TOYO Co., Ltd Executes US Expansion Amid Concentration and Liquidity Challenges

TOYO’s rapid capacity additions in solar manufacturing coincide with notable customer concentration and liquidity pressures, shaping its near-term financial dynamics.

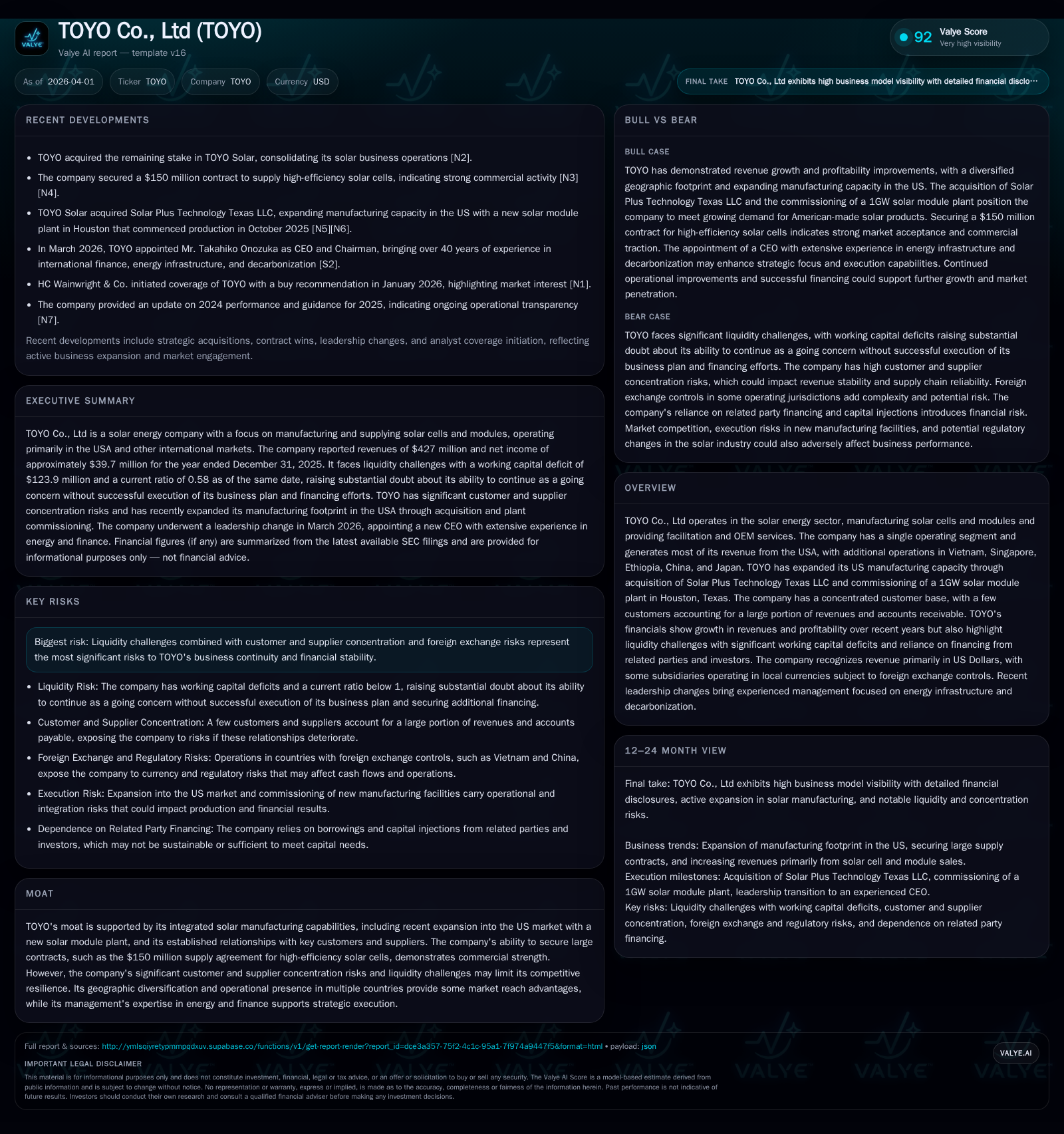

TOYO Co., Ltd marked a period of aggressive top-line growth driven by commissioning major new production facilities and strategic acquisition in the US market. However, this expansion amplifies customer concentration risks alongside pronounced working capital deficits and reliance on related-party financing. Despite strong operating cash flow generation and improved operating income, net income remained relatively flat due to increased expenditures and capital needs. Leadership changes point toward a recalibration focused on governance and energy finance expertise. The company’s future trajectory hinges on sustaining key customer relationships while managing liquidity amid significant capital investments.

Record Revenue Growth Fueled by Capacity Expansion

TOYO Co., Ltd demonstrated exceptional revenue growth in fiscal year 2025, achieving $427.4 million — more than double the $177.0 million recorded in 2024, representing a 141.5% year-over-year increase [F1]. This surge was largely underpinned by the commissioning of new solar cell production capacity: notably the 4GW facility in Ethiopia activated in October 2025 and the fully utilized 2GW plant in Vietnam [S1]. The company also expanded its OEM collaborations, securing additional third-party orders that contributed to top-line momentum.

Operating income experienced an even more pronounced rise, climbing by approximately 566% to reach $59.0 million in 2025 from $8.9 million a year earlier [F1]. This leap illustrates productive operating leverage as fixed costs were absorbed across higher volumes, although the absolute margin improvement is tempered by elevated expenditure tied to expansion initiatives.

The following table summarizes TOYO’s key annual financial metrics over the past two fiscal years:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 427 | 40 | 133 | 59 | +141.5% | -2.3% |

| 2024 | 177 | 41 | 47 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 41 | 35.6 |

| 2024 | 4 | 68.6 |

Source: SEC companyfacts cache [F1].

(Data sourced from company filings [F1])

Customer Concentration: A Double-Edged Sword

TOYO’s revenue profile remains heavily concentrated among a limited number of customers—a structural risk that could impact financial stability should these relationships shift unfavorably. One third-party customer alone represented approximately 40% of total revenues during fiscal year 2025; combined with one related party customer accounting for an additional 36%, these two clients made up nearly three-quarters of sales [S4][S11]. Furthermore, accounts receivable exposure affirms this concentration risk—with two customers accounting for roughly two-thirds of outstanding receivables [S12].

While supply contracts with entities like VSUN provide some order visibility and mitigate short-term volatility concerns [S4][S11], dependency on few large clients intrinsically elevates counterparty risk. Any reduction or delay in orders by these cornerstone customers could sharply affect profitability given the fixed nature of capital-intensive solar manufacturing operations.

Liquidity and Working Capital Concerns

Despite strong operating cash flows—$133 million generated in FY2025 compared to $46.5 million the previous year—TOYO faces significant liquidity pressure driven primarily by large working capital deficits [F1][S6][S8]. As of December 31, 2025, current liabilities ($295.7 million) substantially outpaced current assets ($171.8 million), resulting in a current ratio of just around 0.58—a level well below conventional thresholds for comfortable short-term coverage [F1].

This deficit is exacerbated by substantial payables to related parties amounting to over $62 million that may be extended upon maturity but are nonetheless present on the balance sheet [S8]. Contract liabilities totaling approximately $108 million indicate expected settlement through future revenue recognition but represent near-term cash outflow commitments [S10]. Capital expenditures ballooned to nearly $92 million in FY2025 as part of aggressive capacity build-out efforts—more than doubling prior year spend—and continue to weigh on free cash flow despite robust cash generation [F1][S14][S22].

TOYO’s ability to secure funding from related parties alongside outside investors remains critical to addressing these working capital constraints and sustaining growth initiatives [S6][S8][S10]. Management acknowledges that maintaining this liquidity balance is essential for going concern viability while actively pursuing external financing alternatives.

US Manufacturing Plant Acquisition and Strategic Implications

A pivotal aspect of TOYO's strategic growth is its recent acquisition of Solar Plus Technology Texas LLC and commissioning a state-of-the-art photovoltaic module manufacturing plant in Houston with a capacity of approximately one gigawatt [S1][S24]. This move explicitly targets strengthening local US production amid shifting solar supply chain dynamics influenced by geopolitical considerations.

Localizing module production serves dual purposes: it reduces exposure to international supply disruptions and aligns TOYO closer to a key revenue market where it derived most sales ($341 million out of $427 million total revenue in FY2025) [S17]. This enhanced footprint complements existing facilities abroad while positioning TOYO favorably against competitors navigating similar reshoring trends.

Operational Efficiency and Production Utilization Insights

Full utilization rates achieved at both the Vietnam (2GW) and Ethiopia (4GW) solar cell plants underscore the company's operational scalability during this stage of capacity ramp-up [S1]. Capturing economies at these facilities supports cost absorption critical for margin improvements as fixed assets are leveraged.

Nevertheless, tight production bandwidth leaves limited headroom for unexpected demand surges or flexibility adjustments without further investment or OEM channel rerouting strategies—highlighting an operational discipline imperative alongside growth.[S1]

Leadership Shift Reflecting Strategic Recalibration

In March 2026 a leadership transition saw CEO Junsei Ryu resign without dispute pertaining to operational direction or policy matters; successor Takahiko Onozuka was appointed CEO concurrently serving as Chairman of the Board [S2][S3].

Mr. Onozuka brings over four decades of global experience in energy infrastructure finance including project origination for significant independent power projects across Asia and beyond—a profile well-suited for stewarding TOYO amid capital intensity and decarbonization imperatives. His credentials incorporate roles at Japan’s Export-Import Bank focusing on structured finance and renewable initiatives coupled with executive responsibilities overseeing decarbonization strategies at Abalance Corporation prior to joining TOYO.

This leadership change appears poised to sharpen corporate governance focus while leveraging deep sector knowledge vital for navigating competitive dynamics and evolving regulatory environments.[S2][S3]

Capital Allocation Profile: Returns, Cash Flow, and Equity Deployment

TOYO delivered a reported return on equity near an estimated 35.6% in FY2025 when comparing annual net income ($39.7 million) against year-end equity balances ($111.3 million)—a robust indicator given current business scale [F1]. However, net income slightly declined by about -2.3% versus prior year due mainly to expanded costs accompanying capacity expansion.

Operating cash flow surged +186% year-over-year highlighting underlying cash-generative capability despite significant capital expenditures which catapulted +116% reaching nearly $92 million invested primarily toward plant acquisitions and upgrades [F1][S14][S22]. The resultant free cash flow approximated $41 million positive albeit weighted by timing differences inherent in capex cycles.

Equity injections persisted during this period via share issuance mechanisms aligned with escrow agreements supporting business combination structures; although details imply limited dilution pressures presently while providing necessary liquidity buffers [S29]. Buyer-side vigilance should monitor capital raises closely given ongoing sizable funding requirements.

Outlook: Competitive Positioning Against Sector Headwinds (Analysis)

Looking ahead, TOYO occupies a strategically advantageous position through integrated solar manufacturing capabilities augmented by geographic diversification encompassing Vietnam, Ethiopia, Singapore, China, Japan alongside core US market presence. Yet persistent customer concentration restrains risk diversification — reliance on anchor clients like VSUN creates vulnerability needing mitigation through broader commercial wins.

Currency exposures remain relevant given that revenues are predominantly USD-denominated whereas costs span multiple currencies including Vietnamese Dong and Renminbi—realizing FX management as an operational priority.[S12]

The balancing act will involve leveraging scale economies from full capacity utilization while ensuring sufficient liquidity via strengthened capital partnerships or debt instruments capable of funding continued expansion without jeopardizing solvency metrics highlighted by onerous working capital deficits.[F1][S6]

Competitive sustainability will likely hinge on innovation within cell efficiency parameters combined with flexible OEM partnerships enabling responsiveness amid fluctuating demand patterns nationally and internationally.

Disclaimer: This report synthesizes publicly available information including SEC filings but does not constitute investment advice or endorsement regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments