AbbVie Inc.'s Financial Rebound and Strategic Pipeline Anchors Growth Outlook

AbbVie rebounds strongly in FY2025 with robust revenue growth and a strengthened pipeline focused on immunology and oncology, supported by active capital deployment amidst liquidity and regulatory challenges.

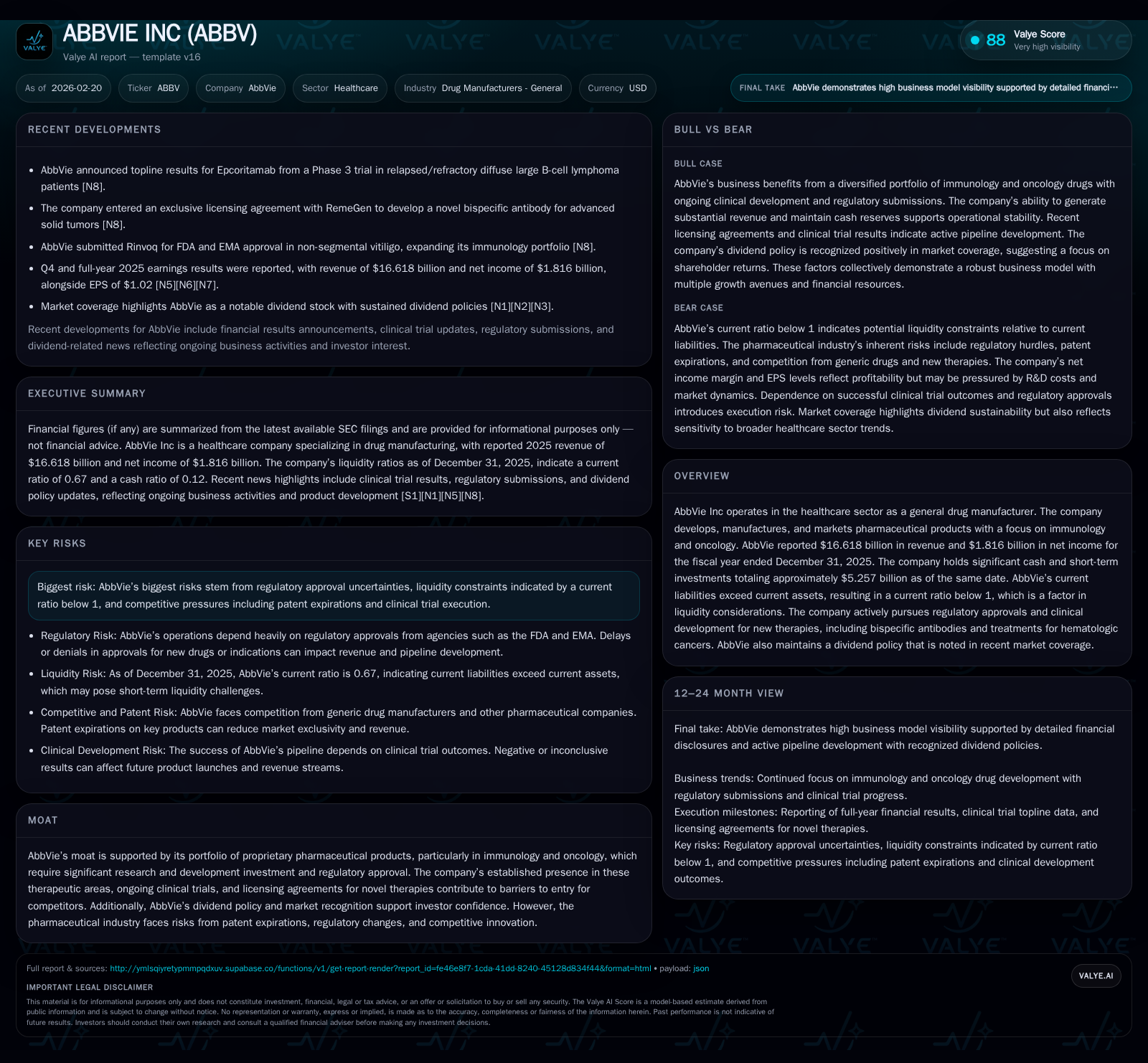

AbbVie Inc. demonstrated a significant financial turnaround in fiscal 2025, posting over $16.6 billion in revenue—a 10% increase year-over-year—and recovering net income to positive territory after prior losses. This rebound reflects operational leverage and strategic focus on immunology and oncology pipelines, including promising Phase 3 trial results for bispecific antibodies targeting hematologic cancers. Despite robust operating cash flow and ongoing dividends, the company faces headwinds from patent cliffs, regulatory uncertainties, and a current ratio below 1 indicating liquidity constraints. Capital allocation has balanced dividend commitments with tempered buybacks amid debt maturity considerations. Key upcoming clinical milestones will be crucial signals for sustained momentum in this competitive pharmaceutical landscape.

Revenue and Income Recovery: Tracing FY2025 Performance

AbbVie’s fiscal year ended December 31, 2025, marks a significant inflection point after previous volatility marked by narrow or negative net earnings. The company reported revenues of approximately $16.62 billion, reflecting a solid 10% increase compared to $15.10 billion in FY2024 [F1]. This top-line acceleration is underpinned by strong performance in immunology and oncology therapeutic areas where AbbVie maintains exclusive franchises.

Operating income saw an even more pronounced recovery, surging by nearly two-thirds (+65%) to reach $15.08 billion after dipping to $9.14 billion the year before [F1]. This implies not only volume growth but enhanced operational leverage helped absorb R&D expenditures amidst evolving pipeline investments.

Most notably, net income swung back into positive territory at $1.82 billion—up from a nominal loss of $22 million in FY2024—an extraordinary gain of over 8300% YoY [F1]. This normalization reflects reduced one-time charges or impairments impacting prior periods and validates underlying business resilience.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 16.6 | 1.8 | 19.0 | 15.1 | +10.0% | +8354.5% |

| 2024 | 15.1 | -0.0 | 18.8 | 9.1 | +5.6% | -102.7% |

| 2023 | 14.3 | 0.8 | 22.8 | 12.8 | -5.4% | -66.8% |

| 2022 | 15.1 | 2.5 | 24.9 | 18.1 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 11.7 | 980 | 17.8 |

| 2024 | 11.0 | 1708 | 17.8 |

| 2023 | 10.5 | 1972 | 22.1 |

| 2022 | 10.0 | 1487 | 24.2 |

Source: SEC companyfacts cache [F1].

Note: Buybacks omitted from table due to quarterly timing; ROE excluded due to negative equity balance.

Expansion Drivers: Clinical Innovations and Pipeline Advancements

AbbVie’s strategic pivot toward next-generation therapies in immunology and oncology is bearing tangible fruit with several advanced clinical trial programs nearing potential approval phases [S6]. A key highlight is the Phase 3 EPCORE DLBCL-1 trial with Epcoritamab—a bispecific antibody targeting CD3xCD20 antigens—intended for treatment-resistant diffuse large B-cell lymphoma patients, which recently reported encouraging topline efficacy outcomes [N6]. Such clinically differentiated assets address significant unmet needs with potential blockbuster market penetration.

Further pipeline developments encompass multiple bispecific antibodies acting via dual tumor antigen engagement mechanisms designed to improve therapeutic index profiles over conventional biologics [S6]. This aligns well with industry trends prioritizing molecular precision therapies supported by rigorous FDA scrutiny involving complex endpoints.

Market analysts emphasize AbbVie's inherited immunology portfolio's robust position but also acknowledge that new launches like Epcoritamab could decisively lift mid-term revenue trajectories given successful regulatory milestones and adoption dynamics worldwide [N9]. The continuity of innovation within these core franchises remains indispensable as patent cliffs pressure legacy drugs.

Assessing Mid-term Growth Opportunities and Industry Constraints

While the clinical pipeline offers upside potential, AbbVie remains subject to classic pharmaceutical sector headwinds outlined explicitly in recent risk disclosures: regulatory approval uncertainties, intensified competition from biosimilars/generics following patent expirations, pricing pressures especially in U.S markets, and the inherent unpredictability of late-stage clinical trial outcomes [S4][S5]. Management also notes ongoing global macroeconomic and healthcare policy variables that could impact demand elasticity.

The patent expirations on several older molecules necessitate balanced R&D expenditure prudence while maintaining aggressive clinical development timelines for novel compounds to offset volumes lost post-exclusivity lapses.

Investment literature suggests immunology indications will continue contributing substantially but incremental gains from oncology bispecific antibodies must meet elevated safety-efficacy thresholds set by regulators to translate into meaningful market share expansions [N9]. Consequently, the growth outlook is cautiously optimistic but hinges on successful execution across multiple developmental fronts.

Capital Allocation Overview: Dividends, Buybacks, and Debt Management

In FY2025 AbbVie upheld a shareholder-friendly capital allocation approach with sizable dividends disbursed totaling approximately $11.66 billion—up modestly from prior years—highlighting consistent commitment despite mixed earnings history [F1][N11][N13]. Share repurchase activity moderated significantly to about $980 million compared to earlier years exceeding $1 billion annually [F1], likely reflecting shifts in free cash flow prioritization amid ongoing balance sheet refinements.

The firm's return-on-equity calculation stands distorted due to a negative shareholders' equity balance of approximately -$3.27 billion at year-end 2025 following accumulated deficit effects primarily linked to goodwill impairments or restructuring charges incurred over preceding periods [F1]. Thus, traditional ROE metrics are less instructive here.

Debt maturities through staggered senior notes ranging from 2027 to 2031 appear manageable per recent filings [S7][S8][S9], providing timing flexibility for refinancing or deleveraging where prudent without immediate straining.

Overall, AbbVie balances yield maintenance (dividend yields remain attractive relative to cash flows) against cautious buyback resumption synchronized with leverage targets—reflecting a calibrated capital recycling philosophy suitable for late-cycle pharma enterprises facing patent expiries yet investing heavily in innovation.

Liquidity Status and Balance Sheet Dynamics

Liquidity analysis reveals the company's current ratio rests at roughly 0.67—current assets stand at about $29 billion vis-à-vis current liabilities approximating $43 billion as of December-end 2025 [F1]. While sub-1 ratios often flag short-term coverage insufficiency concerns, it’s essential here this imbalance partly reflects sizable deferred tax liabilities or accrued expenses typical in large pharma firms managing complex legal and regulatory provisions.[S7]

Moreover, AbbVie's cash reserves include over $5 billion in cash and cash equivalents plus highly liquid short-term investments that help offset near-term obligations easing funding risks.[F1] Nonetheless, this working capital dynamic warrants monitoring for operational flexibility preservation especially should unforeseen accelerated payables arise.

The substantial scale of operating cash flow—around $19 billion annually—further buttresses liquidity frameworks bolstering creditor confidence despite the compressed current ratio.[F1]

What to Watch: Upcoming Milestones and Regulatory Developments

Given the absence of detailed forward-looking guidance outside general earnings outlooks published earlier this year [N3], investors and analysts should particularly track critical regulatory filings for key innovation drivers such as bispecific antibodies like Epcoritamab aimed at hematologic malignancies expected over the next few quarters.[N6]

Additionally, continued clinical data readouts from ongoing trials across oncology indications alongside submission progressions will materially influence AbbVie's commercial expansion scope.[N9]

Monitoring generic/biosimilar threats emerging within legacy immunology treatments remains essential considering patent cliff impacts discussed extensively in risk disclosures.[S4][S5]

Engagement with FDA decisions on label expansions or fast-track designations can accelerate market adoption curves thereby materially affecting near- to mid-term revenue streams.

Disclaimer: This analysis does not constitute investment advice or recommendations but aims to provide an informed overview based on publicly available documents and acknowledged sector dynamics as of February 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments