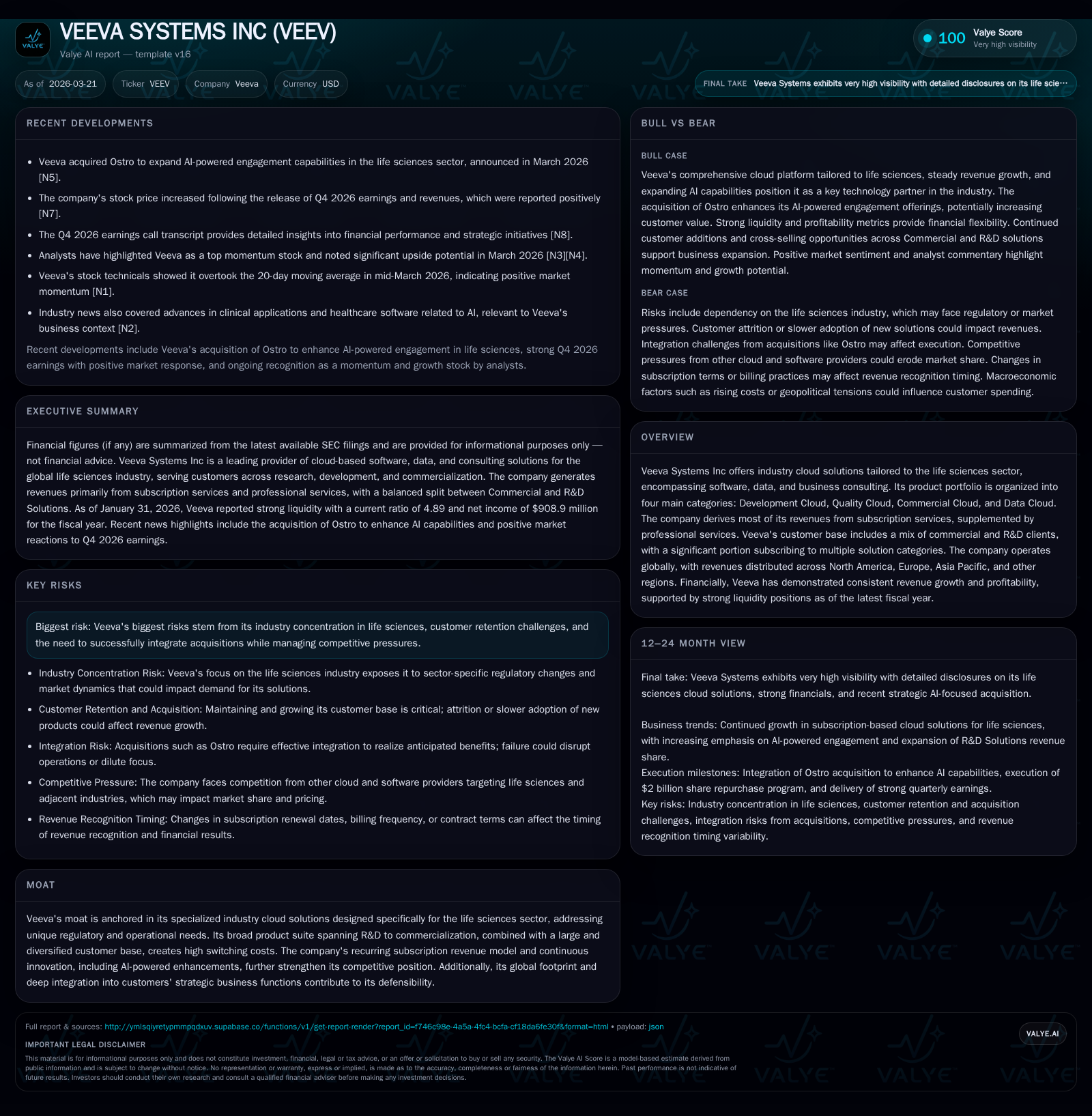

Veeva Systems' Growth Surge and Strategic AI Expansion in Life Sciences Cloud

Veeva balances robust multi-year financial growth with strategic AI acquisitions and capital discipline in a specialized industry cloud market.

Veeva Systems has demonstrated strong revenue and profitability momentum, marked by a 34.1% revenue increase in its latest fiscal year and high cash flow generation. Its specialized life sciences industry cloud solutions, primarily subscription-based, foster high customer retention through integrated product suites spanning R&D and commercial functions. Recent strategic acquisition of Ostro enhances Veeva's AI capabilities, reinforcing its competitive moat. The company exhibits disciplined capital allocation with substantial free cash flow and an active share repurchase program, while carefully managing operational efficiency amidst rising R&D investments. Going forward, integration of AI-driven features and geographic diversification remain key to sustaining growth amid concentration and competitive risks.

Financial Momentum: Examining Multi-Year Growth and Margin Expansion

Veeva Systems' financial trajectory over recent years underscores a vigorous growth pattern fueled by expanding adoption of its industry cloud solutions for the life sciences vertical. Revenue progressed from approximately $150 million in FY2017 to over $3.11 billion by FY2026, marking an annualized expansion catalyzed by customer demand for digital transformation tools tailored to regulatory-intensive workflows [F1]. The latest fiscal year delivered a substantial 34.1% year-over-year increase in top-line revenue.

This surge translated into commensurate operating income growth of 32.5%, reaching $916 million in FY2026, indicative of operating leverage benefits alongside scaling subscription revenues [F1]. Net income followed suit with a robust rise to $909 million (+27.3%). Moreover, operating cash flow exceeded $1.4 billion (up nearly 30%), affirming the strong cash conversion typical of SaaS businesses with high subscription ARR quality [F1]. Capital expenditure remains lean relative to cash flow, facilitating ample free cash flow availability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2026 | 909 | 1415 | 916 | +27.3% |

| 2025 | 714 | 1090 | 691 | +35.8% |

| 2024 | 526 | 911 | 429 | +7.8% |

| 2023 | 488 | 780 | 459 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2026 | 12.6 |

| 2025 | 12.2 |

| 2024 | 11.3 |

| 2023 | 13.1 |

Source: SEC companyfacts cache [F1].

*Latest three years reflect reported year-end figures with comprehensive segment encapsulation [F1].

Subscription Model and Product Suite: Drivers of Recurring Revenue Strength

Central to Veeva's durable financial performance is its industry-focused subscription services architecture which comprised roughly 84% of total revenues for the recent periods analysed [S5],[S6]. The company's product offering is segmented into Commercial Solutions (Commercial Cloud & Data Cloud) and R&D Solutions (Development Cloud & Quality Cloud), collectively serving both the commercial go-to-market and regulated research functions within life sciences firms.

The integrated suite creates meaningful switching costs; customers frequently adopt multiple solution categories across developmental pipelines through commercialization stages leveraging Veeva’s ecosystem . This widespread cross-vertical adoption elevates customer retention rates—the lifeblood of subscription ARR expansion—and increases average contract value per account.

Further embedding itself within critical workflows such as regulatory compliance documentation management, clinical trials data harmonization, commercial detailing outreach, and analytics ensures sticky usage patterns that underpin Veeva's recurring revenue base [S12],[S18]. Professional services contribute approximately 16% complementing subscription fees via implementation consulting that both facilitates product rollouts and fortifies client relationships.

AI-Powered Enhancements and M&A: Expanding the Innovation Frontier

Innovation acceleration through AI integration has become a defining strategic thrust for Veeva as it seeks to maintain its category leadership and deepen functional differentiation within life sciences cloud software [N5]. In March 2026, Veeva acquired Ostro — an early-stage startup specializing in AI-powered customer engagement solutions geared towards pharma sales forces — for about $100 million [N3],[N5].

This move signals an intentional expansion into smart automation, enabling clients to harness machine learning models for targeted outreach optimization across omnichannel marketing initiatives fine-tuned to healthcare professionals’ evolving preferences.

Such acquisitions are tactically synergistic; they augment existing CRM-like Commercial Cloud capabilities while preserving the integrity of the broader life sciences SaaS platform rather than diluting focus with unrelated adjacencies . It exemplifies prudent capital deployment focused on accelerating platform-derived value enhancement instead of speculative diversification.

Global Footprint and Customer Diversification: Mitigating Concentration Risks

While North America remains Veeva’s dominant revenue pool—contributing roughly two-thirds or more—the company has progressively diversified its geographic reach into Europe, Asia Pacific, and emerging markets including Middle East, Africa, and Latin America segments [S5],[S17]. For example, Europe accounts for nearly one-quarter of revenues with steady growth dynamics corroborated by increasing subscription uptake among regional life sciences enterprises [S5].

Customer counts have steadily grown with approximately mid-thousands served globally spread between Commercial Solutions (around 730 customers) and R&D Solutions (over 1100 clients), some engaging both lines of offerings concurrently [S6],[S12]. The mix includes large multinational pharma corporations as well as smaller biotechs progressing through development pipelines—a spectrum that naturally tempers single-client concentration threats.

However, inherent exposure to the life sciences vertical constitutes a structural risk factor given sector cyclicality themes like drug approval cycles or regulatory shifts which could influence spend patterns abruptly despite broad client dispersion .[S4]

Capital Allocation Discipline: Cash Flow Generation, Buybacks, and Shareholder Returns

Veeva exercises rigorous capital stewardship exemplified by robust free cash flow generation exceeding $1.41 billion in FY2026 (derived from CFO minus minimal capex outlays), emphasizing efficient conversion from earnings to liquidity [F1]. This liquidity supports flexible deployment options including organic growth investments alongside capital returns.

Notably, early January 2026 governance approved a $2 billion share repurchase plan valid over two years aimed at optimizing capital structure and delivering shareholder value through stock price support mechanisms amidst volatile market conditions [S20]. Dividend activity is not prominently disclosed suggesting preference for reinvestment plus repurchase strategies typical among high-growth tech SaaS entities.

The firm's ROE based on FY2026 net income relative to equity stands near an appreciable ~12.6%, demonstrating effective profit generation on shareholders’ funds supporting ongoing valuation robustness [F1].

Operational Efficiency Initiatives: R&D Investment Versus Capex Trends

Analysis of expense trends reveals rising commitments toward research and development expenditures aligned with the company’s innovation agenda encompassing AI integration and continuous product evolution [S11],[S14],[S15]. These investments absorb a meaningful portion of operating resources but do so without substantially inflating capital expenditures which remain subdued due to the SaaS model's cloud infrastructure reliance rather than physical asset intensity.

This strategy balances scalable software enhancements against controlled overhead footprint allowing margins expansions amid competitive differentiation demands—a hallmark management operational lever within enterprise SaaS contexts targeting regulated industries like pharmaceuticals where compliance complexities mandate constant platform updates.

Investor Sentiment and Market Position: Wall Street’s Take on Veeva’s Trajectory

While detailed consensus estimates are not provided here explicitly, recent coverage reflects positive momentum following Q4 fiscal results that surpassed analyst expectations driving bullish commentary on upside potential approaching or exceeding +50% from current valuations according to recent Nasdaq analyst articles [N7],[N8],[N9]. Such sentiment aligns with recognized leadership positioning in life sciences cloud combined with strategic AI deal-making fueling investor confidence in sustainable growth runway.

Risks to Monitor: Industry Focus, Integration Challenges, and Competitive Pressures

Veeva faces several intrinsic risks as documented formally within SEC disclosures including intense concentration within the specialized life sciences sector exposing it to regulatory changes or client spend variability specific to pharma/biotech cycles [S4]. Integration risk also emerges related to ongoing M&A activity notably early-stage ventures like Ostro whose technologies must be seamlessly embedded without disruption or cultural friction.

Competitive pressures arise from entrenched enterprise software vendors extending into life sciences verticals plus newer niche players advancing domain-specific analytics or workflow automations capable of eroding market share unless countered effectively via feature innovation—areas requiring vigilant R&D focus aligned with customer success initiatives.

Outlook and Key Milestones: What to Watch Post-Acquisition

Absent explicit formal guidance for forthcoming periods in publicly available materials per this analysis window [N1],[N2], strategic attention should focus on outcomes related to Ostro integration progress including deployment speed of enhanced AI features within Commercial Cloud suites impacting renewal rates or enabling upsell opportunities beyond existing customer bases.

Moreover, growth vectors anticipated include further penetration into R&D Solutions with increased addressable markets outside traditional pharma verticals potentially unlocking incremental cross-industry applications particularly across North American/European segments noted previously [N3],[N5],[S12]. Monitoring quarterly cadence around backlog trends deferred revenue changes can yield insights into subscription base expansions affirming ongoing momentum.

This analysis is based strictly on publicly available company filings, news reports dated up to March 21, 2026, and recognized financial metrics without any investment recommendation or price projection implied herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments