MicroAlgo Inc. Rebounds to Profitability with Strategic Shift Away from Intelligent Chips

MicroAlgo Inc.'s financial recovery reflects a strategic realignment toward central processing algorithm services amid market headwinds.

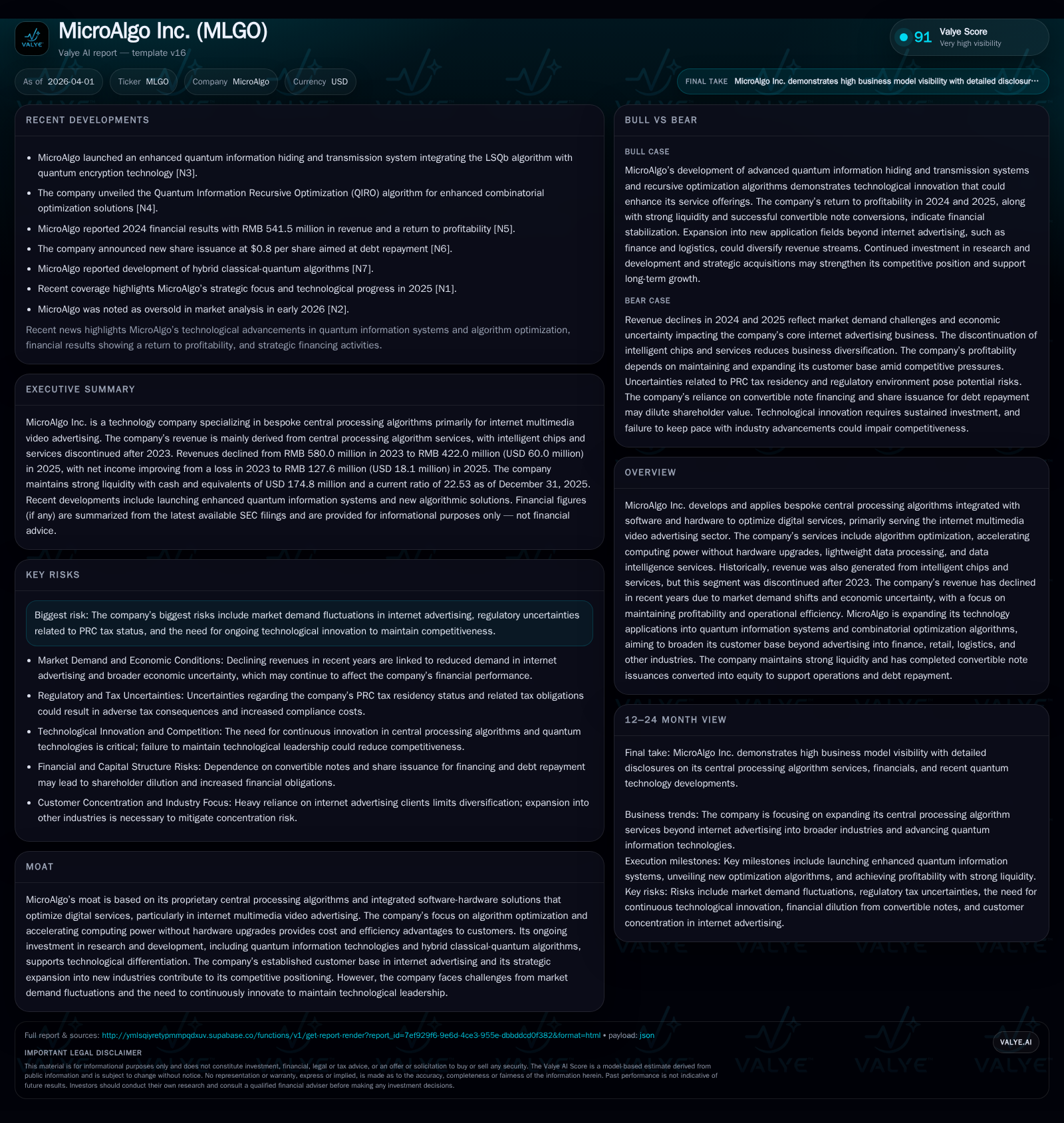

MicroAlgo Inc., a specialist in bespoke central processing algorithms primarily serving internet multimedia video advertising, experienced declining revenues from 2023 to 2025 due to market demand shifts and the discontinuation of its intelligent chips segment. However, the company returned to net profitability in 2024 and significantly improved results in 2025 by focusing on its core algorithm services and investing in AI and quantum technology. Despite revenue contraction, MicroAlgo maintains a strong liquidity position with substantial cash reserves and is executing share restructurings to comply with Nasdaq requirements. Growth prospects hinge on expanding applications beyond advertising into finance, retail, and logistics while navigating regulatory uncertainties related to PRC tax status and capital controls.

Company Overview and Historical Performance

MicroAlgo Inc., listed on Nasdaq under ticker MLGO since December 2022, specializes in the development of bespoke central processing algorithms integrated with both software and hardware solutions. Historically a hybrid model that included intelligent chips manufacturing alongside algorithm services, MicroAlgo divested its intelligent chips subsidiaries post-2023 to concentrate exclusively on its central processing algorithm services aimed primarily at the internet multimedia video advertising sector [S1][S6].

The company's revenues have seen notable contraction over recent years amid macroeconomic challenges impacting client marketing budgets globally. Recorded top-line figures stood at approximately USD 87.1 million in FY22, followed by steady declines: USD 81.9 million in FY23, USD 75.3 million in FY24, culminating at USD 60.0 million in FY25 — a near-31% reduction over three years [F1][S16].

Simultaneously, MicroAlgo experienced a turnaround from significant net losses (-USD 37.6M, FY23) to profitability with net income climbing from USD 7.3M in FY24 to USD 18.1M in FY25 [F1][S6]. Operating income mirrored this trend, moving from negative territory in FY23 (-7.9M) into modestly positive figures—approximate USD 3.2M in FY25 [F1]. This improvement was enabled by aggressive cost restructuring including a nearly halved research & development spend as R&D projects matured or completed [S5][S8].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 60 | 18 | 2 | 3 | -20.3% | +149.0% |

| 2024 | 75 | 7 | 4 | 3 | -8.0% | +119.4% |

| 2023 | 82 | -38 | -6 | -35 | -6.0% | -439.7% |

| 2022 | 87 | -7 | 2 | -8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 5.5 |

| 2024 | 5.0 |

| 2023 | -82.8 |

| 2022 | -10.4 |

Source: SEC companyfacts cache [F1].

*Includes goodwill impairments and stock compensation expenses that boosted operating losses [S5].

Drivers Behind Past Performance

Revenue decline is primarily linked to shifts in market demand within internet advertising driven by tightening corporate marketing budgets amid global economic uncertainty during the referenced period [S16]. Additionally, disposal of the intelligent chips segment eliminated an approximate USD ~1-2 million revenue source post-2023 but allowed sharper focus on core competencies [S1][S16].

Operational improvements stemmed from strict cost management including reduced R&D expenses as certain projects wrapped up—transitioning toward newer AI-enhanced algorithmic capabilities—and efficiencies gained across selling and administrative functions [S5]. Reduction of intangible asset impairments and elimination of stock-based compensation charges also reflected gains compared with prior loss-ridden year [S5].

Future Growth Prospects

MicroAlgo aims to expand application fields for its central processing algorithms beyond traditional internet advertisement clients into adjacent sectors such as finance, retail, logistics, manufacturing, and even local government entities that contest with rapidly growing data volumes requiring optimized computation resources [S6][N1]. Research efforts are increasingly focused on integrating artificial intelligence advancements alongside explorations into quantum-information-based combinatorial optimization algorithms that may provide differentiated computing efficiency without hardware upgrades [N1][S8]. The company highlights these innovations as potential competitive moats.

However, cautious budget allocations across client industries given economic conditions may still cap short-term top-line growth [S23]. The company also encounters regulatory risks rooted chiefly in potential classification as a PRC tax resident enterprise under China’s Enterprise Income Tax Law based on "de facto management body" criteria—a status that could impact worldwide taxable income assessments [S1]. Furthermore, tightening foreign exchange controls imposed by Chinese authorities complicate capital flows which may restrain outbound dividend payments or capital expenditures despite healthy cash reserves [S10][S15].

Forecasts and Key Milestones

While explicit forward-looking guidance was not provided for fiscal year beyond December 31, 2025 [N1], monitoring metrics will include:

- Revenue recovery trajectory amid expansion into new industry verticals.

- Evolution of R&D investment focused on AI and quantum computing integrations.

- Client base diversification measured against internet advertisement dependency.

- Regulatory developments regarding tax residency and capital restrictions.

- Successful capitalization on acquisition or partnership opportunities within the central processing algorithm space.

Industry analysts should watch updates from MicroAlgo’s quarterly releases or investor communications around these strategic inflection points.

Capital Allocation and Financial Returns

MicroAlgo's capital management reflects prudent stewardship characterized by no dividends paid historically or forecasted given reinvestment priorities for growth technologies [S9]. The company undertook multiple rounds of share consolidations between early-2024 through mid-2025 designed to maintain compliance with Nasdaq listing rules — notably involving changes converting ordinary shares into dual-class structures with varied voting rights increasing authorized capital substantially before effectuating reductions back down while increasing par value per share for simplification [S3][S9]. These actions potentially dilute share count but enable enhanced governance control mechanisms beneficial for long-term value creation.

Liquidity remains robust with cash & equivalents at approximately USD 174.8 million as of year-end 2025 along with a strong current ratio exceeding twenty-to-one — signaling comfortable coverage of short-term liabilities totaling about USD 15.5 million [F1][S7][S12]. Operating cash flow is positive but modest (approximately USD 2.5 million), declining somewhat year-over-year consistent with lower revenues yet adequate for sustaining ongoing R&D efforts without prompting immediate external funding needs [F1][S13][S25]. Free cash flow remains positive albeit limited due to continued capital expenditure commitments related to platform enhancements.

Return on equity stands near about five-and-a-half percent based on latest net income relative to equity balances showing expansion since negative returns during loss-making periods—this improving profit generation supports perceptions of restored operational leverage following transformation initiatives [F1].

Industry Positioning and Moat Analysis

MicroAlgo’s moat stems principally from its proprietary integration of central processing algorithms with customizable software-and-hardware solutions enhancing digital service efficiency especially for high-demand data environments such as video advertising platforms [N1][S1]. Its ability to accelerate computing power without necessitating extensive hardware upgrades offers cost savings valued by customers seeking scalable data intelligence services [S14]. Coupled with ongoing R&D initiatives targeting next-generation quantum computing approaches, this technological edge underpins customer loyalty within existing markets while framing pathways into lucrative adjacent sectors requiring advanced data empowerment solutions.

Nevertheless, sustainability of this competitive advantage hinges on continuous innovation alongside agile market adaptation amid fluctuating demand patterns typical for internet-based advertisement-focused enterprises—and regulatory complexities concentrated around jurisdictional tax treatments present further hurdles for cross-border enterprise structures common among Chinese-adjacent tech companies listed overseas [S1][S15].

Conclusion

Following marked temporal setbacks during the COVID-19 era reflected sharply reduced revenues accompanied by high impairment charges ending FY23 at large net losses, MicroAlgo has reoriented strategically toward revenue concentration solely on its central processing algorithm business serves broadening industry sectors beyond its Internet Multimedia Video Advertising roots while trimming costs mainly via focused R&D spend rationalization.

Despite declining top-line trends through fiscal 2025 due to external macroeconomic conservatism compressing marketing budgets across customer verticals, the company successfully achieved net profitability restoration driven by operational discipline; enjoys strong liquidity footing supporting further technology investments; executed equity restructuring safeguarding Nasdaq listing eligibility; and pursues expanding addressable markets via AI-enabled quantum processes.

Investors should monitor how effectively the company penetrates new customer segments outside online digital ads amid emerging regulatory scrutiny over PRC residency status affecting global tax exposure alongside adherence to evolving foreign exchange regulations that could influence cross-border fund flows critical for continued strategic flexibility.

This analysis is based solely on publicly available information including filings up through April 1st, 2026; it excludes investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments