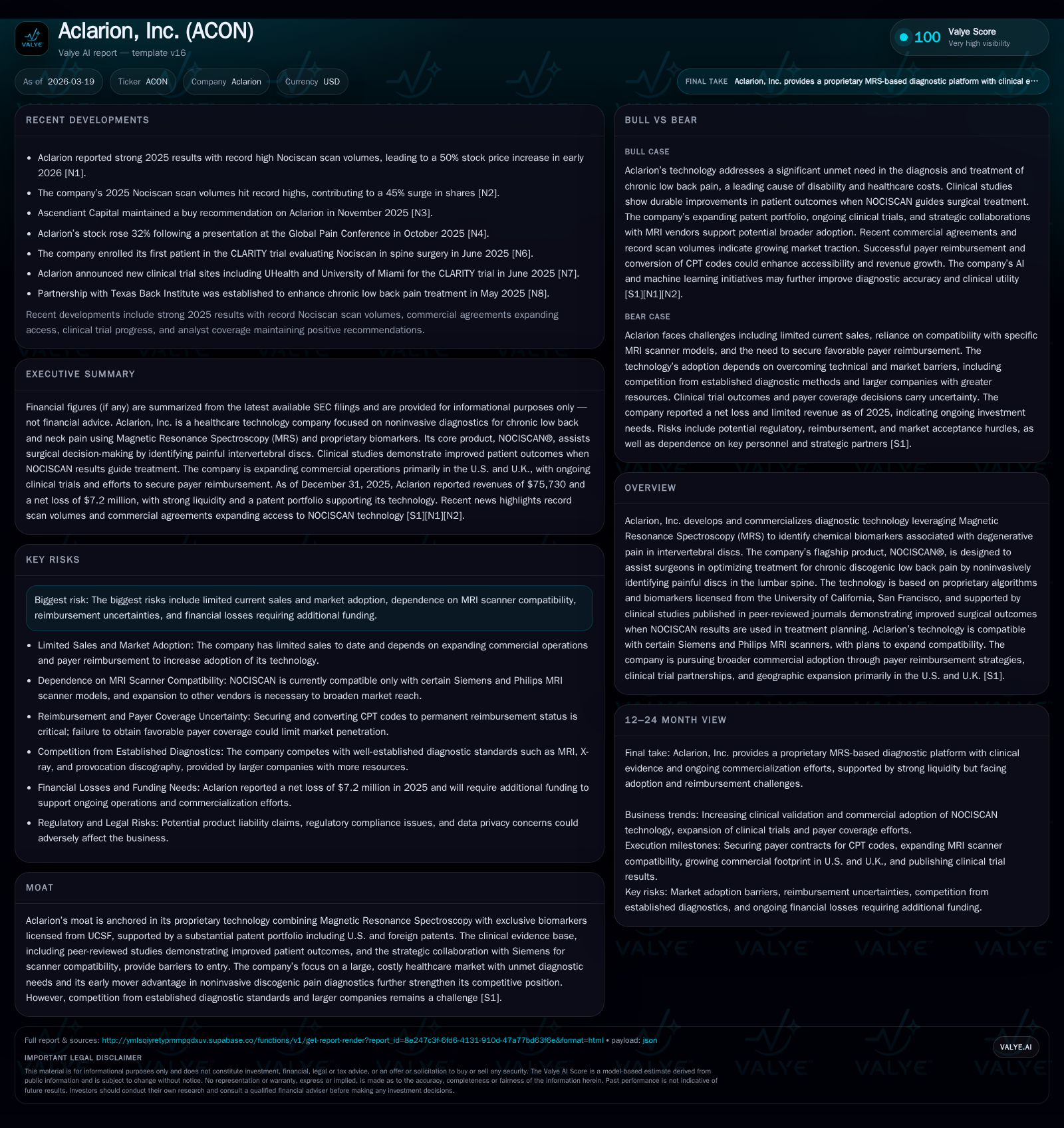

Aclarion, Inc. Tackles Chronic Low Back Pain Diagnostics with Proprietary MRS Technology

Aclarion spearheads innovation in chronic low back pain diagnostics through its unique Magnetic Resonance Spectroscopy platform combined with exclusive biomarkers.

Chronic low back pain represents a significant medical and economic burden in the U.S., and Aclarion, Inc. has developed a proprietary diagnostic technology leveraging Magnetic Resonance Spectroscopy (MRS) coupled with licensed biomarkers from UCSF. Its flagship product, NOCISCAN®, offers surgeons noninvasive chemical biomarker detection to identify painful lumbar discs, supported by clinical studies that demonstrate improved surgical outcomes. Despite promising technology and growth in revenues driven by expanding market traction and scanner compatibility partnerships, Aclarion continues to grapple with operating losses, reimbursement challenges, and limited current adoption. The company’s future hinges on broadening scanner compatibility, securing permanent CPT code coverage, expanding clinical indications, and navigating complex regulatory and compliance landscapes.

Historical Revenue Trends and Operating Performance Dynamics

Aclarion's financial performance over recent years reflects the early commercialization stage typical of innovative medtech companies. Fiscal year 2025 closed with revenues of USD 75.7 thousand—a significant increase of 65.6% compared to FY2024’s USD 45.7 thousand and roughly in line with FY2023's USD 75.4 thousand [F1]. This growth signals initial traction as the company expands clinical deployment.

Despite revenue gains, operating income declined further into negative territory at USD -7.05 million for FY2025 compared to USD -5.51 million the prior year—a near 28% increase in operating losses year-over-year [F1]. Net income showed similar trends with losses of USD -7.23 million versus USD -6.99 million in FY2024 [F1]. Operating cash flow was also substantially negative at USD -7.16 million for the year while capital expenditures rose sharply to USD 21.5 thousand from just over USD 5 thousand the previous year [F1], resulting in a free cash flow deficit exceeding USD -7 million.

The balance sheet remains relatively strong with cash and equivalents of approximately USD 12 million at year-end and a high current ratio of about 14.8x due to low current liabilities under USD 0.84 million—providing runway amid continuing losses [F1]. Shareholders’ equity improved significantly to over USD 12.8 million by end-2025 after previous years of negative equity balances, reflecting recent capital raises.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 75730 | -7 | -7 | -7 | +65.6% | -3.4% |

| 2024 | 45724 | -7 | -5 | -6 | -39.4% | -42.4% |

| 2023 | 75404 | -5 | -4 | -5 | +24.8% | +30.5% |

| 2022 | 60444 | -7 | -5 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -56.4 |

| 2024 | -5 | -720.9 |

| 2023 | 674.6 | |

| 2022 | -317.6 |

Source: SEC companyfacts cache [F1].

All figures in thousands where applicable; negative percentages for operating income change reflect increasing losses.

Proprietary Magnetic Resonance Spectroscopy: Technological Differentiation

At the core of Aclarion’s offering is its NOCISCAN® platform based on Magnetic Resonance Spectroscopy (MRS). Unlike standard MRI which provides anatomical images depicting tissue structure, MRS measures chemical composition signals converted into spectra that reveal tissue biochemistry relevant to discogenic pain conditions in the lumbar spine [S1].

The technology integrates proprietary biochemical biomarkers licensed exclusively from UCSF that correlate strongly with painful intervertebral discs [S1]. Artificial intelligence aids spectral post-processing quality control by identifying poor-quality studies and enhancing diagnostic precision—fortifying a competitive moat supported by multiple patents covering biomarker discoveries and analytic methods.

This biochemical diagnostic approach addresses a key clinical gap as conventional lumbar MRI cannot reliably differentiate symptomatic degenerative discs from asymptomatic ones—a factor contributing to failed back surgery syndrome when inappropriate disc levels are treated.

Clinical Validation and Surgeon Adoption Progress

Market acceptance depends on robust clinical evidence demonstrating superior patient outcomes versus existing standards of care—a focus area supported by ongoing Key Opinion Leader (KOL)-driven clinical studies published in peer-reviewed literature [S1]. These studies indicate that incorporating NOCISCAN findings into surgical planning reduces unnecessary surgeries and improves targeting of pathological discs.

Physician education initiatives emphasize training on interpreting MRS spectra and integrating biochemical insights into decision-making workflows to drive referrals among spine surgeons new to spectroscopy-based diagnostics [S1]. However, adoption remains early-stage given novelty and inertia favoring anatomical imaging paradigms.

Commercial Deployment: Scanner Compatibility and Reimbursement Challenges

Commercial success requires integration into hospital imaging workflows facilitated by compatible MRI platforms alongside favorable payer coverage enabling sustainable reimbursement.

Currently NOCISCAN is compatible primarily with select Siemens and Philips MRI scanners—estimated at about 1,500 installed units in the U.S., part of an approximate global installed base of 4,320 such compatible systems capable of spectroscopy [S12]. Upgrading scanners with spectroscopy hardware/software involves costs ranging from USD 25K-50K per machine which may slow adoption rates.

Plans include collaborations with additional MRI vendors to broaden compatibility though dependency on limited partners presents concentration risk [S12].

On reimbursement frontiers, NOCISCAN holds temporary Category III CPT codes granted by CMS for emerging technologies lacking widespread coverage; conversion to permanent Category I codes with adequate reimbursement levels would materially enhance commercial viability but remains uncertain given CMS evaluation complexity [S12]. The company actively pursues payer contracts supported by accumulating real-world evidence.

Growth Opportunities Amid Market Complexities

Beyond lumbar applications targeting chronic discogenic pain, Aclarion aims to expand MRS diagnostics into cervical spine disorders addressing neck pain—though smaller cervical disc size presents technical challenges for obtaining quality spectroscopic data [S1]. Success here could broaden addressable markets within the $134 billion U.S low back and neck pain treatment landscape noted in medical literature.

Additional avenues include leveraging biomarker insights for conservative therapy management such as physical therapy or regenerative treatments enabling personalized care pathways.

Barriers include clinician hesitancy toward novel modalities without long-term multi-center validation; entrenched competing diagnostic methods; reimbursement variability lengthening sales cycles; plus rigorous regulatory compliance requirements constraining rapid expansion.[S1]

Capital Allocation and Financial Sustainability Considerations

Capital expenditure increased markedly (+321%) from approximately USD 5K in FY2024 to USD 21.5K in FY2025 focused on software enhancements including AI quality controls and expanding scanner compatibility programs [F1].

Operating cash flow remains deeply negative due to ongoing clinical study expenses and commercialization efforts exceeding USD 7 million annually without profitability yet achieved [F1]. Equity position improved substantially into positive territory exceeding USD 12 million at FY2025-end following fundraising rounds supporting continued development amid cash burn dynamics.

Return on equity stands at approximately -56%, consistent with early-stage medtech firms investing heavily pre-scale-up phases.[F1]

No dividends or share repurchases have been declared as reinvestment prioritizes technological advancement and market penetration.

Regulatory Environment and Compliance Risks

Aclarion operates under extensive regulatory frameworks including FDA medical device regulations governing design controls, manufacturing practices and clinical trial oversight under Good Clinical Practice standards due to ongoing validation efforts[S15][S20].

Healthcare fraud statutes like the Anti-Kickback Statute and False Claims Act impose constraints on financial relationships involving physicians or providers; violations could lead to severe penalties including fines or exclusion from federal programs Medicare/Medicaid affecting revenue streams.

Data privacy laws such as CCPA/CPRA in California alongside HIPAA federal protections plus European GDPR impose stringent requirements safeguarding sensitive patient information collected via spectroscopy scans—entailing operational costs and exposure to breach-related risks[S6][S16][S19].

Failures in compliance may result in reputational harm alongside financial consequences impacting business viability.

Key Milestones Investors Should Monitor

- Expansion of scanner compatibility partnerships beyond Siemens/Philips facilitating broader geographic reach.

- Progress toward converting temporary CPT codes into permanent categories ensuring sustainable reimbursement.

- Clinical study results demonstrating improved patient outcomes reinforcing physician adoption.

- Advances in cervical spine diagnostic applications overcoming technical challenges.

- Capital raise activities supporting liquidity amidst continued investment needs.

- Regulatory approvals or clearances related to new indications or post-market surveillance outcomes.

- Compliance monitoring for anti-fraud statutes adherence and data privacy safeguards mitigating operational risks.

In conclusion, Aclarion stands at the forefront of an innovative niche within interventional pain diagnostics combining scientific rigor with early-stage commercialization hurdles typical of breakthrough healthcare technologies.

This analysis summarizes publicly filed information as of March 19th, 2026 without providing investment advice or price projections.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments