Sidus Space Faces Revenue Contraction and Escalating Losses Amid Growth and Capital Raises

Emerging aerospace company Sidus Space shows operational scale-up alongside deteriorating profitability and reliance on equity financing.

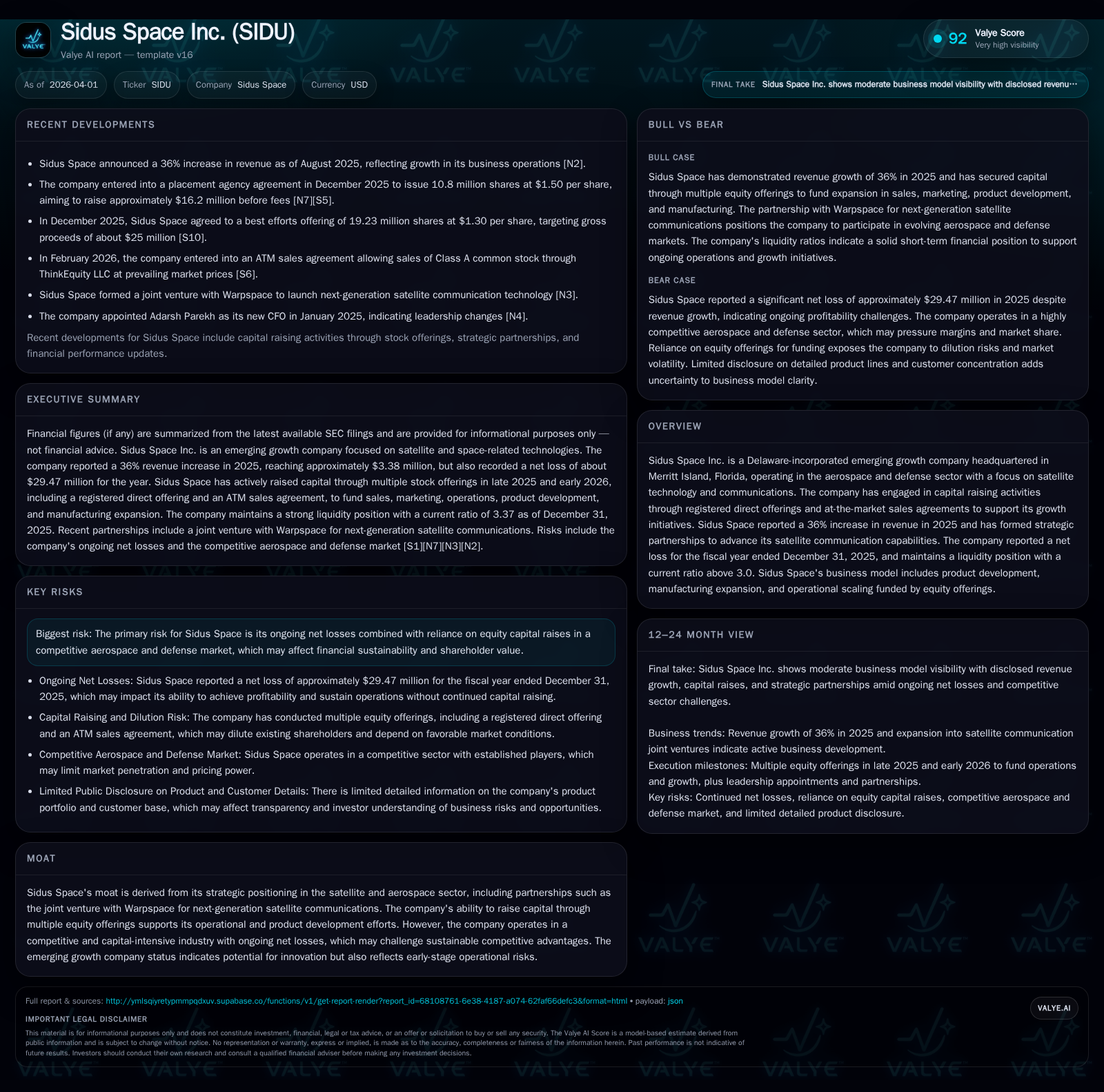

Sidus Space Inc., an emerging satellite technology firm, posted a revenue decline of approximately 28% in 2025, reversing prior growth trends while net losses widened significantly. The company continues to invest heavily in production capacity and product development, reflected in rising operating costs and capital expenditures. To fund these commitments, Sidus Space conducted multiple equity offerings including direct registered offerings and at-the-market sales agreements, underpinning its liquidity position with a strong current ratio near 3.4x. Despite strategic partnerships and advances in satellite communication capabilities, the firm's limited operating history and ongoing losses underscore substantial financial risks.

Company Overview

Sidus Space Inc., headquartered in Merritt Island, Florida, operates in the aerospace sector specializing in satellite technology and communication systems [S1]. Founded out of Craig Technologies Aerospace Solutions (CTAS), the company evolved from a manufacturing-centric business into an integrated space and defense technology provider in 2021 [S1]. Equipped with a 35,000-square-foot facility near Florida’s Space Coast launch infrastructure, Sidus leverages a multidisciplinary engineering team developing satellites across Low Earth Orbit (LEO), Geostationary Orbit (GEO), and lunar applications [S1].

Historical Financial Performance

Over the past four years through fiscal year 2025, Sidus Space experienced a marked deterioration in revenue alongside escalating operational losses [F1]. Revenues declined annually from $7.29 million in 2022 down to $3.38 million by end-2025 — a cumulative collapse reflecting challenges in customer acquisition and contract timing volatility inherent in aerospace project deliveries.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3 | -29 | -18 | -28 | -27.6% | -68.2% |

| 2024 | 5 | -18 | -16 | -16 | -21.6% | -22.3% |

| 2023 | 6 | -14 | -12 | -13 | -18.2% | -11.6% |

| 2022 | 7 | -13 | -12 | -12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -26 | -58.2 | |

| 2024 | 19555 | -23 | -74.5 |

| 2023 | 19555 | -19 | -200.9 |

| 2022 | -14 | -331.3 |

Source: SEC companyfacts cache [F1].

Operating income reflects deeper losses yearly despite attempts to scale production and service capabilities [F1]. Negative operating cash flows persist significantly below zero alongside rising investment in capital assets supporting manufacturing expansion.

Business Model and Growth Drivers

Sidus generates revenue through multiple streams aligned with the space mission lifecycle: satellite platform sales/customization; payload hosting; engineering integration services; hardware manufacturing; proprietary AI-based computing products; and emerging subscription access to space-derived data analytics [S1]. This diversified approach attempts to balance fixed-price contracts typical for satellite missions with recurring or milestone-based revenues.

Noteworthy is the company’s recent strategic partnership with Warpspace targeting next-generation satellite communications — an important moat element given the competitive landscape dominated by larger incumbents investing heavily into constellation deployments [N1]. Furthermore, operating near launch facilities aids accelerated schedule alignment but supply chain complexity for space-rated components remains a persistent risk [S1].

Future Growth Prospects

While revenue contraction persisted through FY25 due to execution timing delays and initial commercial traction challenges [F1], ongoing investments into production level manufacturing and launch cadence suggest potential inflection points ahead if contracted orders translate consistently into spacecraft deliveries. Product development continues focusing on AI-enabled computing platforms embedded within satellites — an area gaining market interest as edge analytics for space assets become critical.

Risks constraining growth include intrinsic high capital intensity requiring continuous funding rounds; difficulty forecasting contract wins amid shifting defense/commercial budgets; retaining top-tier engineering talent for emerging technologies like AI integration; managing geopolitical restrictions affecting international customers; plus intellectual property protection challenges inherent in dual-use aerospace sectors [S1].

Capital Structure and Liquidity

To underpin its growth strategy given sustained losses—$29.5 million net loss for FY25 alone—Sidus has frequently tapped equity markets via registered direct offerings and ATM sales agreements [S5][S6][S7][S8][S15][S16][S17][S18]. Notably:

- In December 2025 alone: two placement agency agreements raised aggregate gross proceeds exceeding $40 million covering marketing expansion product development manufacturing scale-up working capital general corporate purposes.

- The transactions carried customary placement agent fees around ~7% along with warrants incentivizing agents [S15][S16].

At December year-end 2025 the company’s current assets significantly exceeded current liabilities ($50.7M vs $15M), producing a strong current ratio near 3.37 indicating short-term solvency adequacy despite operational cash burn [F1]. However free cash flow remains deeply negative (approximately -$26.3 million in FY25), pointing to ongoing reliance on financing over internal funds generation.

Shareholders' equity has risen sharply from under $4M at end-2022 to over $50M by end-2025 due primarily to cumulative equity infusions alleviating balance sheet risks but diluting ownership concentration accordingly [F1]. No significant dividends or share repurchases have been reported given capital preservation priorities [F1][S9][S10].

Industry Context Analysis

The satellite manufacturing sector involves long lead times from design through launch to commissioning plus volatile contract flows influenced by government procurement cycles commercial constellation deployments and emergent space data monetization models such as subscription-based analytics access. Integration of AI onboard satellites represents an emerging vector requiring significant R&D investment but promises differentiation if effectively commercialized.

Competition includes legacy aerospace contractors expanding into small sats new-space entrants aggressively scaling constellations while defense agencies increasingly leverage commercial partnerships demanding agility cost-effectiveness secure supply chains.

Supply chain for space-grade elements is notoriously complex prone to bottlenecks impacting schedules—a challenge exacerbated by global semiconductor shortages geopolitical risks affecting materials origins escalating component costs influenced by inflationary pressures.

What To Watch Forward (Analysis)

Key milestones involve:

- Achievement of steady state production volumes elevating satellite deliveries supporting revenue stabilization or growth reversal;

- Material contract wins with commercial or defense customers indicating validated market demand;

- Successful commercialization of subscription data service revenue streams expanding recurring income base;

- Execution on technical roadmaps embedding AI-enabled capabilities demonstrating competitive differentiation;

- Maintaining sufficient liquidity leveraging capital markets efficiently without excessive shareholder dilution;

- Managing supply chain stabilization reducing cost overruns delays enhancing gross margins potential.

Failure on any of these fronts could exacerbate existing financial pressure given persistent net losses coupled with high fixed costs.

Conclusion

Sidus Space exemplifies an emerging growth aerospace player attempting rapid scale-up in a capital-intensive competitive environment complicated by volatile revenues contracting since peak levels four years ago despite market potential indicated by strategic partnerships. Its significant equity financing activities underscore ongoing dependency on external funds fueling primarily product development manufacturing expansion working capital rather than profitable operations.

Investors should weigh the company's ambitious multi-revenue stream model supported by technical depth against historical financial trends highlighting large losses negative cash flows early-stage operational risks related to proof-of-concept commercialization uncertainty supply chain fragilities plus macro factors affecting aerospace/defense spending trajectories.

This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments