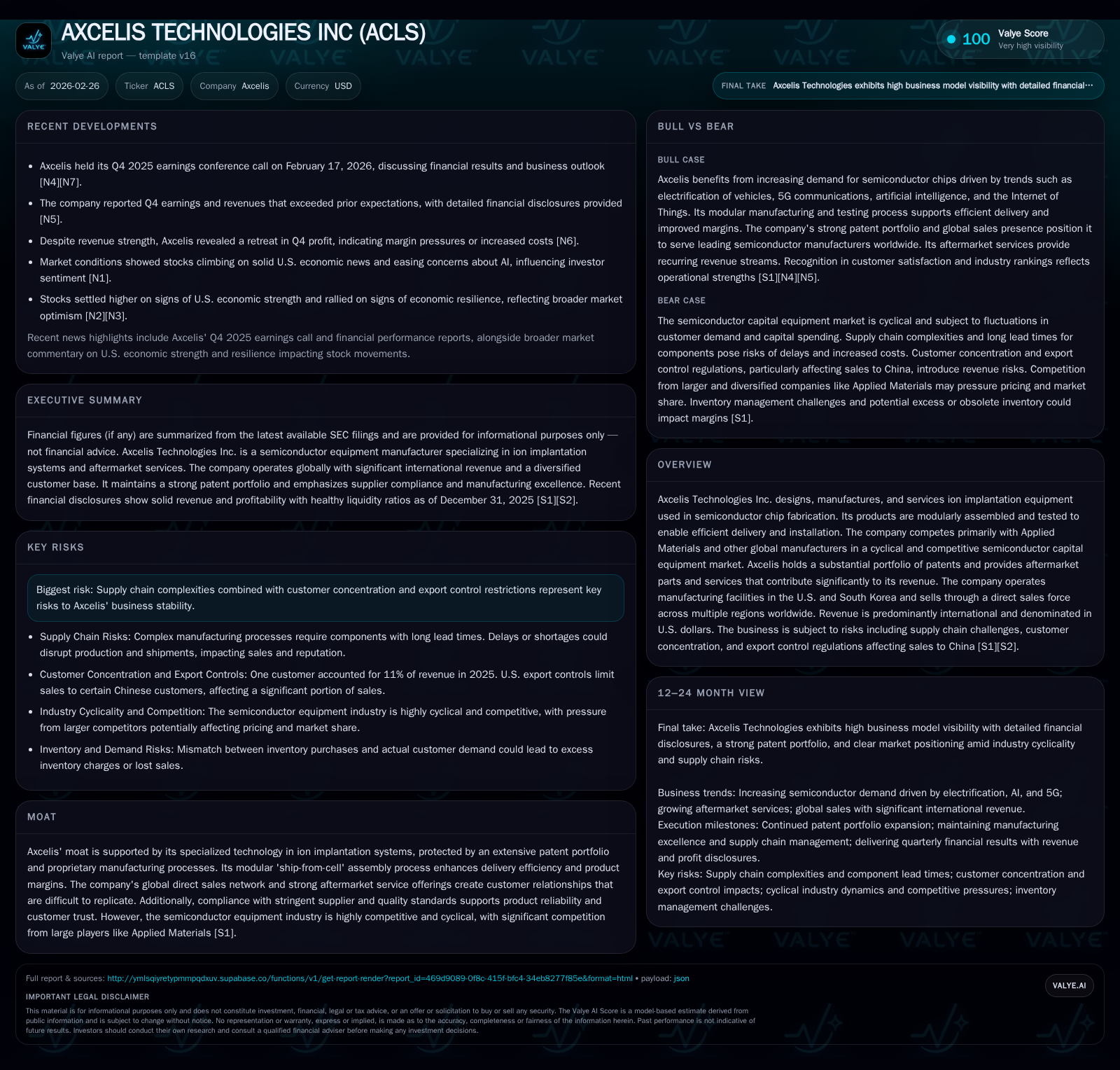

Axcelis Technologies' Strategic Reset After Semiconductor Market Headwinds

Axcelis confronts a cyclical semiconductor equipment downturn through innovation, operational discipline, and focused capital deployment.

In FY2025, Axcelis Technologies experienced a substantial revenue decline of 17.6% and operating income contraction of 43.4%, driven by intensifying competition and U.S. export controls restricting sales to China. The company is leveraging its specialized ion implantation technology, modular assembly processes, and robust patent portfolio to sustain market presence while targeting growth in advanced logic segments and aftermarket services. Capital allocation remains disciplined with notable share repurchases and sustained R&D investment to fuel innovation and margin improvement. Customer concentration and geopolitical complexities present ongoing risks to top-line stability, making monitoring backlog trends and regulatory shifts critical for near-term outlook.

Financial Momentum and Industry Headwinds in FY2025

Axcelis Technologies navigated a challenging fiscal year in 2025 marked by pronounced semiconductor industry cyclicality that materially impacted its financial performance. Total revenue retreated sharply by approximately 17.6%, falling from about $1.02 billion in FY2024 to $839 million in FY2025 [F1]. This decline reflects softer capital equipment demand as chipmakers moderated investment amid high inventory levels and geopolitical uncertainties.

Operating income fell even more steeply by roughly 43.4%, dropping to $119.3 million from $210.8 million year-over-year [F1]. The disproportionate contraction suggests significant margin compression affected by pricing pressures and under-absorbed fixed costs intrinsic to the semiconductor capital equipment sector's fixed-cost base. Net income similarly followed the downward trend, settling at around $120 million [F1].

Despite the top-line contraction, Axcelis maintained positive operating cash flow at $118.3 million for the year—down about 16%—which after modest capex spending of nearly $11.3 million resulted in free cash flow generation north of $107 million [F1]. The company kept capital expenditures tightly controlled, decreasing capex by over 7% compared to the prior year, underlining rigorous cost management during cyclical softness [F1].

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 839 | 118 | 119 | 11 | -17.6% |

| 2024 | 1018 | 141 | 211 | 12 | -10.0% |

| 2023 | 1131 | 157 | 266 | 21 | +22.9% |

| 2022 | 920 | 216 | 212 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 121 | 107 |

| 2024 | 60 | 129 |

| 2023 | 52 | 136 |

| 2022 | 57 | 205 |

Source: SEC companyfacts cache [F1].

Data illustrates magnitude of declines in core earnings against relatively stable capital deployment trends for context on firm resilience.

Drivers Behind Revenue Contraction: Competitive and Geopolitical Factors

Several intersecting factors contributed to the pronounced top-line pressure observed during FY2025. Chief among these was escalating competition from industry giant Applied Materials, which possesses broader financial resources and a wider product suite challenging Axcelis’ specialized ion implant segment [S5]. Although Axcelis maintains a viable moat through its ion implantation technology uniquely protected by an expansive patent portfolio exceeding hundreds of active patents globally [S13], competing incumbents continue pressing price-performance improvements.

Geopolitics notably shaped sales trends given that Chinese customers historically represented a sizable portion of total revenue—reflecting Asia’s dominance with approximately 76% of system sales directed there [S8][S10]. The imposition of strict U.S. export controls since late-2022 affects shipments to Chinese wafer fabrication plants engaged in advanced logic device manufacturing or using certain ion implant parameters [S19]. One major client, Semiconductor Manufacturing International Corporation (SMIC), remains on the U.S. Entity List subject to licensing restrictions that Axcelis has largely been able to navigate; however, broader access constraints increased uncertainty on continued revenue streams from Chinese fabs [S4][S17].

Customer concentration risk is non-trivial: the top ten customers accounted for over 55% of net sales last year compared with under 50% previously; one single customer accounted for approximately 11% of total revenues in FY2025 [S4][S5]. This concentration intensifies vulnerability to order deferrals or supplier substitution amidst geopolitical tensions.

Additionally, supply chain complexities have slightly delayed deliveries while increased component costs have pressured margins despite limited ability to escalate pricing considering market dynamics [S8].

Growth Enablers and Market Opportunities Going Forward

Amid these headwinds, Axcelis is pursuing targeted growth levers grounded in product innovation and service excellence. Central to this strategy is the Purion line of ion implantation systems designed for better energy efficiency and lower cost of ownership relative to legacy platforms—factors highly valued by fabs optimizing throughput-per-watt metrics [S18][N1]. The Purion M variant also suits high-altitude fabs or those processing heavier ions due to its superior energy capability beyond competitors.

Axcelis frames these initiatives within the "DVS" framework—differentiated, valuable, and sustainable solutions—which resonates well among semiconductor capital equipment buyers seeking lasting productivity advantages [S6].

Geographically, Japan represents a key emerging market focus alongside expansion efforts into advanced logic segments where demand resilience tends to outperform older memory or commodity wafer fabs [S6][N1]. Beyond incremental organic growth, corporate development initiatives aimed at adjacent technologies beyond pure ion implantation were discussed but remain nascent.

Approximately one-third of revenue comes from aftermarket parts and service contracts—a comparatively stable segment generating recurring cash flow that cushions cyclical swings in new system orders [S18]. Continued enhancement of aftermarket offerings via programs like Managed Inventory service strengthens client relationships and recurring revenue streams.

Critical Operational Initiatives: Modular Assembly and Product Differentiation

Axcelis benefits from a proprietary "ship-from-cell" modular assembly process tailored to accelerate system delivery timelines without sacrificing reliability—an operational edge in an industry where lead time drives fab capacity planning [S15]. By testing modules incrementally with customized test stands and software before full system installation onsite, cycle times shrink markedly improving inventory turns.

The company's manufacturing footprint spans a large ISO-certified plant in Beverly, Massachusetts (~417K sq ft), supplemented by its Asian Operations Center in South Korea benefiting from lean manufacturing techniques like Six Sigma quality control standards [S6][S15]. This global manufacturing collaboration coupled with tight engineering-marketing integration shortens development cycles enhancing time-to-market for innovations.

Intellectual property protection remains fundamental: as of December 31, 2025 Axcelis held approximately 169 active U.S patents along with more than three hundred foreign patents ensuring technological barriers against competitive imitation while fostering iterative upgrades sustaining product relevance [S13].

Capital Deployment Strategy: Buybacks, R&D, and Cash Flow Generation

Axcelis exhibits disciplined capital stewardship balancing reinvestment with shareholder value return through buybacks rather than dividends—a common preference among smaller tech equipment firms aiming for growth rather than yield payouts [F1][S28]. In FY2025 alone it repurchased approximately $121 million worth of shares, roughly double the prior year's level underscoring aggressive return amid lower earnings [F1].

Research & Development spend rose modestly reaching $109 million or around 13% of revenue reflecting commitment toward maintaining competitive product differentiation illustrated by recent launches such as Purion family systems [S7][N1]. Concurrently capex expenditures remained moderate at ~$11 million focused mainly on sustaining production capabilities rather than incremental capacity expansion given current demand softness [F1][S6].

Management employs "Design for X" (DfX) strategies encompassing manufacturability, cost optimization and quality enhancements allowing continuous gross margin improvement despite cyclical headwinds—a sophisticated approach enhancing long-term profitability leverage within fixed-cost structures typical of semiconductor tooling operations [S6].

Risks from Customer Concentration and Export Controls

The underlying business model faces significant risks tied primarily to high customer concentration where reliance on a handful of large fabs amplifies sensitivity to order timing variations or strategic shifts away from Axcelis products [S4][S5]. Deterioration or loss of any major account could rapidly depress revenues given no multi-year contracts mandate purchases.

Export controls represent another critical challenge particularly involving China-based clients subject to layered U.S.-led regulatory frameworks increasingly stringent since mid-2020s expansions. While licenses have allowed continued shipments selectively—especially mature node fabs operated by SMIC—the regulatory environment remains fluid creating potential disruption if policies tighten further beyond current thresholds [S17][S19][N10].

Supply chain fragility elevates operational risks as some specialized components possess few alternative sources; delays or cost inflation therein may hinder timely fulfillment while eroding margins absent offsetting price actions which are constrained competitively [S8][S20].

Outlook at Customer Demand Patterns and Backlog Trends

As of December end-2025 backlog stood at about $457 million down considerably from nearly $646 million a year prior indicating diminished near-term customer commitments reflecting chip fab investment caution [S16][F1]. However bookings accelerated late in calendar Q4 — rising above comparable Q4 last year levels — suggesting stabilizing demand as customers recalibrate deployment plans amid easing AI-related excitement jitter effects on semi capex cycles [N1][N7][N8][N9].

Management commentary highlights ongoing market uncertainty but expresses cautious optimism around sustaining order flows especially driven by strategic wins with Purion platforms in Japan plus revamped aftermarket contracts aiming at steady repetition business over multiyear horizons [N1][S27]. Margin outlook remains challenged though targeted operational improvements seek gradual restoration over fiscal '26 guided by disciplined spend controls aligned with evolving market patterns.

Evaluating Shareholder Returns: ROE, Dividends, and Repurchase Activities

Surprisingly resilient return metrics emerge despite top-line contraction with approximate annual ROE hovering around a respectable ~11.6%, aided by high equity base expansion over prior years as retained earnings build gradually even through cyclical troughs [F1]. There is no indication that Axcelis pays cash dividends; instead capital returns prioritize share repurchases—with FY25’s buyback program effectively doubling previous years’ magnitude underscoring management’s focus on stock price support amid uncertain growth visibility [F1][S28].

Free cash flow continues robust generation exceeding $100 million annually facilitating this buyback cadence alongside capex-restricted spending policies demonstrating internal liquidity strength underpinning operational agility during fluctuating cycle phases.

Disclaimer: This analysis is based solely on publicly available data as of February 26, 2026, including SEC filings and company disclosures combined with sector-sensitive interpretations; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments