimed as 'one-to-many' SKU identification technologies still struggling with accuracy across tens of thousands of SKUs under variable conditions [S15], but A2Z offers one of few end-to-end turnkey smart cart platforms fully integrating scanning hardware/software/anti-fraud/payment in one package.

Partnerships leverage non-exclusive distributor agreements especially in the U.S., where Cust2mate USA Inc., established mid-2023 coordinates localized deployments supported by Level10 LLC—a recognized retail IT service firm handling nationwide installation and support services [S4][S18]. Entities serving Mexico/Central America/France/Chile also act as crucial conduits enabling broad reach without direct sales overheads [S4].

The design advantage of detachable control units allows legacy carts retrofitting without full fleet replacement costs improving incremental market entry economics while accommodating retailer-specific customization—a practical edge over rigid designs requiring heavy capital outlay upfront.

Nonetheless customer concentration remains notable—with significant revenue reliance on Yochananof chain orders highlighting vulnerability should key client dynamics shift unexpectedly [S7][S29].

Capital Allocation Review: Share Repurchases Amid Losses

Despite sizable net losses eroding earnings (-$38 million in FY25), management maintains capital discipline evidenced by board-approved share repurchase programs extended into early 2026 aimed at supporting liquidity management & shareholder value preservation amid volatile trading environments [N2][S9][F1].

Equity capitalization strengthened markedly—from negative equity (-$2.31 million in FY23) through successive financings resulting in robust equity exceeding $76 million by end-2025 primarily via share issuances coupled with warrant exercises boosting cash reserves alongside working capital adequacy [F1][S26].

Return on equity stands deeply negative (~-50%) reflecting unprofitable operations weighted against inflated equity stakes accumulated through financing rounds rather than retained earnings so far [F1]. Yet healthy cash positions near $13.5 million combined with current ratios exceeding 11x reinforce sufficient runway allowing continued R&D investments without immediate jeopardy despite elevated operating cash burn [$22+ million used in operations during FY25] [F1][S12]-[S14].

Liquidity, Financial Strength, and Balance Sheet Highlights

Liquidity metrics portray solid short-term financial footing underpinning scaling efforts despite losses: Total current assets reported at approximately $79.4 million vastly exceed current liabilities near $7 million yielding a current ratio around an impressive 11:1—signaling excellent ability to meet upcoming obligations comfortably [F1]. Cash balances are stable compared to prior year around $13.5 million while other liquid investments totaling above $55 million support flexibility albeit likely earmarked for ongoing projects or strategic initiatives [F1][S12]-[S14].

Total liabilities remain modest relative to assets; lease liabilities present but do not materially constrain financial adaptability currently; warrant liabilities reduced substantially reflecting exercised instruments providing fresh capital inputs during FY25 helping sustain working capital adequacy even under adverse cashflow trajectories [F1][S13]-[S14].

Future Outlook: Growth Potential Meets Operational Constraints

Near-term prospects hinge on further deployments within multi-store chains leveraging refined modular cart designs that reduce weight & improve maneuverability while maintaining integration breadth featuring detachable control units enhancing retrofit opportunities globally [N1].

Strategic partnerships such as those formed with Nayax for embedded payment integration represent important milestones signaling platform maturation towards broader commercial appeal outside flagship clients currently dominating revenues notably Yochananof which contributed meaningful sales portions but whose order book fluctuates dynamically impacting revenue predictability [N1][S23].

However risks persist including intense competition vying with scan-and-go apps or emerging image recognition approaches creating pricing pressures alongside technological hurdles inherent in refining real-time SKU-level recognition accuracy consistently across diverse retail environments limiting adoption speed despite technological advantages held by A2Z’s fully integrated approach (hardware/software/anti-fraud/payment unified system) [S15][S23]. Customer base concentration compounded by ongoing net losses further cloud stability until scale economies are demonstrated sustainably.

Key Milestones Investors Should Monitor

Critical upcoming developments include subscriber expansions under subscription licenses fostering more predictable monthly recurring revenues; new partnership rollouts beyond initial markets emphasizing U.S.-centric deployments through Cust2mate USA Inc.; advancements or launches related to lighter modular smart cart iterations designed for easier host-fleet integration enhancing commercialization potential; rigor around controlling administrative cost escalations amid global footprint enlargement; plus progress validating retail media platform monetization supporting diversifying revenue streams beyond hardware-software sales alone [N1][N2][S5][S19]. Monitoring cash flow trends particularly operating cash burn reductions relative to topline lifts will signal operational leverage gains critical given current negative profitability trends offset somewhat only by strong balance sheet liquidity offering cushion for one-to-two year horizon presently.

This analysis is based exclusively on publicly available filings from A2Z Cust2Mate Solutions Corp., inclusive of SEC disclosures up through April 2026 plus cited news releases; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments